Carry, basis, and funding-trade concepts sit together because yield, financing, leverage, collateral, liquidity, and exit pressure can interact. Carry focuses on income, yield, or a funding spread. Basis focuses on a price relationship between related instruments. Funding stress focuses on financing constraints. An unwind describes exit pressure when a position can no longer be held cleanly. Volatility carry and reverse carry add different holding-risk conditions, while carry-and-roll-down is an assumption-based fixed-income estimate, not a guaranteed return.

- Carry is not the same thing as basis.

- Funding stress changes whether leveraged exposures can be held, financed, or reduced.

- Unwind pressure is about exits, not ordinary income collection.

- Volatility carry and reverse carry depend on different risk and holding-cost conditions.

- Carry-and-roll-down depends on curve and holding assumptions.

- These concepts are market-structure evidence, not standalone trading signals.

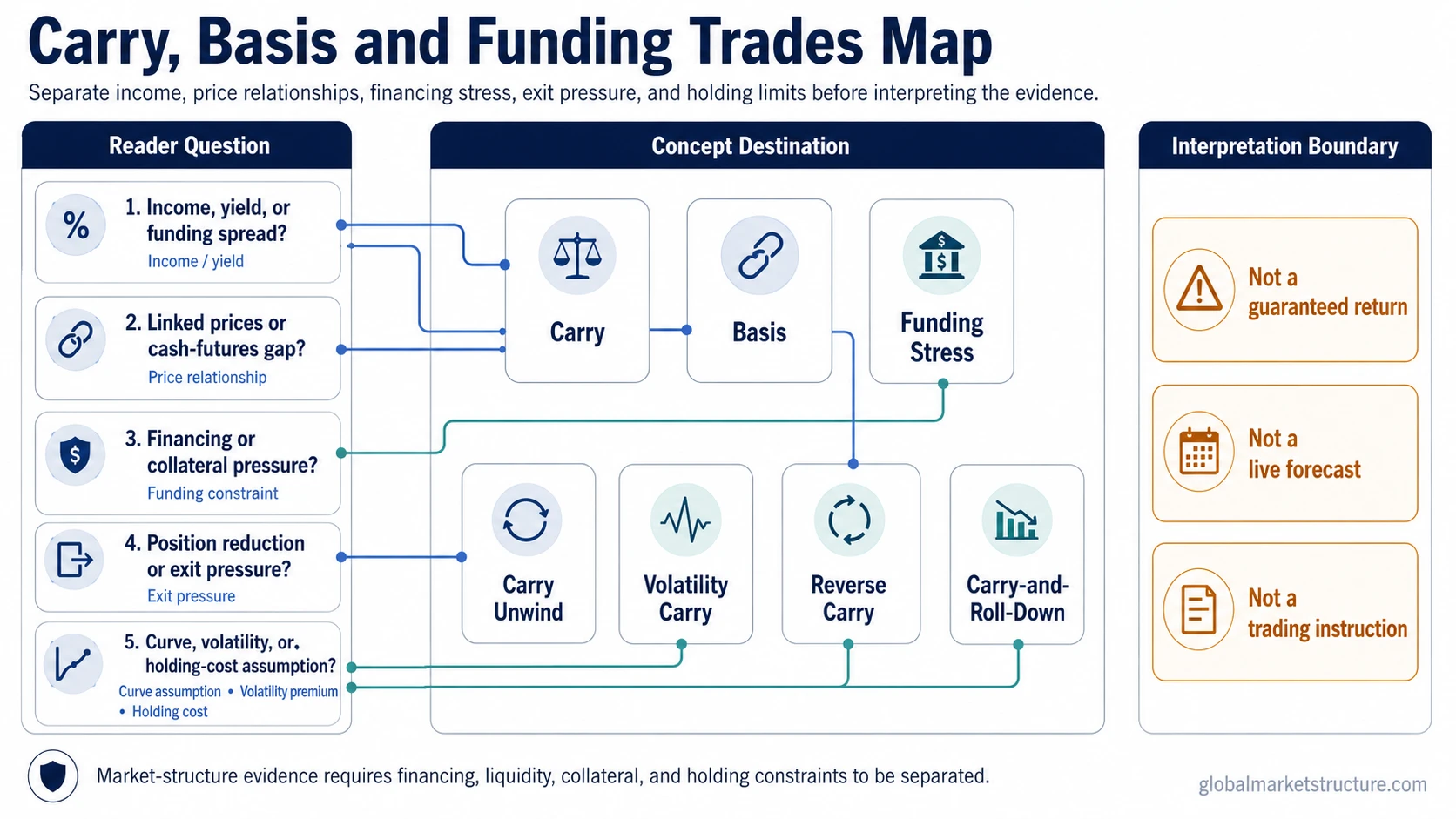

Which Concept Do You Need?

Start with the concept that matches the question. The same market episode can involve more than one idea, but each term answers a different problem.

| If the question is about… | Start with… | Why |

|---|---|---|

| Income, yield pickup, rate differential, or funding spread | carry trade | Carry begins with the relationship between financing cost and expected income or return from the exposure. |

| Cash-futures gaps, related-instrument pricing, or convergence risk | basis trade | Basis is about the relationship between linked prices, not simply the income from holding exposure. |

| Financing constraints, collateral pressure, or weaker ability to hold leveraged exposure | funding stress | Funding stress focuses on whether participants can finance positions, not whether the original trade idea was attractive. |

| Exit pressure from positions that were previously financed or crowded | carry trade unwind | An unwind is about position reduction and forced-flow pressure, not the normal income logic of carry. |

| Carry plus curve movement assumptions in fixed income | carry and roll-down | Carry-and-roll-down combines assumptions about income, curve shape, time, and holding conditions. |

Carry, Basis, Funding Stress, and Unwind Pressure Are Different

The useful distinction is not whether these ideas can appear in the same market environment. They often can. The distinction is what each concept is trying to explain.

| Concept | Main question | What it describes | Common misread |

|---|---|---|---|

| Carry | What is earned or paid to hold the exposure? | Income, yield pickup, financing spread, or holding cost. | Reading positive carry as a guaranteed return. |

| Basis | How are related instruments priced against each other? | A price relationship, spread, or convergence setup between linked markets. | Calling every basis gap risk-free arbitrage. |

| Funding stress | Can the position still be financed? | Pressure from borrowing cost, collateral needs, margin, liquidity, or balance-sheet limits. | Assuming stress automatically proves a live liquidation event. |

| Carry unwind | What happens when positions are reduced? | Exit pressure from exposures that may no longer be attractive or financeable. | Treating every price move as a forced unwind. |

| Volatility carry | What risk is being sold or absorbed for premium? | Exposure to volatility risk premium and stress-sensitive payoff behavior. | Ignoring how volatility spikes can change the holding condition. |

| Reverse carry | What does it cost to keep holding? | An unfavorable carry condition where holding the exposure has a cost rather than a yield benefit. | Confusing negative carry with a directional forecast by itself. |

| Carry-and-roll-down | What return is estimated if curve assumptions hold? | An assumption-based fixed-income estimate combining income and curve movement. | Reading the estimate as a realized or guaranteed return. |

How the Concepts Connect Through Market Pressure

A leveraged position can look attractive while funding is stable. The interpretation changes if financing costs rise, collateral demands increase, margin becomes harder to meet, or liquidity weakens. Under those conditions, a trade that once looked like a carry or basis opportunity can become a source of position-reduction pressure.

Yield or spread: Carry starts with the income, rate differential, or expected holding benefit.

Price relationship: Basis starts with the gap between related instruments, such as cash and futures markets.

Financing condition: Funding stress changes whether positions can be held without forced adjustment.

Exit path: Unwind pressure appears when participants reduce exposures because the financing, risk, or liquidity condition has changed.

Specialized Routes Inside This Group

Use the primary routes above for the broad distinction. Use the specialized routes below when the question is narrower.

Currency-funded carry: Use currency carry trade when the question is about borrowing in one currency and holding exposure in another. Use yen carry trade when the funding-currency lens is specifically the yen.

Basis variants: Use Treasury basis trade when the question involves Treasury cash, Treasury futures, repo financing, collateral, or margin sensitivity. Use cash-and-carry trade when the structure is about holding spot or cash exposure against a related futures contract.

Holding-cost and volatility variants: Use reverse carry trade when the question is about negative carry or the cost of holding exposure. Use volatility carry trade when the question is about volatility risk premium or short-volatility-style income exposure.

Fixed-income carry and curve movement: Use fixed-income carry when the question is about yield, financing, and holding a bond exposure. Use bond roll-down when the question is about a bond moving along the yield curve as time passes.

What Not to Infer From These Concepts Alone

- They are not one unified strategy category.

- They do not create guaranteed returns.

- They do not prove that a carry trade unwind is happening now.

- They do not prove current hedge-fund crowding or systemic risk without dated evidence.

- They are not buy, sell, long, short, entry, or exit signals.

- They should be read as market-structure evidence only after financing, liquidity, collateral, and holding constraints are separated.