Credit spreads are the extra yield investors demand to hold debt with credit risk instead of a safer benchmark with a similar maturity. They are usually discussed in basis points and are used to measure how much compensation markets require for default risk, downgrade risk, liquidity risk, and changing risk appetite.

In a Global Market Structure context, credit spreads mean credit-market yield spreads, not options credit spread strategies. Options credit spreads are trading structures built from options positions. Credit-market spreads are yield premiums in debt markets.

Widening and narrowing spreads are risk-pricing observations. They can help interpret financial conditions, but they do not independently forecast recessions, equity direction, or market timing.

What Credit Spreads Are

A credit spread is the yield difference between a debt security with credit risk and a safer benchmark of comparable maturity. The spread isolates the compensation investors demand for taking credit exposure rather than holding the safer reference asset.

The same-maturity comparison matters because yield differences can come from maturity, duration, inflation expectations, or policy-rate expectations. A credit spread is most useful when the benchmark comparison reduces those non-credit effects.

For example, a corporate bond is often compared with a Treasury yield of similar maturity. The remaining yield gap is treated as the market’s required compensation for the issuer’s credit risk and related liquidity conditions.

How Credit Spreads Are Calculated

The basic calculation is simple:

Credit spread = risky bond yield – comparable safer benchmark yield

If a corporate bond yields more than a similar-maturity Treasury, the difference is the credit spread. If the difference is 2 percentage points, the spread is 200 basis points. One basis point equals 0.01 percentage point.

The calculation is conceptually simple, but the interpretation depends on the bond type, benchmark, maturity, liquidity, issuer quality, and whether the spread series is option-adjusted.

What Credit Spreads Are and Are Not

| Credit spreads are | Credit spreads are not |

|---|---|

| Yield premiums for holding credit risk instead of a safer comparable benchmark. | Options credit spread strategies built from calls or puts. |

| A market-based measure of credit-risk compensation. | A standalone recession forecast. |

| A useful input inside broader financial-conditions analysis. | A direct equity-market timing tool. |

| A way to compare risk appetite across credit quality, maturity, and market stress conditions. | Proof that markets are safe when spreads are narrow. |

| An observable signal that can be tracked through credit-market data series and spread indexes. | A replacement for official data, bond-market context, or broader confirmation signals. |

What Credit Spread Widening and Narrowing Mean

Credit spreads widen when investors demand more yield compensation for holding credit risk. Widening can reflect rising default concern, weaker risk appetite, lower market liquidity, downgrade risk, or pressure in funding conditions.

Credit spreads narrow when demanded compensation falls. Narrowing can reflect easier risk appetite, stronger confidence in borrower credit quality, better liquidity, or calmer financial conditions.

The direction alone is not enough. Widening spreads can appear during broad risk reduction, but they can also reflect sector-specific stress, liquidity conditions in one credit segment, or a repricing of default risk that has not yet spread across markets. Narrow spreads can reflect calm credit pricing, but they do not prove that macro risk has disappeared.

Credit Spreads Inside Financial Conditions

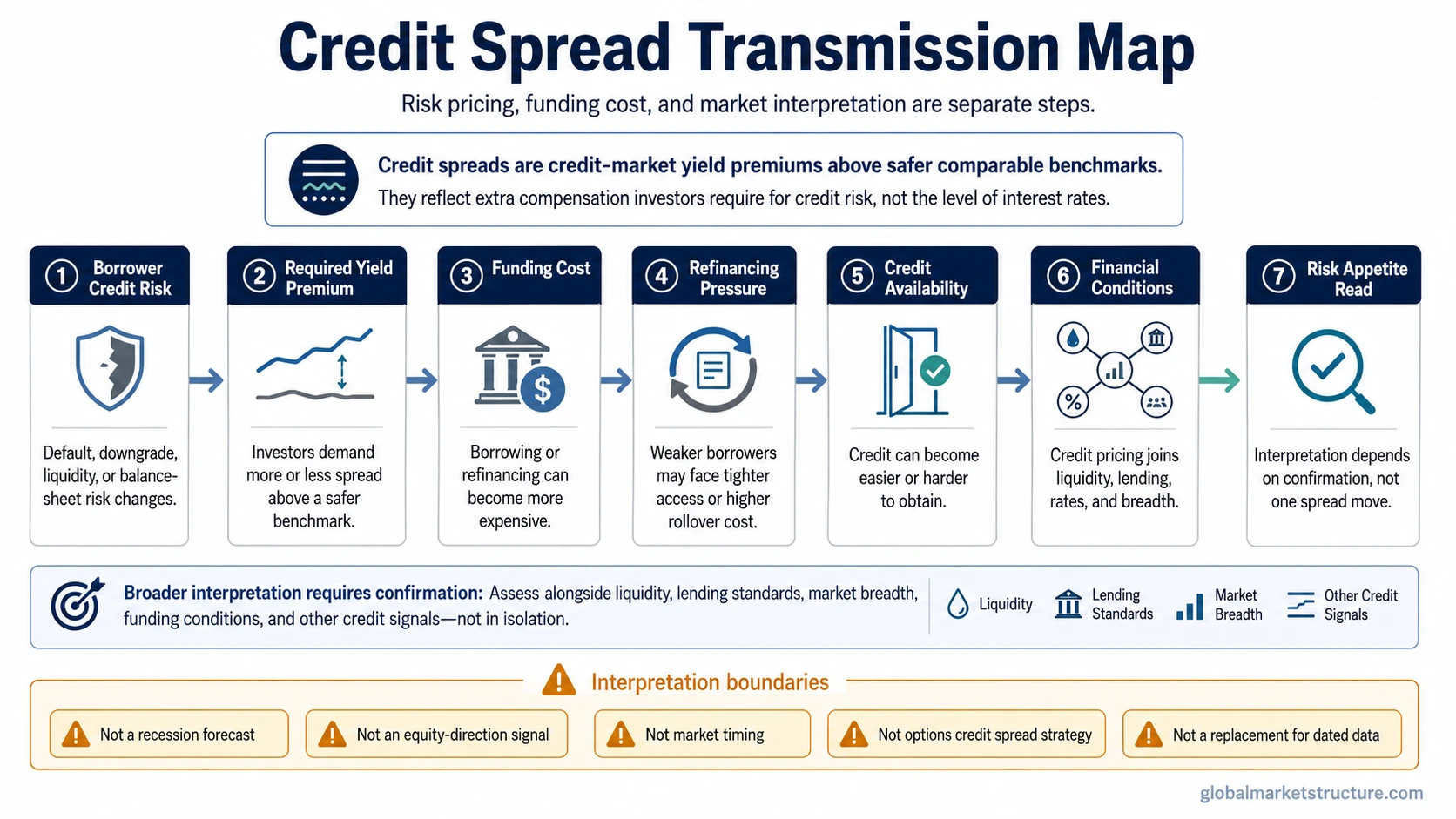

Credit spreads matter because they connect credit-risk pricing with the cost and availability of financing. When investors demand a higher yield premium, borrowers may face higher funding costs and more difficult refinancing conditions.

A useful transmission sequence is:

- Borrower credit risk: investors reassess default, downgrade, liquidity, or balance-sheet risk.

- Required yield premium: investors demand more or less compensation above safer benchmarks.

- Funding cost: higher spreads can raise the cost of issuing or refinancing debt.

- Credit availability: tighter pricing can reduce access to credit for weaker borrowers.

- Risk appetite: broader markets may treat widening spreads as a sign that risk compensation is deteriorating.

Because of that sequence, credit spreads are often read alongside a financial conditions index, liquidity measures, market breadth, and credit-supply indicators.

Limits of Credit Spread Interpretation

Credit spreads are strongest as confirmation inputs, not as isolated forecasts. A widening spread can indicate that credit risk is being repriced, but it does not automatically confirm recession, equity-market decline, or a specific timing window.

The signal carries more weight when other evidence points in the same direction. For example, widening spreads carry more weight when lending behavior is also tightening, liquidity is weakening, and market breadth is deteriorating. If those signals conflict, the interpretation stays less certain.

Credit spreads also differ from bank credit-supply behavior. Market spreads reflect the yield compensation investors demand in traded credit markets, while bank lending standards describe how banks are changing loan availability and underwriting behavior.

Common Misread: Treating Spreads as a Market Signal by Themselves

A common mistake is treating wider spreads as an automatic recession signal or treating narrow spreads as proof that risk is gone. Credit spreads measure compensation for credit risk. They do not identify the full macro regime by themselves.

Calm spreads can coexist with weakening growth signals, deteriorating breadth, or tighter bank lending. Widening spreads can also occur before other markets respond, after other markets have already repriced, or in only one part of the credit market.

The narrower interpretation of credit spreads widening depends on the surrounding evidence, including liquidity, lending standards, default risk, refinancing pressure, and broader financial conditions.

Illustrative Credit Spread Scenario

Imagine credit spreads begin widening while major equity indexes remain near recent highs. The widening does not prove that equities must fall. It indicates that credit investors are demanding more compensation for risk.

The interpretation becomes stronger if other conditions confirm the same message: bank lending standards tighten, lower-quality borrowers face refinancing pressure, market breadth weakens, and liquidity indicators deteriorate. If those signals remain stable, the spread move may still matter, but the broader market read stays less decisive.

Credit Spreads vs Options Credit Spreads

Credit-market spreads and options credit spreads use similar words for different concepts.

In credit markets, a credit spread is a yield premium. It compares the yield on riskier debt with a safer comparable benchmark.

In options markets, a credit spread is an options position that receives net premium when opened. That options usage involves option strikes, expirations, premiums, payoff profiles, and risk controls. Those mechanics belong to options education, not credit-market financial-conditions analysis.

Where Credit Spread Data Fits

Credit spread data series and chart tools are useful because spreads are observable market prices, not only abstract concepts. High-yield spreads, investment-grade spreads, option-adjusted spreads, and sector-level credit indexes can each answer different questions.

Any current spread level needs a dated data source. Without a dated source, credit-spread discussion should stay conceptual: what spreads measure, why they widen or narrow, and how they interact with broader financial conditions.

Credit Spreads FAQ

Are credit spreads the same as options credit spreads?

No. In credit markets, credit spreads are yield premiums for taking credit risk. In options markets, credit spreads are options structures built from multiple options positions.

Are credit spreads a recession signal?

Credit spreads can support recession-risk interpretation when they widen alongside weaker liquidity, tighter lending, deteriorating breadth, and broader financial stress. They are not standalone recession forecasts.

Why does same-maturity comparison matter?

Same-maturity comparison helps separate credit-risk compensation from maturity effects. Without a comparable benchmark, the yield difference may reflect duration, inflation expectations, or rate expectations rather than credit risk alone.