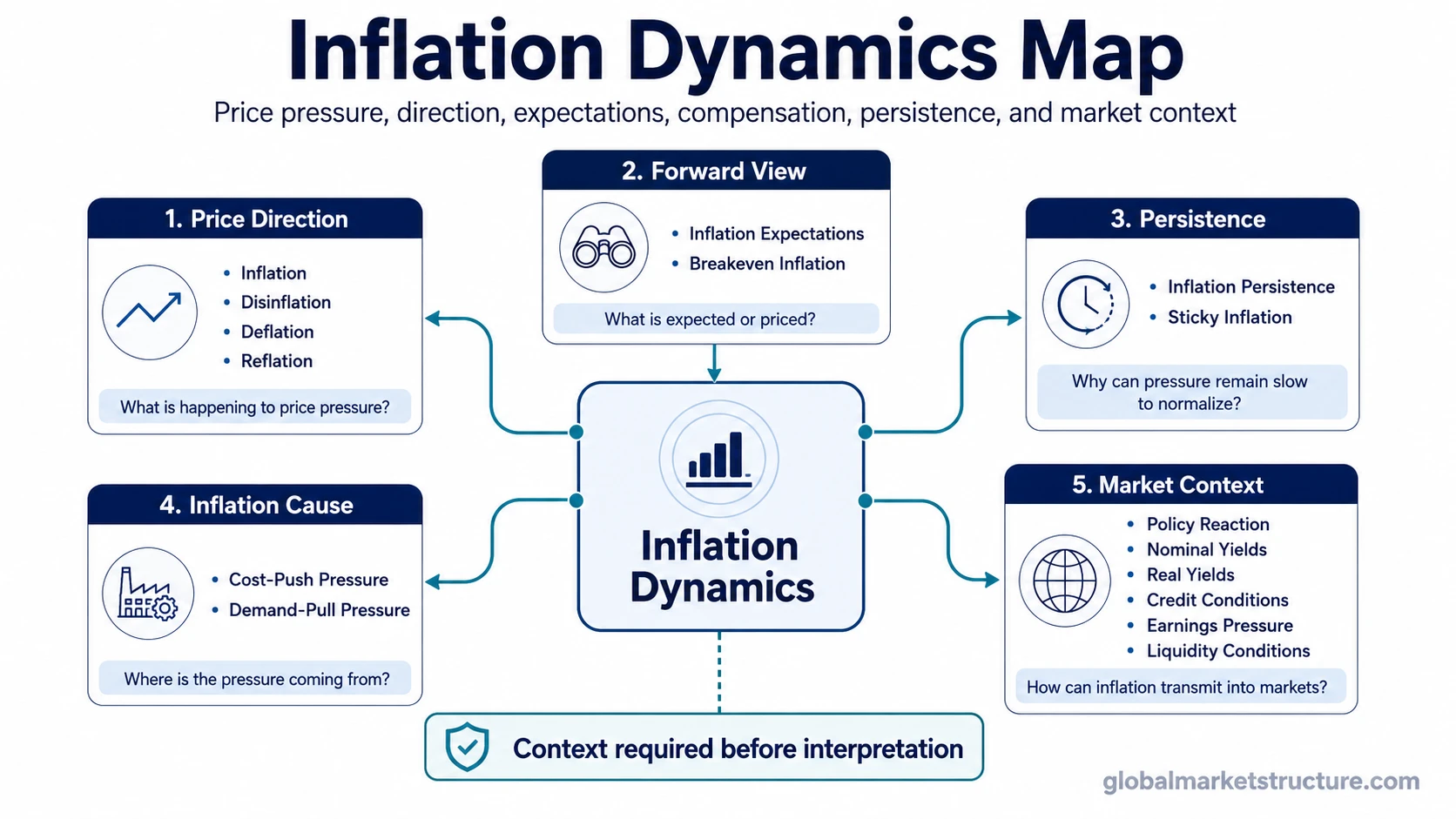

Inflation Dynamics is a map of related inflation concepts, not a single inflation signal. It separates realized inflation from changes in inflation direction, expected inflation, market-implied inflation compensation, persistence, sticky price behavior, and broad market effects.

The useful starting question is not whether inflation is automatically bullish or bearish. The better question is which inflation concept is being discussed and what kind of macro interpretation it supports.

Inflation question map

| Reader question | Best next concept | Why it fits |

|---|---|---|

| What does inflation mean in macro and market context? | Inflation | Defines the core price-level concept. |

| What does it mean when inflation is still positive but slowing? | Disinflation | Separates a slower inflation rate from falling prices. |

| What is outright deflation? | Deflation | Focuses on sustained price-level decline and its macro risks. |

| What is reflation? | Reflation | Covers renewed nominal pressure after weakness or deflationary pressure. |

| Why do inflation expectations matter? | Inflation Expectations | Focuses on expected inflation and how expectations can affect policy, yields, wages, and pricing behavior. |

| What does breakeven inflation measure? | Breakeven Inflation | Covers market-implied inflation compensation. |

| What is the difference between disinflation and deflation? | Disinflation vs Deflation | Resolves the common confusion between slower inflation and falling prices. |

| What is the difference between cost-push and demand-pull inflation? | Cost-Push vs Demand-Pull Inflation | Separates supply-side inflation pressure from demand-side inflation pressure. |

| Why can inflation stay elevated longer than expected? | Inflation Persistence | Focuses on why inflation pressure can remain difficult to normalize. |

| What is sticky inflation? | Sticky Inflation | Covers slower-moving inflation components and persistence risk. |

| How does inflation affect markets? | How Inflation Affects Markets | Connects inflation concepts to broader market interpretation. |

Realized inflation and inflation direction

Inflation is the core concept. It describes a rise in the general price level and provides the starting point for interpreting price pressure across the economy.

Disinflation means inflation is slowing while the inflation rate remains positive. Prices may still be rising, but the pace of increase is cooling.

Deflation means the general price level is falling. It is different from disinflation because the direction of prices has moved below zero inflation rather than simply slowing from a higher rate.

Reflation describes renewed inflation or nominal activity after weakness, deflation pressure, or a period of subdued demand. It can matter for macro interpretation, but it does not automatically define a risk-on market regime.

Expectations and market-implied inflation compensation

Inflation expectations focus on what households, businesses, investors, or policymakers expect inflation to be in the future. Expectations can influence wage demands, pricing behavior, bond yields, and policy interpretation.

Breakeven inflation is different. It reflects market-implied inflation compensation, often derived from the difference between nominal Treasury yields and inflation-protected Treasury yields. It can be useful, but it should not be treated as a clean forecast of future realized inflation.

Common comparison routes

Disinflation and deflation are often confused because both can appear during cooling macro conditions. The distinction matters because slower inflation and falling prices can imply different growth, policy, and earnings conditions.

Cost-push and demand-pull inflation answer a different question. Cost-push pressure comes from rising input costs or supply constraints, while demand-pull pressure comes from demand running ahead of supply. The cause can change how policymakers and markets interpret the same inflation reading.

Persistence and sticky inflation

Inflation persistence focuses on why inflation pressure can remain elevated or slow to normalize. It is useful when the question is not only what inflation is doing, but why it is not falling as quickly as expected.

Sticky inflation focuses on inflation components that adjust slowly. These components can make the inflation picture harder to interpret when faster-moving categories are already cooling.

Market impact

Broad inflation-market questions belong in market context, not in a single inflation label. Inflation can affect markets through policy reaction, nominal yields, real yields, credit conditions, earnings pressure, valuation multiples, currency effects, and liquidity conditions.

The market impact depends on the surrounding regime. Inflation during strong growth can be interpreted differently from inflation during weak growth. Disinflation with stable demand can be interpreted differently from disinflation caused by a sharp slowdown.

What inflation dynamics should not be reduced to

Inflation dynamics should not be reduced to a simple rule such as inflation bad, disinflation good, deflation bullish or bearish, or reflation automatically risk-on. Breakeven inflation is not the same as a guaranteed future inflation rate. Sticky inflation does not guarantee a specific policy outcome. Inflation data alone does not tell traders or investors what to buy or sell.

Inflation concepts become more useful when they are interpreted alongside policy reaction, growth conditions, real yields, nominal yields, liquidity, credit, labor conditions, and broader market context.

Suggested next path

Start with Inflation if the goal is the core definition. Move to Disinflation, Deflation, or Reflation when the question is about inflation direction. Use Inflation Expectations and Breakeven Inflation for forward-looking interpretation. Use Inflation Persistence and Sticky Inflation when the issue is why inflation may remain difficult to normalize. Use How Inflation Affects Markets when the question is broader market transmission.