Inflation expectations are beliefs, estimates, or market-implied compensation about future inflation. They matter because expected inflation can affect wage demands, price setting, central-bank credibility, nominal yields, real yields, business margins, credit conditions, liquidity, and risk appetite.

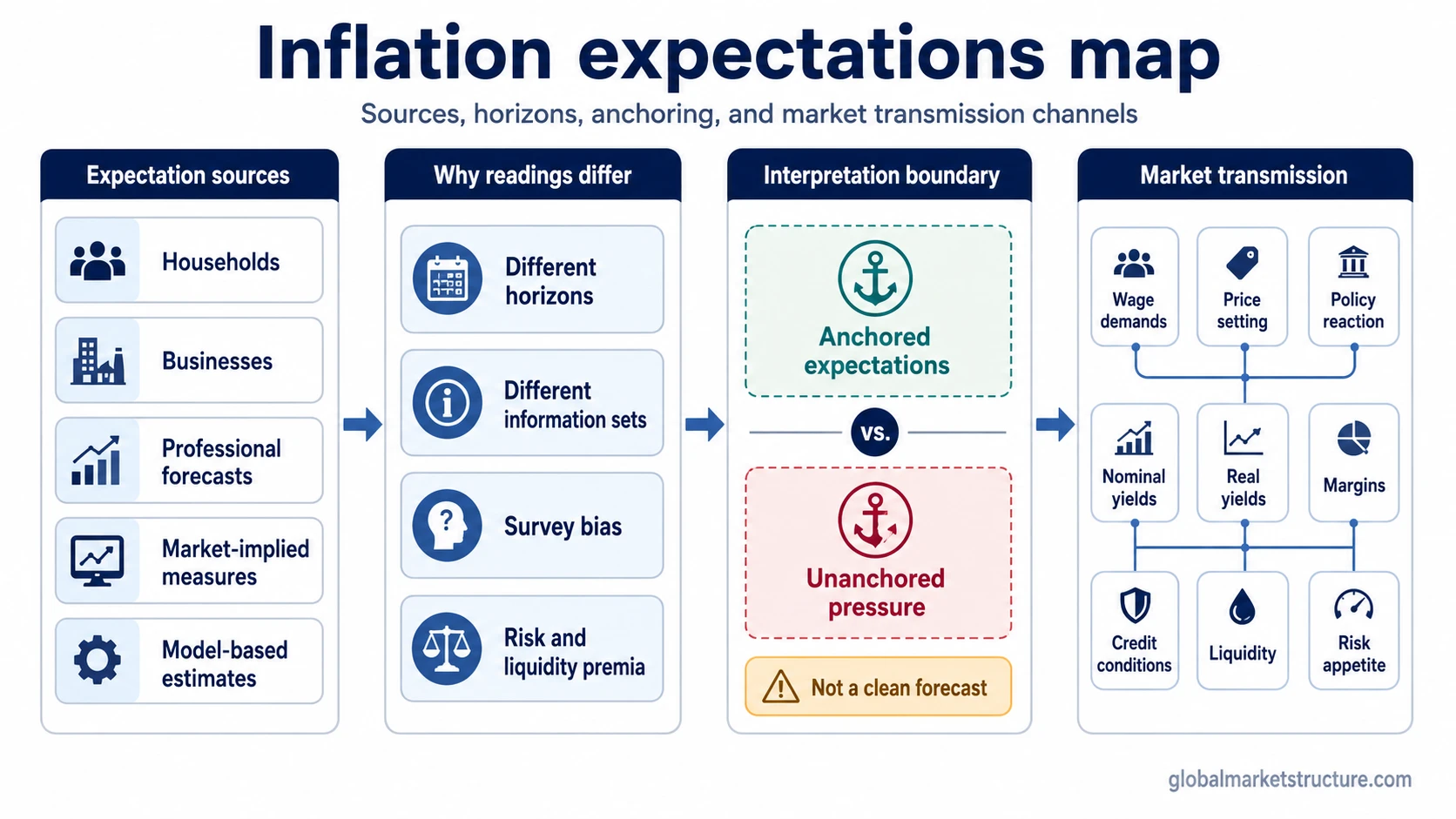

No single inflation-expectation measure gives a clean forecast. Household surveys, business surveys, professional forecasts, market-implied measures, and model-based estimates can disagree because they come from different sources, cover different horizons, and include different biases or market premia.

The interpretation depends on which measure is moving, why it is moving, whether expectations remain anchored, and how policy, yields, credit, and risk appetite absorb the shift.

Definition: Inflation expectations describe what households, businesses, investors, forecasters, or models expect inflation to be in the future. They are forward-looking views about inflation, not the same thing as realized inflation and not the same thing as a current inflation nowcast.

Some measures come from surveys. Some come from market prices. Some come from professional forecasts or central-bank models. Each channel answers a different question, so interpretation depends on the source, horizon, and measurement limits.

Why inflation expectations matter

Inflation expectations can influence behavior before future inflation is observed. If workers expect higher inflation, wage demands may rise. If businesses expect higher input costs, pricing decisions may change. If central banks believe expectations are becoming unanchored, policy may stay tighter for longer than current inflation alone would imply.

Financial markets respond through several channels. Higher expected inflation can lift nominal yield compensation. If policy reaction becomes more aggressive, real yields can also rise. That combination can affect equity valuation pressure, credit spreads, liquidity conditions, and the willingness to hold risk assets.

Expectations also shape the difference between a temporary inflation shock and a more persistent inflation regime. A one-time price shock is easier for policy makers and markets to absorb when longer-term expectations remain anchored. The same shock becomes more difficult when households, firms, and investors begin assuming that higher inflation will persist.

How inflation expectations are measured

Inflation expectations are not measured through one universal indicator. Each channel reflects a different group, horizon, and information set.

| Measure or channel | Who or what it reflects | Question it helps answer | Main limitation |

|---|---|---|---|

| Household surveys | Consumers and households | How people perceive future inflation in daily expenses, income planning, and purchasing decisions | Responses can be influenced by visible prices such as food, fuel, rent, and recent personal experience |

| Business surveys | Firms and pricing decision makers | How companies expect costs, wages, and selling prices to evolve | Expectations may vary by industry, margin pressure, labor exposure, and supply-chain conditions |

| Professional forecasts | Economists, institutions, and forecasting panels | How analysts estimate future inflation across defined horizons | Forecasts can lag turning points and depend on model assumptions |

| Market-implied measures | Prices of nominal bonds, inflation-linked bonds, and related market instruments | How markets price inflation compensation over a given horizon | They may include inflation risk premia, liquidity effects, term premia, and market-condition distortions |

| Central-bank or model-based estimates | Statistical models that combine multiple data and market inputs | How institutions estimate expected inflation after adjusting for observed inputs and model structure | Model outputs depend on methodology and should not be treated as direct observations |

A household survey may capture lived price pressure. A market-implied measure may capture inflation compensation embedded in bond markets. A model-based estimate may try to separate expected inflation from risk premia. Those are related, but they are not interchangeable.

How expectations move through markets

Inflation expectations affect markets through a chain of behavior, policy response, and asset-pricing channels.

- Expectations form: households, firms, investors, forecasters, and models update views about future inflation.

- Behavior changes: wage demands, pricing decisions, spending patterns, and margin assumptions can adjust.

- Policy credibility is tested: central banks judge whether expectations remain anchored or are drifting away from target-consistent behavior.

- Policy reaction changes: expected rate paths, policy restraint, and communication can shift.

- Yields reprice: nominal yields, real yields, and breakeven inflation can move for different reasons.

- Markets absorb the signal: margins, credit conditions, liquidity, duration sensitivity, and risk appetite adjust to the new inflation-policy mix.

The sequence is not mechanical. A rise in household inflation expectations can mean something different from a rise in market-implied inflation compensation. A market move can reflect expected inflation, but it can also reflect changing real yields, liquidity premia, inflation risk premia, or a stronger expected policy response.

Why inflation-expectation measures can disagree

Different inflation-expectation measures often disagree because they are built from different inputs. Consumers may react strongly to prices they see frequently. Businesses may focus on wages, inventory, supplier costs, and pricing power. Investors may price inflation compensation alongside liquidity, term premia, and policy risk.

Horizon also matters. Short-term expectations may react to energy prices, food prices, rent changes, or tax effects. Longer-term expectations are more important for policy credibility because they show whether inflation beliefs remain anchored beyond near-term shocks.

Market-implied measures require extra care. A spread between nominal and inflation-linked securities can be useful, but it is not a pure survey of investor beliefs. It can include compensation for inflation uncertainty, differences in liquidity, and other market-pricing effects.

Disagreement is not automatically a flaw. It can be the most important part of the signal. Divergence forces the analyst to ask whether inflation pressure is consumer-led, business-led, market-priced, model-estimated, or policy-driven.

Inflation expectations vs related concepts

| Concept | Core meaning | How it differs from inflation expectations |

|---|---|---|

| Realized inflation | Inflation that has already occurred in measured price data | Inflation expectations look forward, while realized inflation records past or current price changes |

| Inflation nowcasting | Estimates of current or near-term inflation before full official data are available | Nowcasting estimates near-present inflation, while expectations describe future inflation views or compensation |

| Breakeven inflation | Market-implied inflation compensation from nominal and inflation-linked bond pricing | Breakevens are one market-based channel, not the whole set of inflation expectations |

| Sticky inflation | Inflation that adjusts slowly because some prices are less flexible | Sticky inflation can influence expectations, but it describes price behavior rather than expectations themselves |

| Inflation persistence | The tendency for inflation pressure to continue over time | Persistence can shape expectations, but expectations are beliefs or compensation about future inflation |

| Reflation | A recovery phase where inflation and nominal growth pressures rise from weak conditions | Reflation is a broader macro regime concept, while expectations are one forward-looking inflation channel within that environment |

Practical scenario: consumer expectations rise while market expectations stay stable

A common scenario is that households report higher expected inflation because visible prices feel painful, while market-implied inflation compensation remains stable. That difference does not automatically mean one side is wrong.

Consumers may be reacting to recent price experience. Bond markets may be pricing a stronger central-bank response, weaker future demand, or liquidity effects inside inflation-linked securities. Professional forecasters may sit between the two because their estimates depend on policy assumptions, base effects, and model structure.

The market-structure interpretation depends on the full mix. If household expectations rise while long-term expectations remain anchored, the signal may point to near-term price stress without a broad credibility problem. If survey expectations, business expectations, market-implied compensation, and wage behavior all move higher together, the risk of an unanchored inflation regime becomes more serious.

When inflation expectations can mislead

Inflation expectations can mislead when one measure is treated as the whole story. A consumer survey can exaggerate the influence of recent visible price changes. A business survey can reflect sector-specific cost pressure. A market-implied measure can move because of liquidity, risk premia, or changing policy expectations rather than expected inflation alone.

The false reading is strongest when source, horizon, and policy context are ignored. A short-term rise in expected inflation does not automatically mean a lasting inflation regime. A stable market-implied spread does not automatically mean inflation risk is gone. A high survey reading does not automatically create a market signal.

Inflation expectations become more useful when they are read across channels: who is forming the expectation, what horizon is being measured, whether expectations remain anchored, and how policy and yields are likely to respond.

Anchored and unanchored expectations

Anchored inflation expectations mean longer-term inflation beliefs remain close to a stable policy-consistent range even when near-term inflation moves around. This gives central banks more room to treat temporary shocks as temporary.

Unanchored expectations are more dangerous. If households, firms, and markets begin assuming that high inflation will persist, wage-setting, pricing behavior, and policy expectations can reinforce one another. In that environment, central banks may respond more forcefully because credibility becomes part of the inflation problem.

The distinction matters for markets because anchored expectations can reduce the risk that every inflation shock becomes a policy shock. Unanchored expectations can raise uncertainty around the policy path, real yields, margins, and credit conditions.

How to interpret inflation expectations in market context

A useful interpretation starts with the source. Household expectations are not business expectations. Business expectations are not professional forecasts. Market-implied measures are not pure forecasts. Model-based estimates are not direct observations.

The next step is the horizon. Short-term expectations can react to temporary price shocks. Longer-term expectations are more important for credibility, policy reaction, and regime interpretation.

The final step is transmission. If expectations rise but policy credibility remains strong, markets may focus on real yields and expected policy restraint. If expectations rise while credibility weakens, markets may price a more difficult inflation regime with higher risk premia, weaker liquidity, and more pressure on long-duration assets.

Inflation expectations are most useful when combined with realized inflation, labor-market pressure, wage behavior, credit conditions, liquidity, and policy reaction. They are a forward-looking input, not a standalone forecast or trading instruction.

FAQ

What are inflation expectations?

Inflation expectations are beliefs, estimates, or market-implied compensation about future inflation. They can come from households, businesses, forecasters, market prices, or models.

How are inflation expectations measured?

They are measured through channels such as household surveys, business surveys, professional forecasts, market-implied inflation compensation, and model-based estimates. Each channel reflects a different source and horizon.

Are inflation expectations the same as breakeven inflation?

No. Breakeven inflation is one market-implied measure of inflation compensation. It can include inflation risk premia, liquidity effects, and other market-pricing influences, so it should not be treated as the whole concept.

Are inflation expectations a forecast?

They can contain forecast information, but they are not a clean forecast. Survey expectations, market-implied measures, and model estimates can all be affected by bias, premia, horizon differences, and policy assumptions.

Why can different inflation expectation measures disagree?

They can disagree because households, firms, investors, forecasters, and models use different information. Survey bias, market liquidity, inflation risk premia, policy expectations, and time horizon can all change the reading.