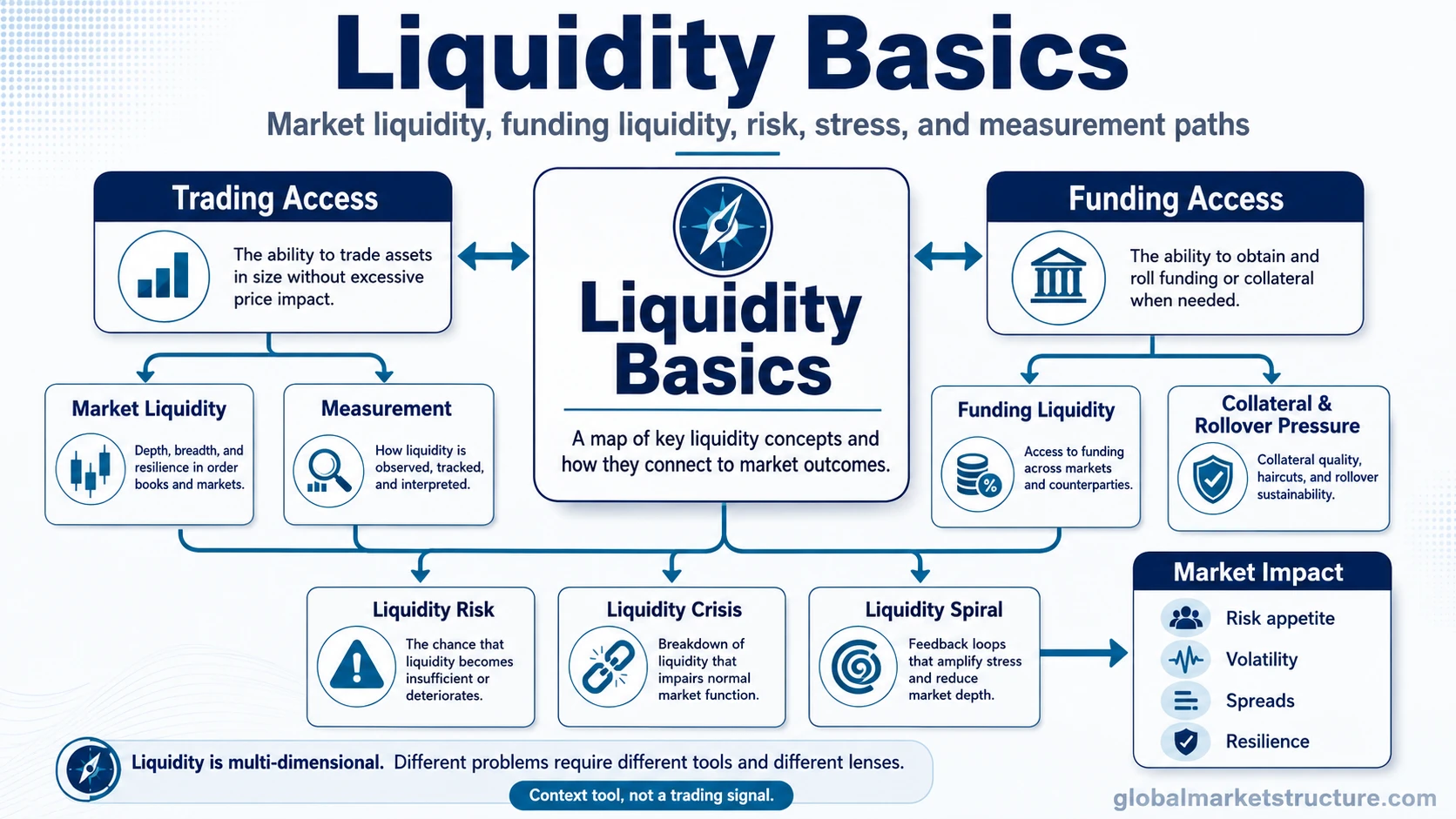

Liquidity basics start with one distinction: some liquidity problems come from the ability to trade assets, while others come from the ability to obtain funding.

The useful starting point is choosing whether the liquidity question is about trading access, funding access, stress behavior, or measurement.

In market structure, liquidity is not one single bullish or bearish signal. It can describe how easily assets trade, how easily participants finance positions, how quickly stress spreads, or how market conditions change when depth disappears.

The main paths are market liquidity, which focuses on trading conditions, and funding liquidity, which focuses on access to financing, collateral, leverage, and rollover pressure.

Liquidity Concept Map

Liquidity questions become clearer when the concept is matched to the actual problem: trading access, financing access, risk, crisis behavior, self-reinforcing stress, or measurement.

| Concept | Use it when the question is… | What it clarifies | Destination |

|---|---|---|---|

| Liquidity | What does liquidity mean in market context? | The broad concept and why it matters across markets. | Liquidity |

| Market Liquidity | Can an asset be traded without large price impact? | Depth, spreads, volume, turnover, and price impact. | Market Liquidity |

| Funding Liquidity | Can participants obtain financing or roll funding? | Collateral, leverage, credit access, and financing pressure. | Funding Liquidity |

| Liquidity Risk | What can go wrong when liquidity disappears? | Transaction risk, funding risk, forced-selling pressure, and execution stress. | Liquidity Risk |

| Liquidity Crisis | What happens when normal liquidity breaks down? | Stress conditions, market dysfunction, funding pressure, and impaired confidence. | Liquidity Crisis |

| Liquidity Spiral | How can liquidity stress reinforce itself? | Selling pressure, margin pressure, lower collateral values, and feedback loops. | Liquidity Spiral |

| Market Liquidity vs Funding Liquidity | Which type of liquidity problem is visible? | The difference between trading access and financing access. | Market Liquidity vs Funding Liquidity |

| How to Measure Market Liquidity | Which indicators describe market liquidity conditions? | Bid-ask spreads, depth, volume, turnover, and price impact. | How to Measure Market Liquidity |

| How Liquidity Affects Markets | How does liquidity transmit into broader market behavior? | Risk appetite, volatility, spreads, cross-asset stress, and market resilience. | How Liquidity Affects Markets |

Core Liquidity Concepts

Liquidity is the broad market concept. It describes how easily value can move through assets, funding channels, and market conditions without excessive friction or instability.

Market liquidity focuses on the trading side. A market is more liquid when participants can buy or sell meaningful size without large spreads, thin order books, or sharp price impact.

Funding liquidity focuses on the financing side. It becomes more important when leverage, collateral, margin requirements, or rollover access start driving market behavior.

Liquidity risk is the possibility that liquidity will not be available when it is needed. The risk can appear through wider spreads, falling depth, forced selling, tighter financing, or weaker market confidence.

A liquidity crisis is more severe than ordinary low liquidity. It describes a stress environment where normal trading or funding channels become impaired and market participants may struggle to transact, finance, or manage risk normally.

A liquidity spiral describes the feedback loop that can emerge when falling prices, weaker collateral, margin pressure, and forced selling reinforce each other. The spiral concept matters because liquidity stress can become self-amplifying instead of staying isolated.

Market Liquidity vs Funding Liquidity

Market liquidity asks whether assets can be traded efficiently. The focus is on spreads, depth, price impact, and the ability to transact without destabilizing the market.

Funding liquidity asks whether participants can obtain or maintain financing. The focus is on credit access, collateral value, leverage, margin pressure, and rollover conditions.

The distinction matters because both can weaken at the same time, but they do not have to start in the same place. A market can trade smoothly while funding conditions are tightening beneath the surface. A market can also show poor trading depth even when broad financing conditions have not fully broken down.

Which Liquidity Question Are You Asking?

| Question | Best starting point |

|---|---|

| What does liquidity mean? | Start with the broad liquidity concept. |

| Can assets be traded without large price impact? | Use market liquidity. |

| Can participants obtain financing? | Use funding liquidity. |

| What happens when liquidity disappears? | Use liquidity risk and liquidity crisis. |

| How do liquidity problems reinforce themselves? | Use liquidity spiral. |

| How can market liquidity be measured? | Use spreads, depth, turnover, volume, and price-impact measures. |

| How does liquidity affect broader markets? | Connect liquidity conditions with risk appetite, volatility, credit, and cross-asset behavior. |

Common False Readings

- Liquidity does not always mean asset prices must rise. Easier liquidity can support risk appetite, but valuation, growth, credit, positioning, and policy expectations still matter.

- High trading volume is not the same as deep liquidity. Volume can rise during stress, while spreads widen and price impact becomes worse.

- Market liquidity and funding liquidity are not interchangeable. Trading access and financing access can deteriorate through different channels.

- A liquidity crisis is not ordinary low liquidity. Crisis conditions involve dysfunction, stress transmission, or impaired access to normal market and funding channels.

- Liquidity indicators are context tools. They can help interpret market conditions, but they are not buy or sell signals.

Related Liquidity and Monetary Conditions Paths

Liquidity sits next to several other market-condition concepts. Central bank liquidity covers policy balance sheets, reserves, quantitative easing, and quantitative tightening. Rates and yield-curve concepts add the discount-rate and policy-expectation layer. Financial conditions and credit conditions add the risk-pricing and borrowing-cost layer.

The cleanest sequence is to separate the liquidity problem first, then connect it to broader monetary conditions. Trading liquidity, funding access, credit stress, policy liquidity, and yield conditions can interact, but each concept answers a different market-structure question.

Next Liquidity Path

Start with the broad liquidity concept when the question is definitional. Move to market liquidity when the issue is trading depth or price impact. Move to funding liquidity when financing, collateral, leverage, or rollover access is the main pressure point. Use liquidity risk, liquidity crisis, and liquidity spiral when the question shifts from normal liquidity conditions to stress behavior.