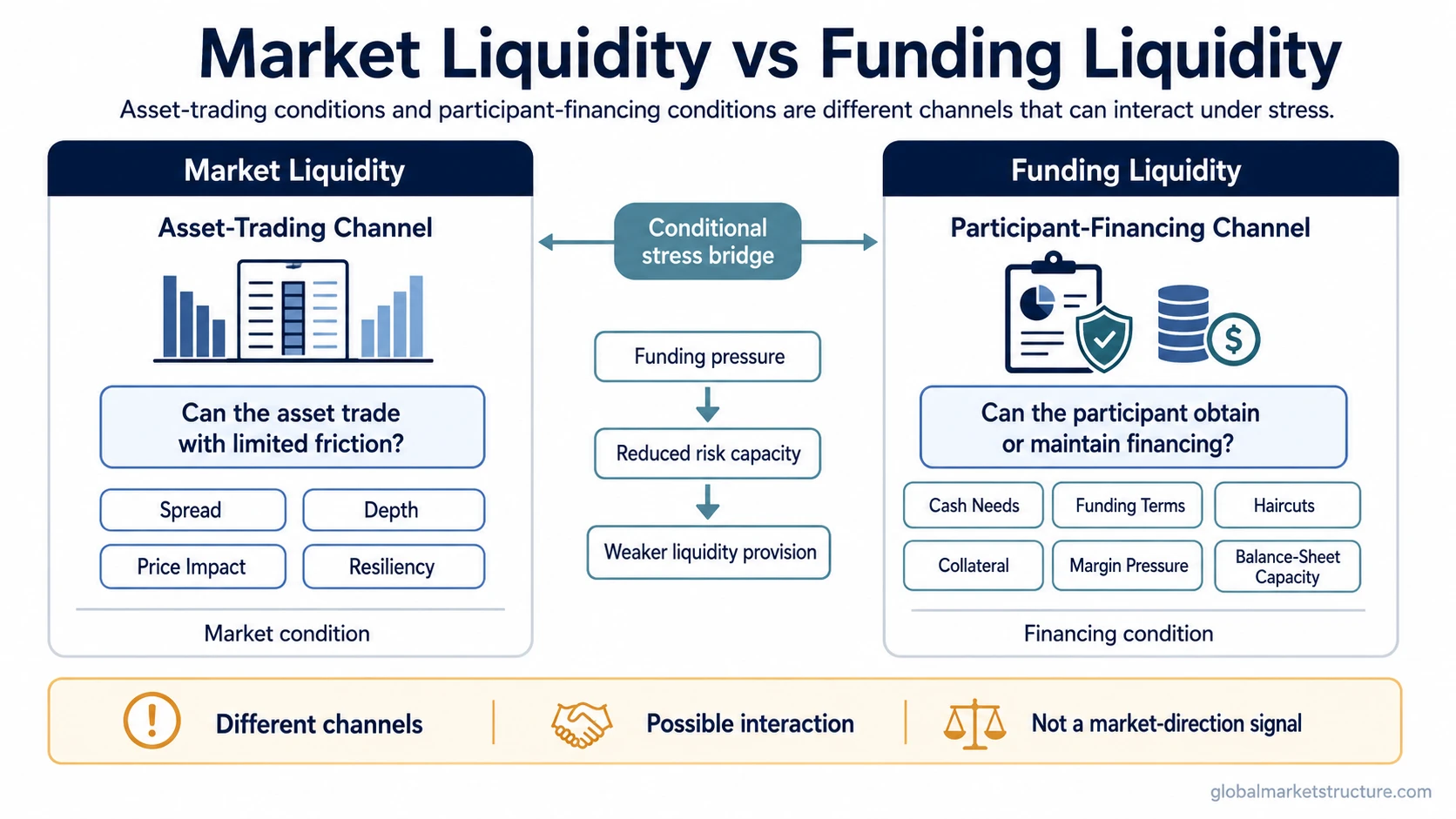

Market liquidity describes the trading conditions around an asset: whether it can be bought or sold quickly, in size, and with limited price impact. Funding liquidity describes the financing conditions around a participant: whether it can obtain, roll, or maintain the cash and credit needed to meet obligations.

The useful distinction is simple: market liquidity is the asset-trading channel, while funding liquidity is the participant-financing channel. The two can interact during stress, but they measure different problems.

Market liquidity vs funding liquidity: the core difference

Market liquidity asks whether an asset can trade without large friction. Funding liquidity asks whether a participant can finance its positions, meet cash needs, roll borrowing, or satisfy collateral demands.

The confusion comes from the word liquidity being used for both. In one case, liquidity describes the trading environment around an asset. In the other, it describes the financing access of a market participant.

| Criteria | Market liquidity | Funding liquidity |

|---|---|---|

| Main object | Asset, order book, or trading venue | Participant, balance sheet, or financing channel |

| Core question | Can the asset be traded without large cost or price impact? | Can the participant obtain, roll, or maintain financing? |

| Stress symptom | Wider spreads, weaker depth, larger price impact, slower execution | Higher funding cost, tighter credit, margin pressure, haircuts, collateral demands |

| Measurement angle | Bid-ask spread, depth, turnover, price impact, resiliency | Funding terms, financing access, collateral requirements, balance-sheet capacity |

| Common false reading | High volume does not always mean strong usable depth | Visible market depth does not prove easy financing |

| Interaction point | Weak funding can reduce liquidity provision | Weak market liquidity can reduce collateral value and increase funding pressure |

What market liquidity describes

Market liquidity is about the ease of trading an asset. A liquid market usually allows participants to buy or sell without moving the price sharply, paying unusually wide spreads, or waiting a long time for execution.

The main focus is the trading channel. Depth, spread, price impact, turnover, and resiliency all describe how well the market absorbs orders.

A market can show high activity and still have weak liquidity if trades require larger price concessions, order-book depth is thin, or prices move sharply for a normal order size.

What funding liquidity describes

Funding liquidity is about access to financing. It concerns the ability of participants to obtain cash, roll short-term funding, post collateral, meet margin calls, or keep positions financed under acceptable terms.

The main focus is the balance-sheet and financing channel. Repo terms, funding costs, haircuts, collateral requirements, margin pressure, and lender willingness all matter more than the visible order book alone.

A participant can face funding pressure even when some markets still look tradable. The issue is not only whether an asset can trade, but whether the participant can finance the position long enough to avoid forced adjustment.

Same stress episode, different liquidity channel

A bond market becomes more volatile. On the market liquidity side, the visible symptoms may be wider bid-ask spreads, thinner depth, and larger price moves for the same order size.

On the funding liquidity side, the pressure may appear through more expensive financing, higher haircuts, tighter repo terms, collateral calls, or reduced balance-sheet capacity.

The same episode can involve both channels, but each channel answers a different question. Market liquidity asks how easily the asset trades. Funding liquidity asks whether the participant can keep financing exposure under the new conditions.

How funding pressure can affect market liquidity

Funding liquidity can affect market liquidity when the participants that normally provide depth face tighter financing conditions. If funding becomes more expensive or collateral demands rise, dealers or leveraged participants may reduce balance-sheet usage.

Under those conditions, available depth can fall and price impact can rise. The transmission path is conditional: funding terms worsen, balance-sheet capacity tightens, liquidity provision weakens, then market depth may fall or price impact may increase.

The mechanism does not mean every funding shock creates immediate market illiquidity. It means financing constraints can reduce the capacity or willingness of some participants to absorb risk.

How to classify the liquidity problem

Asset-trading problem: spreads widen, depth fades, price impact rises, and execution becomes more expensive. That points toward the market liquidity channel.

Participant-financing problem: funding costs rise, collateral terms tighten, margin calls increase, or lenders reduce financing availability. That points toward the funding liquidity channel.

Combined stress problem: funding pressure reduces balance-sheet capacity, which weakens liquidity provision, which can then worsen collateral values or funding needs. That is an interaction between the two channels, not proof that they are identical.

Common false readings

High volume is not enough. Volume can rise during stress while spreads widen, depth thins, and price impact becomes larger.

Tight spreads are not enough. A narrow quoted spread does not always prove that meaningful size can trade without moving the market.

Visible depth does not prove easy funding. An order book can look usable while some participants face tighter financing, higher haircuts, or collateral pressure.

Funding stress is not automatically a crisis. Funding conditions can tighten without immediately producing broad market illiquidity.

Liquidity pressure is not the same as insolvency. A participant can face short-term financing pressure without necessarily being insolvent, and weak market liquidity does not by itself prove balance-sheet failure.

The distinction is not a trading signal. Market liquidity and funding liquidity help classify stress channels. They do not provide a market-direction forecast, timing signal, or execution setup.

When both channels matter together

The strongest liquidity stress usually appears when the trading channel and financing channel reinforce each other. If funding becomes harder, liquidity providers may reduce risk. If market liquidity weakens, collateral values may become harder to realize or finance. That can create a feedback loop under stress.

The safer interpretation is conditional. Market liquidity weakness can make funding pressure more difficult to manage, and funding pressure can reduce market liquidity provision, but the outcome depends on leverage, collateral quality, lender behavior, policy conditions, and market structure.

Key takeaways

- Market liquidity describes whether an asset can trade with limited cost and price impact.

- Funding liquidity describes whether a participant can obtain, roll, or maintain financing.

- The asset-trading channel and participant-financing channel can interact, especially during stress.

- High volume, tight spreads, or visible depth do not fully answer the liquidity question on their own.

- Liquidity stress is a classification problem before it is a crisis, insolvency, or market-direction conclusion.

FAQ

Is market liquidity the same as funding liquidity?

No. Market liquidity is about trading an asset with limited cost and price impact. Funding liquidity is about the ability of a participant to finance positions, meet cash needs, or satisfy collateral demands.

Can market liquidity and funding liquidity weaken at the same time?

Yes. A stress episode can affect both channels. Funding pressure may reduce the capacity to provide market depth, while weaker market liquidity may worsen collateral values or make financing harder to maintain.

Does funding liquidity weakness always mean a crisis?

No. Funding pressure is a stress channel, not an automatic crisis forecast. The outcome depends on the scale of financing pressure, leverage, collateral quality, available backstops, and how market depth responds.

Does high trading volume prove strong market liquidity?

No. High volume can occur during stress. A stronger liquidity reading also needs evidence from spreads, depth, price impact, and the market’s ability to absorb orders without severe disruption.