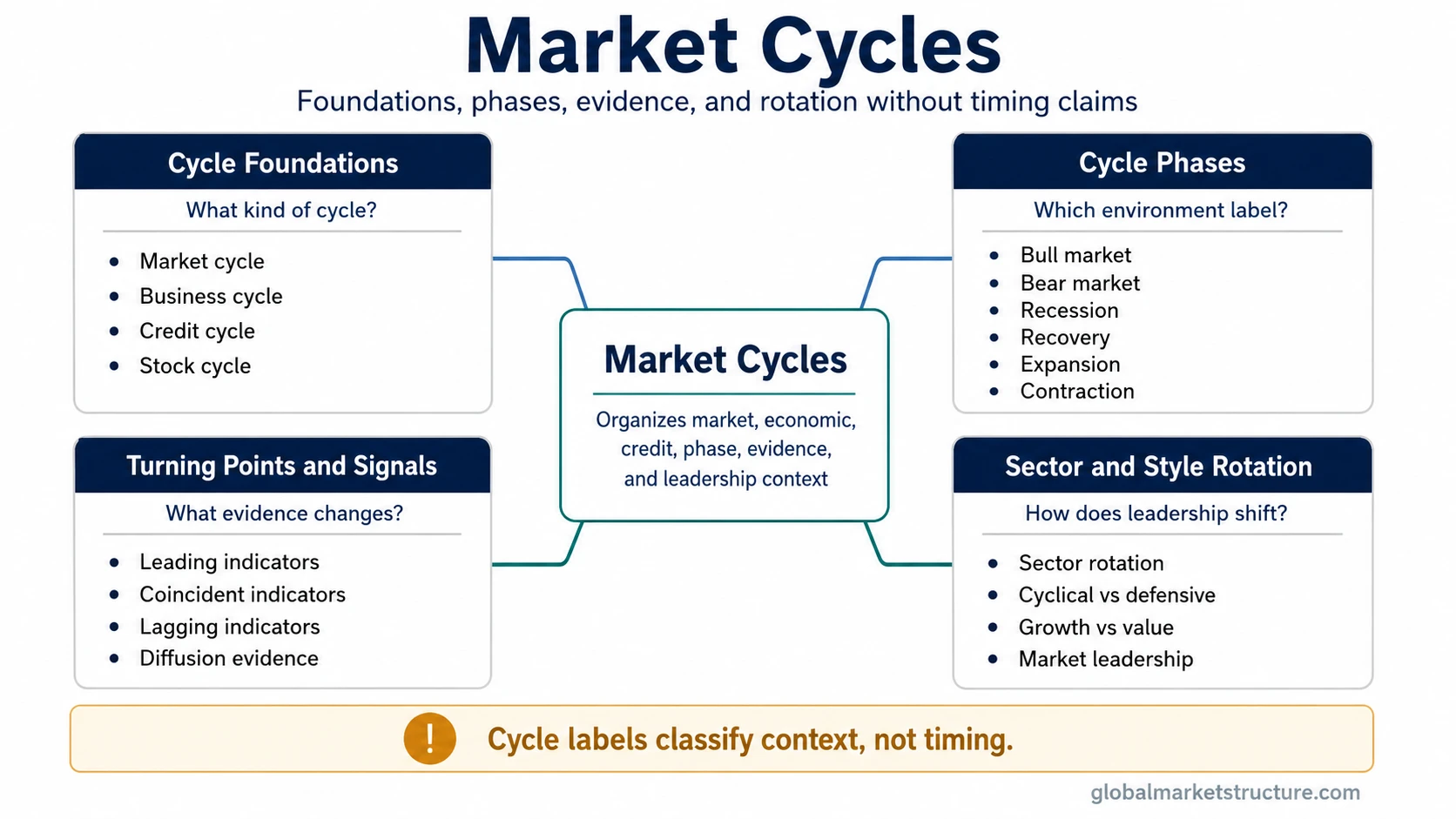

Market cycles group several related ideas: broad cycle concepts, economic and credit-cycle context, phase labels, turning-point evidence, and leadership rotation. The useful starting point depends on the question being asked. A cycle label can organize evidence, but it does not create a fixed timing rule, recession forecast, or buy/sell signal.

Choose the right market-cycle path

| Question | Best starting point | What it clarifies |

|---|---|---|

| What kind of cycle is being discussed? | Cycle Foundations | Market cycle, business cycle, credit cycle, stock cycle, and boom-and-bust distinctions. |

| Which phase label fits the environment? | Cycle Phases | Bull, bear, recession, recovery, expansion, contraction, peak, and trough vocabulary. |

| What evidence changes the cycle reading? | Turning Points and Signals | Leading, coincident, lagging, and diffusion evidence used to classify change. |

| How does leadership shift across cycles? | Sector and Style Rotation | Sector rotation, style rotation, cyclicals, defensives, growth, value, and market leadership. |

Market cycle foundations

Cycle foundations separate the broad cycle idea from nearby concepts that are often mixed together. A market cycle describes recurring changes in market behavior and risk appetite, while a business cycle describes changes in economic activity. A credit cycle focuses on borrowing conditions, lending standards, and balance-sheet pressure.

Use this path for: questions about whether the discussion is centered on markets, the economy, credit, stocks, or boom-and-bust dynamics.

Cycle phases

Cycle phases give names to changing environments, but phase labels are not timing tools by themselves. A bull market and a bear market describe broad market direction and behavior. Economic phase labels such as recession, recovery, expansion, contraction, peak, and trough describe different points in the economic cycle.

Use this path for: questions about phase vocabulary, broad cycle position, or the difference between market-phase labels and economic-phase labels.

Turning points and signals

Turning-point evidence helps organize whether conditions are improving, weakening, confirming, or lagging. A leading indicator may change before the broader environment is visible in headline data. A coincident indicator moves closer to the current environment, while a lagging indicator often confirms what has already developed.

Use this path for: questions about evidence quality, indicator timing, confirmation, or whether a cycle reading is early, current, or delayed.

Sector and style rotation

Sector and style rotation connects cycle interpretation with market leadership. Sector rotation tracks how leadership can move between areas such as cyclical sectors and defensive sectors. Style rotation tracks changes between groups such as growth stocks and value stocks. These shifts can add context, but they do not create a mechanical playbook.

Use this path for: questions about how leadership, sector behavior, or growth-versus-value behavior fits into a broader cycle reading.

Market-cycle limits

Market cycles are classification tools, not precise clocks. The same phase label can carry different meaning depending on credit conditions, liquidity, earnings pressure, policy response, breadth, and leadership quality. Cycle evidence becomes more useful when multiple signals point in the same direction, and weaker when one label is treated as a standalone prediction.

How to choose the next concept

Start with foundations when the question is about what type of cycle is being discussed. Use phases when the question is about environment labels. Use turning-point signals when the question is about evidence quality. Use sector and style rotation when the question is about leadership changes across the cycle.