Cycle phases organize the main labels used to describe market-cycle and business-cycle conditions. The right label depends on the question: bull or bear markets for broad asset direction, expansion or contraction for economic activity, peak or trough for turning points, and recession or depression for downturn severity. A cycle label is contextual. It does not confirm timing, market tops, market bottoms, recession probability, allocation action, or trade direction.

Scope boundary: Cycle labels classify conditions. They do not prove what markets will do next. The same label can mean different things depending on macro data, liquidity conditions, credit, breadth, rates, and cross-asset confirmation.

How to Use Cycle Phase Labels

Cycle phase language is useful when the question is clearly defined. A market-direction question belongs to broad asset-market labels. An economic-activity question belongs to business-cycle labels. A turning-point question belongs to peak and trough labels. A downturn-severity question belongs to recession and depression labels.

The most common mistake is treating every cycle label as a timing call. A label can organize evidence, but it cannot identify an exact market top, exact market bottom, next policy move, or correct portfolio action by itself.

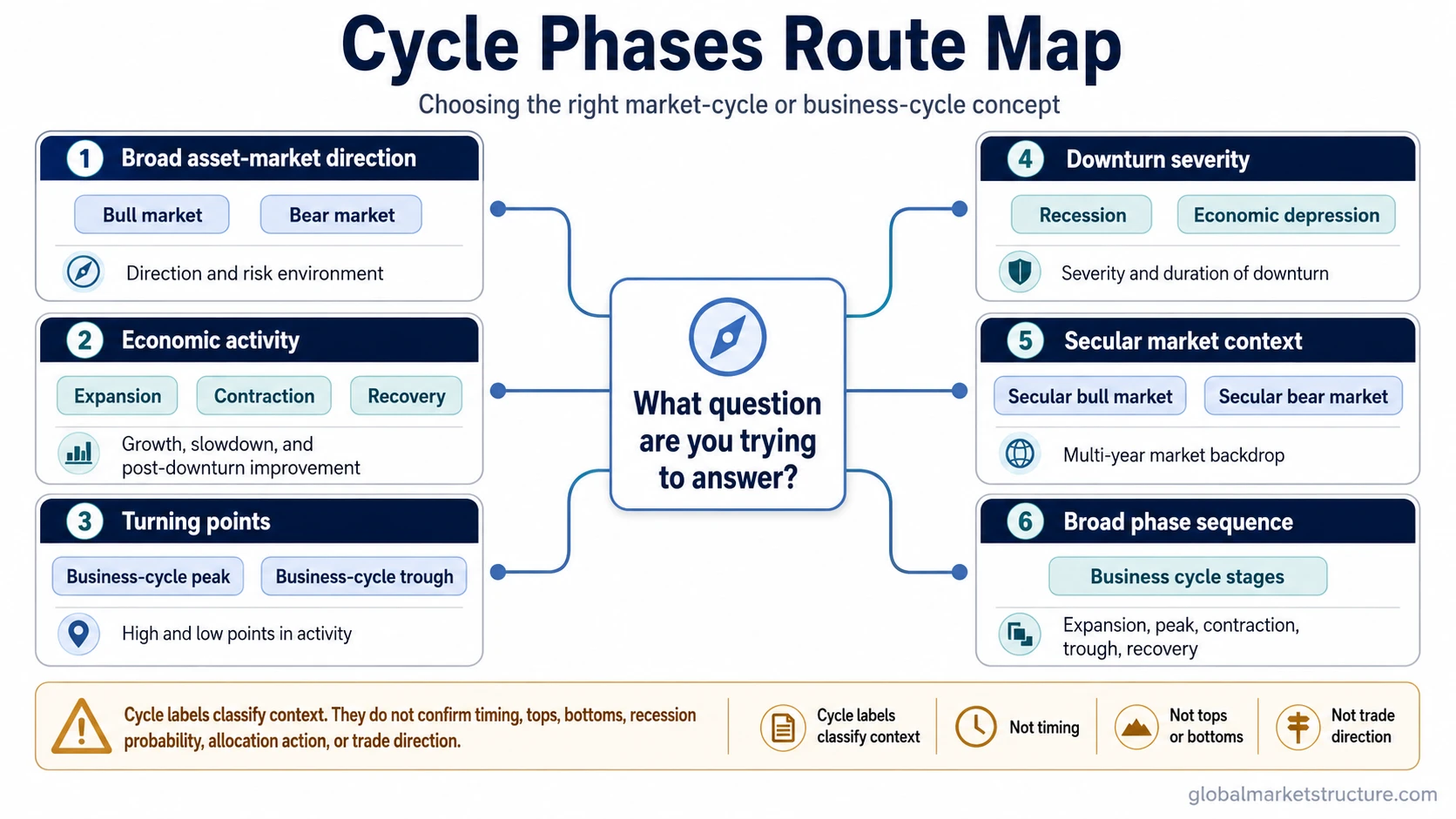

Choose the Right Cycle Phase Concept

The starting point depends on the question being asked. Broad market direction, economic activity, turning points, downturn severity, and secular market context use different labels.

| Question | Best concept | What it owns | What it does not prove |

|---|---|---|---|

| Is the broad asset-market environment rising or falling? | Bull market or bear market | Broad asset-market direction and risk environment | Exact entry, exit, top, or bottom |

| Is the long-horizon market backdrop favorable or difficult? | Secular bull market or secular bear market | Longer-horizon market environment | Short-term timing or near-term trade direction |

| Is economic activity broadly increasing? | Expansion | Growth-phase interpretation in the business cycle | Guaranteed equity returns or risk-asset strength |

| Is economic activity weakening? | Contraction | Slowdown or shrinking activity within the economic cycle | Automatic recession classification or market direction |

| Is activity improving after a downturn? | Recovery | Post-downturn improvement and early normalization | A completed expansion or confirmed risk-on regime |

| Is the downturn broad enough to classify as recession? | Recession | Broad economic downturn classification | Exact market bottom, asset allocation, or policy path |

| Is the downturn unusually severe and prolonged? | Economic depression | Severe downturn classification | Ordinary slowdown labeling or routine recession framing |

| Is the cycle near a high point in activity? | Business-cycle peak | High-point label in a business-cycle sequence | Exact stock-market top confirmation |

| Is the cycle near a low point in activity? | Business-cycle trough | Low-point label in a business-cycle sequence | Exact stock-market bottom confirmation |

| Is the broad phase sequence needed first? | Business cycle stages | The common expansion, peak, contraction, trough, and recovery sequence | A full explanation of every market-cycle label |

Market-Cycle Phase Labels

Market-cycle labels focus on broad asset-market behavior. A bull market describes a rising market environment, while a bear market describes a broad decline or risk-off environment. These labels are about market direction and participation, not exact timing.

Longer-horizon environments need a separate lens. A secular bull market and a secular bear market describe multi-year market backdrops where valuation, earnings, inflation, rates, liquidity, and investor behavior can reinforce a broader trend. They should not be reduced to short-term chart direction.

Useful distinction: A cyclical bull market can occur inside a larger secular bear market, and a cyclical bear market can occur inside a larger secular bull market. The time horizon matters before the label becomes useful.

Business-Cycle and Economic Activity Labels

Business-cycle labels focus on economic activity rather than asset direction. Expansion, contraction, and recovery describe changes in output, employment, income, spending, production, or broader activity conditions. These labels can influence market interpretation, but they are not the same as bull or bear market labels.

Expansion describes a phase of improving or growing economic activity. Contraction describes weakening or shrinking activity. Recovery describes improvement after a downturn, when conditions are no longer deteriorating in the same way but may not yet resemble a mature expansion.

Business cycle stages separate expansion, peak, contraction, trough, and recovery into a single sequence. That sequence is useful as an orientation layer, while individual phase concepts carry the more precise meaning.

Turning Points and Downturn Severity

Peak and trough labels describe turning points in a business-cycle framework. A business-cycle peak marks a high point in economic activity before deterioration becomes visible. A business-cycle trough marks a low point before activity begins to improve. Neither label automatically confirms a stock-market top or bottom.

Downturn labels answer a different question. A recession describes a broad economic downturn. An economic depression describes a much more severe and prolonged downturn. The distinction matters because severity labels require stronger evidence than a simple slowdown or weak market period.

When the main confusion is severity, recession vs depression separates an ordinary recession framework from a much deeper economic breakdown. When the main confusion is market direction, bull market vs bear market separates positive and negative asset-market environments.

What Cycle Labels Do Not Prove

A cycle phase label is a classification tool. It can help organize evidence, but it does not prove exact timing, confirm a top or bottom, forecast a recession, determine allocation, or create a trade signal.

The label becomes more useful only when it is interpreted with supporting evidence. Macro data, liquidity conditions, market breadth, credit spreads, rates, earnings expectations, policy direction, and cross-asset behavior can all change how a phase label should be read.

A market can rise during parts of an economic slowdown. A recovery can begin before confidence fully returns. A bear market can appear without a formal recession. A recession can be recognized after markets have already repriced part of the risk. The label is the start of classification, not the end of analysis.

Where to Go Next

Start with the label that matches the question. For market direction, use bull and bear market concepts. For economic activity, use expansion, contraction, and recovery. For turning points, use peak and trough. For downturn severity, use recession and economic depression. For longer-horizon context, use secular bull and secular bear market labels.

Cycle-phase analysis works best when labels stay separated by purpose. Market labels, economic labels, turning-point labels, downturn labels, and secular labels can overlap in real conditions, but they do not answer the same question.