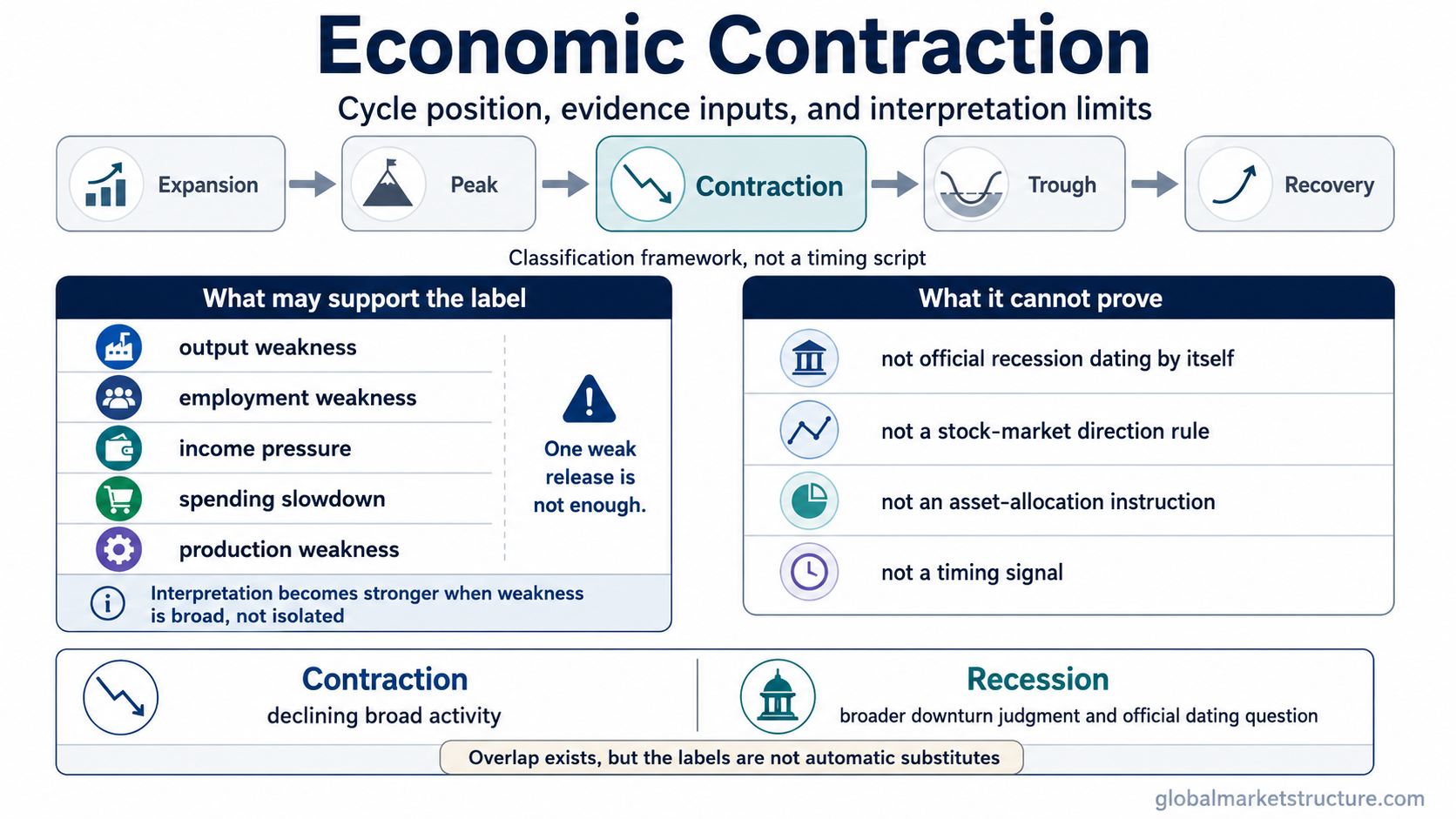

Economic contraction is a phase in which broad economic activity is declining. In business-cycle terms, it refers to a downswing that can show up through weaker output, employment, income, spending, production, or other economy-wide measures. The label can help classify macro conditions, but it does not automatically confirm a recession, predict stock-market direction, determine asset allocation, or function as a trade signal.

A useful distinction is that contraction is strongest as a broad-activity label. It becomes less reliable when readers treat one weak data release, one GDP print, or one market move as a complete cycle judgment.

Key Points

- Economic contraction refers to declining broad economic activity.

- It usually sits on the downswing of the business cycle.

- It can overlap with recession language, but the two labels are not identical in every use case.

- The concept can describe macro context, but it cannot prove market direction or portfolio action on its own.

Where Economic Contraction Sits in the Business Cycle

Economic contraction usually refers to the phase that follows expansion. Broad activity is no longer strengthening across the economy, and incoming evidence begins to weaken rather than improve.

The phase is often discussed after a business-cycle peak, when growth has already reached a high point and the main question shifts from how strong activity is to how broad and persistent the slowdown may become.

A simple sequence is expansion, peak, contraction, trough, and recovery. Real economies rarely move through those labels in a perfectly clean line, so the sequence is best treated as a classification framework rather than a mechanical timing script.

Observable Evidence That May Support the Label

Economic contraction is usually supported by a pattern of weaker broad activity, not by one statistic in isolation. The practical question is whether weakness is appearing across several economy-wide inputs at roughly the same time.

| Evidence input | What it may suggest | What it cannot prove alone |

|---|---|---|

| Output, GDP, or production weakness | Overall activity may be slowing or shrinking | It cannot settle the full cycle classification by itself |

| Employment weakness | Labor demand may be softening | It does not prove that the whole economy is already in a recession |

| Income pressure | Household or business conditions may be deteriorating | It cannot determine market direction on its own |

| Spending or demand decline | Consumption or broader demand may be losing momentum | It does not prove how long the slowdown will last |

| Industrial production or other broad-activity weakness | The slowdown may be spreading beyond one narrow area | It cannot confirm the exact turning point in real time |

| Multi-indicator deterioration | The contraction reading becomes more credible | It still does not create a trading signal or asset-allocation rule |

This distinction matters because isolated weakness can reflect noise, timing effects, or sector-specific problems. The interpretation becomes stronger when several broad indicators weaken together.

Economic Contraction vs Recession

| Aspect | Economic contraction | Recession |

|---|---|---|

| Core idea | Declining broad economic activity | Recession is a broader downturn classification that is often discussed with more attention to depth, diffusion, duration, and official dating. |

| Interpretation threshold | Can describe weakening activity before a stronger downturn label is adopted | Usually asks for a broader judgment about how extensive and established the weakness has become |

| What one weak GDP print cannot do | It cannot settle the full cycle classification | It does not automatically settle the broader downturn judgment either |

In practical terms, contraction helps describe what the activity trend looks like. Recession asks for a broader judgment about how extensive and established that weakness has become.

What the Label Cannot Prove

Economic contraction can describe a weakening phase in broad activity, but it cannot prove that the economy has already reached an officially dated recession, that asset prices must fall next, or that the cycle has already reached a business-cycle trough.

It also cannot tell you how long the downswing will last. Markets can move on expectations, policy shifts, liquidity conditions, valuation changes, and timing effects long before a macro label becomes widely accepted.

Common False Readings

| False reading | Safer interpretation |

|---|---|

| Reading one data point as the whole cycle | A weak release can matter, but contraction is a broad-activity concept. The reading becomes more defensible when weakness is visible across multiple measures. |

| Turning a macro label into a market call | Even if contraction risk is rising, that does not create a reliable stock-market direction rule. Macro classification and market pricing are related, but they are not identical. |

| Assuming the phase reveals the full path ahead | Contraction can help describe where the economy may be in the cycle, but it does not reveal the exact timing of the low point or what the recovery path must look like. |

Related Cycle-Phase Concepts

Expansion usually comes before the downswing, and the peak marks the high point before activity weakens. Recession is the broader downturn label, business-cycle trough is the low point that can follow the downswing, and recovery marks the improvement phase after that low point.