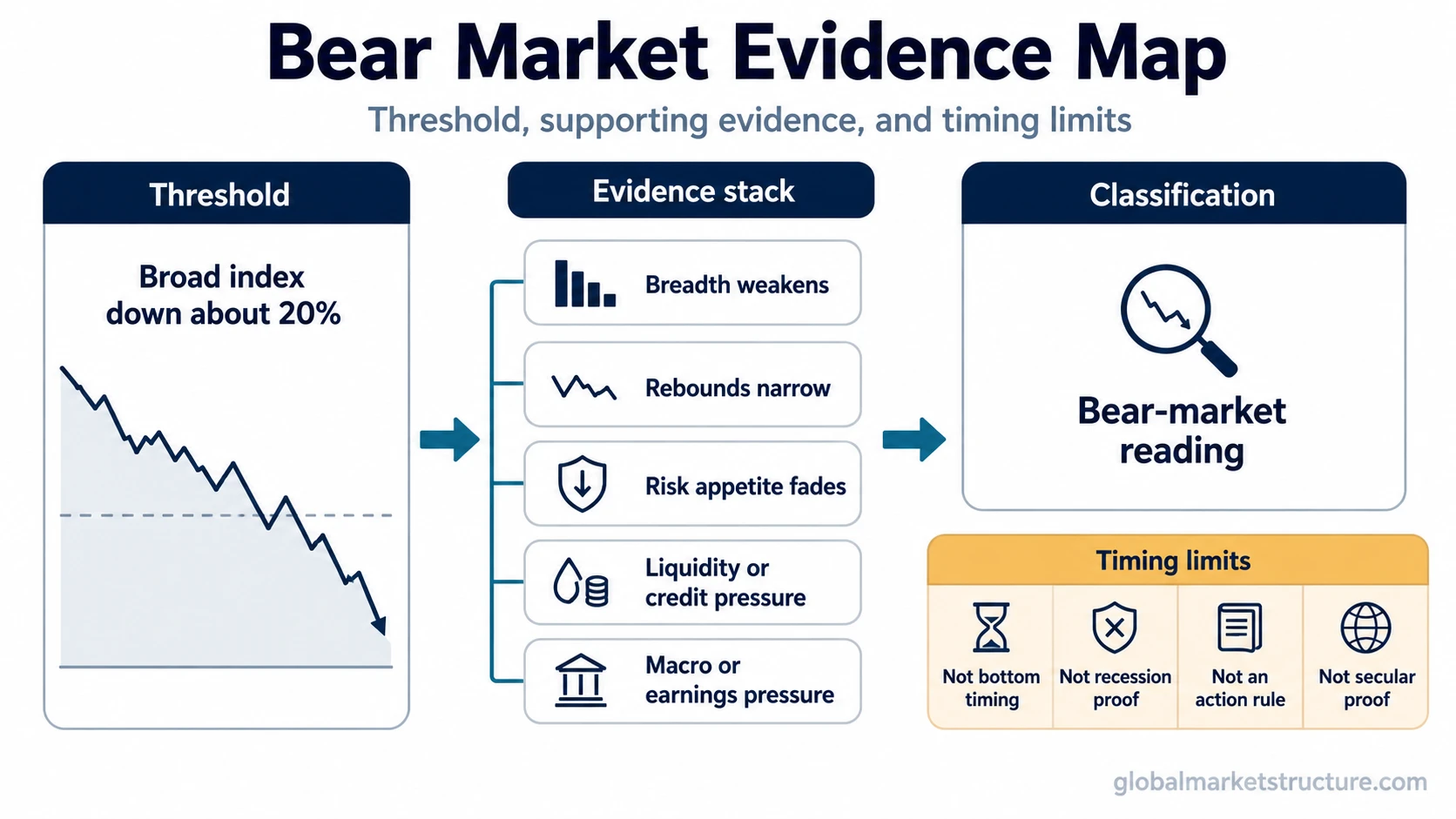

A bear market is a broad decline in market prices, commonly associated with a broad market index falling about 20% or more from recent highs. The label describes market weakness, weaker sentiment, and risk aversion, but it does not identify a bottom, confirm a recession, or create a buy/sell signal.

Key points:

- A bear market describes broad market weakness, not just a bad day or one weak stock.

- The common convention is a decline of about 20% or more from recent highs in a broad market index.

- Breadth, failed rebounds, risk appetite, liquidity, credit, earnings, and macro context can strengthen or weaken the classification.

- The label is descriptive, not a recession call, bottom signal, recovery timer, or investment instruction.

What qualifies as a bear market?

A bear market usually refers to a broad decline in a major market or broad market index, not an isolated decline in a single stock. The common threshold is a fall of about 20% or more from recent highs, especially when the decline reflects wider weakness across sectors, risk assets, or investor participation.

The 20% threshold is useful because it gives the term a recognizable boundary. It is not a complete market framework. A market can touch bear-market territory without every internal signal confirming deep regime damage, and a market can show deteriorating conditions before the threshold is officially reached.

The stronger classification comes from the combination of price decline, weaker breadth, reduced risk appetite, lower-quality rebounds, and pressure in liquidity, credit, earnings, or macro conditions where those forces are relevant.

Why the 20% threshold is useful but incomplete

The 20% convention helps separate a normal pullback from a deeper market decline. It gives investors and analysts a shared reference point, especially when discussing broad market indices.

The limitation is that markets do not change character only because a round-number threshold has been crossed. A decline just below the threshold with weakening breadth and tighter financial conditions may be more fragile than a slightly deeper decline where participation is already stabilizing. The threshold marks territory; the surrounding evidence shapes interpretation.

Important limitation: A bear-market label is usually clearer after price damage has already occurred. It can describe a market condition, but it cannot by itself forecast the next decline, confirm the final low, or define what any individual investor should do.

The evidence stack behind a bear-market reading

A bear-market reading becomes more useful when the price decline is checked against market structure and risk conditions. The goal is not to find a mechanical signal. The goal is to separate a broad risk-off environment from a shallow correction or short-lived volatility shock.

- Price: A broad index falls toward or beyond the common 20% convention from recent highs.

- Trend structure: Lower highs, lower lows, and weak rebound attempts show persistent pressure.

- Breadth: Fewer sectors, industries, or stocks participate in rebounds.

- Risk appetite: Investors become less willing to hold higher-risk assets or pay high valuation premiums.

- Liquidity and credit: Tighter funding, wider spreads, or weaker financing conditions can reinforce the risk-off environment.

- Macro and earnings context: Slowing growth, margin pressure, or weaker earnings expectations can add pressure when they align with price and breadth deterioration.

- Rebound quality: Bear markets can include sharp rebounds or relief rallies, so one rebound is not enough by itself to confirm that broader weakness has ended.

Bear-market evidence can classify conditions without proving a signal

Bear-market evidence can support classification, but each signal has a limit. The same evidence that helps describe broad weakness can be misread if it is treated as a timing tool or trading rule.

| Evidence | Helps classify | Cannot establish by itself |

|---|---|---|

| Broad index down about 20% | Bear-market territory by common convention | Exact bottom, recovery timing, or required action |

| Weak breadth | Participation damage beneath the index level | A guaranteed recession or fixed market path |

| Risk-aversion shift | Pressure on sentiment, positioning, and valuation tolerance | A buy, sell, short, or hedge instruction |

| Credit or liquidity stress | Financial-condition strain that can reinforce broad weakness | A mechanical outcome for stocks or the economy |

| Relief rally | A temporary rebound inside a weak environment | Confirmation that the bear market has ended |

Bear market vs correction

A correction is usually a smaller market decline than the common bear-market convention. It often describes a pullback from recent highs that may be sharp but does not necessarily imply broad, persistent regime deterioration.

A bear market usually points to deeper and broader weakness. The distinction is not only the size of the decline. Breadth, failed rebounds, sentiment damage, and risk conditions help determine whether the market is simply correcting or moving through a more durable risk-off phase.

Bear market vs recession

A bear market describes financial-market price weakness. A recession describes a significant decline in economic activity that is spread across the economy and lasts more than a few months. They can overlap, but one does not automatically prove the other.

Markets can fall sharply because investors are discounting weaker growth, tighter liquidity, lower earnings expectations, or valuation pressure. Economic contraction is a separate classification that depends on economic data, not only asset prices.

The practical mistake is treating a bear-market label as a recession forecast. A bear market can increase concern about the economic backdrop, but it does not replace economic evidence.

Bear market vs bull market

A bull market describes a rising broad-market condition where risk appetite, participation, and investor confidence are generally stronger. A bear market describes a falling broad-market condition where risk aversion, weak breadth, and lower confidence usually matter more.

The direct contrast belongs to bull market vs bear market, where the two environments can be separated across price behavior, sentiment, breadth, and cycle interpretation.

Cyclical bear market vs secular bear market

A normal bear-market label usually describes a major decline within a market cycle. A secular bear market describes a longer structural regime where broad returns, valuations, or inflation-adjusted performance can remain pressured across a much longer period.

A 20% decline does not automatically establish a secular bear market. The longer regime question requires broader evidence around valuation, real returns, inflation, policy conditions, earnings durability, and repeated failure to sustain long-term progress.

A practical bear-market scenario

A broad index falls more than 20% from its recent high. Rebound attempts become narrower, fewer sectors participate, and investors shift toward safer assets. Credit conditions also begin to tighten, while earnings expectations weaken.

That combination can support a bear-market classification because price, breadth, risk appetite, and financial conditions are pointing in the same direction. It still cannot establish that a recession has started, that the final low is close, or that a specific investment action is required.

Timing limits and common false readings

Bear-market labels are often descriptive rather than predictive. By the time a market is widely called a bear market, a meaningful part of the decline may already have occurred. That makes the label useful for classification, but weak as a standalone timing tool.

Common false readings:

- A bear market does not automatically mean a recession has started.

- A bear market does not confirm that the bottom is near.

- A relief rally is not enough to confirm that broader weakness has ended.

- A 20% decline is not enough to establish a secular bear regime.

- A bear-market label does not tell investors what to buy, sell, short, hedge, or hold.

The safer interpretation is classification-first. The label can describe broad market weakness, while separate evidence is needed for recession risk, recovery quality, secular regime analysis, and portfolio decisions.

FAQ

Is a bear market always a recession?

No. A bear market describes financial-market price weakness, while a recession describes a significant decline in economic activity. They can overlap, but a market decline does not automatically prove recession.

Is a 20% decline enough to define a bear market?

A decline of about 20% or more in a broad market index is the common convention. The interpretation becomes stronger when breadth, sentiment, risk appetite, liquidity, credit, or earnings evidence also points to broad weakness.

Can a bear market have rallies?

Yes. Bear markets can include sharp rebounds or relief rallies. A rally becomes more meaningful when participation broadens, risk appetite improves, and the market stops making weaker rebound attempts.

What is the difference between a correction and a bear market?

A correction is usually a smaller decline from recent highs. A bear market usually involves deeper, broader, and more persistent weakness, often with weaker breadth and more defensive investor behavior.