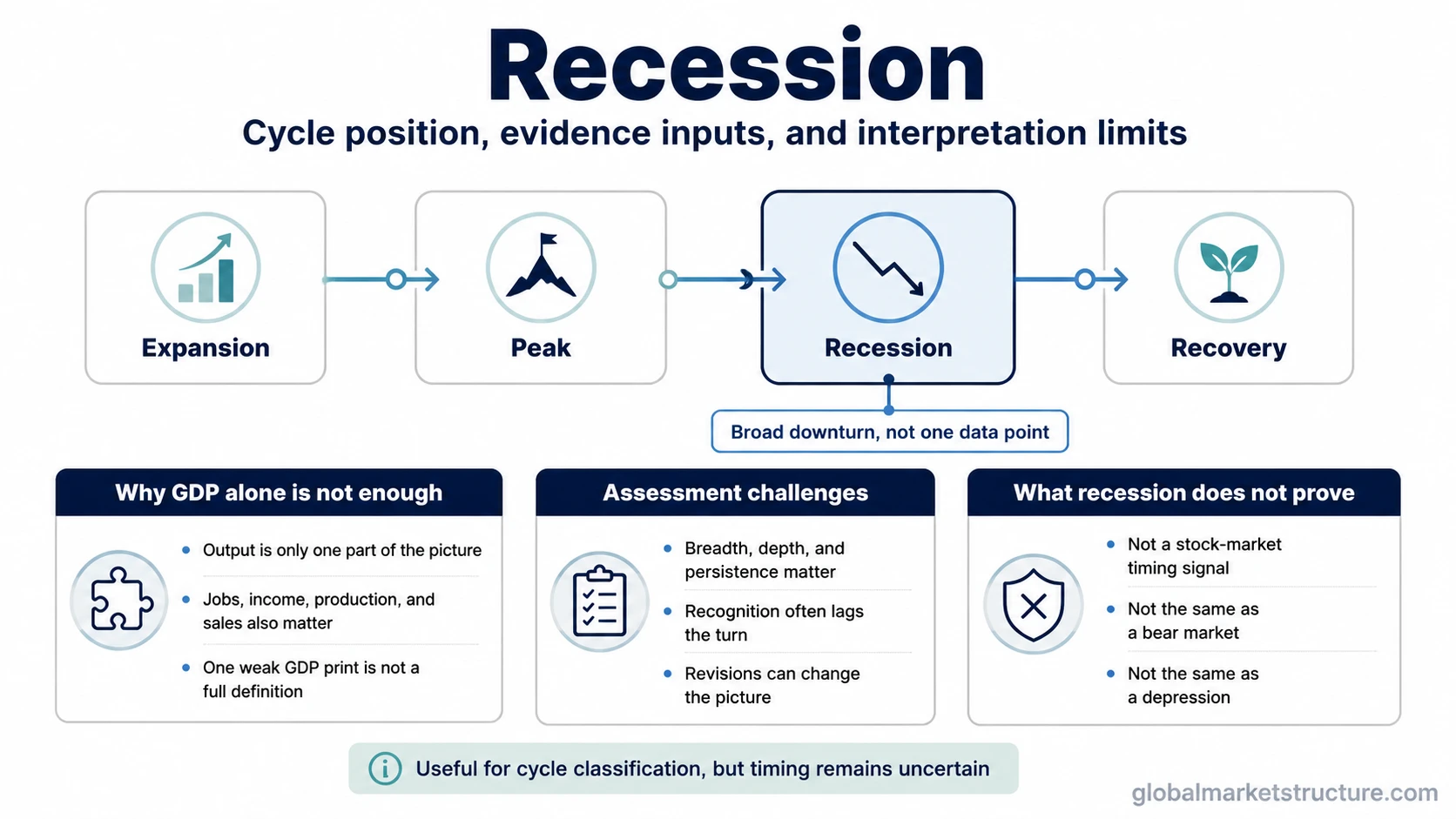

A recession is a broad-based decline in economic activity across an economy. It is not defined by GDP alone, it is often recognized only after the turn has started, and it should not be treated as a shortcut for predicting the next market move.

In practice, the label is used for a downturn that shows up across several parts of economic activity rather than in one headline release. That is why narrow shorthand can be useful for discussion but too weak as a full definition.

Quick boundary

- A recession refers to a broad economic downturn, not a single data point.

- Two negative GDP quarters can be a warning sign, but not a complete test on their own.

- Recognition often lags because the broader downturn becomes clearer only as more evidence accumulates.

- The term describes an economic phase, not an automatic instruction about prices, portfolios, or positioning.

Why GDP alone is not enough

GDP gets attention because it is broad and easy to quote, but recession classification usually looks beyond one output measure. Employment, real income, industrial production, and sales can all matter because downturns do not always show up in the same way or at the same speed.

A strict GDP-only rule can therefore miss the larger picture in both directions. A weak GDP print does not automatically prove recession, and a broader downturn can be developing even before a simple shorthand feels decisive.

| Reading approach | What it captures | Main limit |

|---|---|---|

| GDP-only shorthand | A quick output-based signal | Too narrow to stand as a full recession definition |

| Broader activity view | Output, jobs, income, production, and sales together | Clearer, but often slower and less certain in real time |

How recession classification is assessed and dated

Recession classification is usually an exercise in judging whether a downturn is broad enough, deep enough, and persistent enough to count as a real cycle phase rather than a brief soft patch. That makes timing harder than the headline term suggests.

The key point is that recession dating is often clearer in hindsight than in the moment. Incoming data can be incomplete, later revisions can change the picture, and turning points rarely announce themselves cleanly on one day. That makes the label useful for understanding the cycle, but too blunt to use as a mechanical timing tool for markets.

Limitation: A recession label often lags the turn. It can help classify the cycle, but it does not remove uncertainty about when the downturn started, how deep it will become, or what markets will do next.

What recession is not

The term often gets pulled into market language, but it answers a different question from a bear market. Recession describes the economy, while a bear market describes a large decline in asset prices. The two can overlap, but they do not have to begin, end, or unfold on the same schedule.

Severity creates a second common confusion. The distinction between recession and depression matters because depression implies a more severe and prolonged collapse, while recession is the broader label for an economy-wide downturn that does not automatically reach that extreme.

The label also should not be treated as a trading or allocation signal. It classifies a phase in economic activity. By itself, it does not tell you the next move in stocks, bonds, credit, or any other market.

How recessions can emerge

Recessions can emerge through different channels. Demand can weaken, credit conditions can tighten, policy can become restrictive, inventories can correct sharply, or an external shock can hit production and spending. The exact mix changes from cycle to cycle, which is another reason one fixed rule is usually too crude.

Those channels are best treated as context rather than as a checklist that guarantees a downturn. Some slowdowns stay shallow, some spread more broadly, and some reverse before they become a full recession phase.

Illustrative scenario: GDP is flat to slightly negative for a short period, but payroll growth is weakening, real income is under pressure, industrial production is softening, and sales are fading. That mix does not prove recession from one release, yet it shows why a broader activity view is more useful than GDP shorthand alone.

Where recession sits in the cycle

In cycle terms, recession is the contraction phase where the downturn becomes broad enough to be recognized as more than normal volatility. What follows is usually recovery, although the handoff between the two is rarely obvious in real time.

That transition matters because the economy and markets do not wait for clean labels. Prices can move before the economic record is settled, while the official understanding of the downturn may arrive later.

Related next steps: use the bear-market distinction if the question is about asset prices, use the recession-versus-depression comparison if the question is about severity, and use stagflation and recession if the main issue is weak growth combined with persistent inflation pressure.