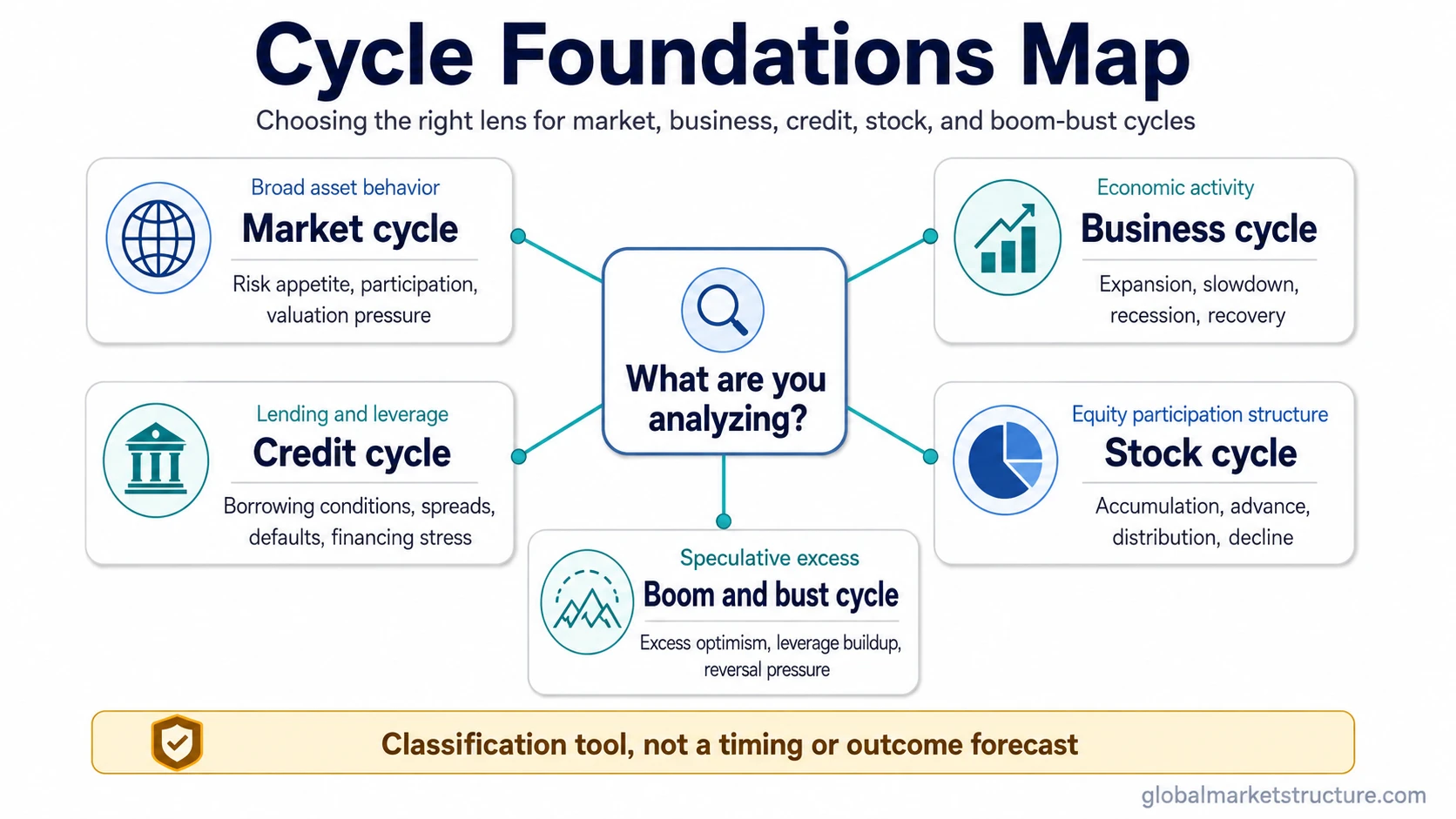

Cycle Foundations separates the main cycle concepts used in market-structure analysis: market cycles, business cycles, credit cycles, stock cycles, and boom-bust dynamics. Each concept answers a different question. Some describe broad asset behavior, some describe economic activity, some describe credit availability, and some describe speculative excess. Cycle labels help classify conditions, but they do not forecast timing on their own.

How the Core Cycle Concepts Differ

Cycle analysis becomes clearer when the first distinction is made before interpretation begins. A market cycle is not the same as a business cycle. A credit cycle is not the same as an equity-market cycle. A boom-bust cycle describes speculative expansion and reversal pressure, not every normal rise and fall in asset prices.

The useful starting point is to identify the process being analyzed. After that, the specific cycle concept can explain the mechanism, common signals, interpretation limits, and related market conditions.

Core Cycle Concepts

| Concept | Best use | Go deeper |

|---|---|---|

| Market cycle | Use for broad asset-market behavior, risk appetite, valuation pressure, and changes in market participation. | Market cycle |

| Business cycle | Use for economic activity, expansion, slowdown, recession, recovery, employment, and output conditions. | Business cycle |

| Credit cycle | Use for lending conditions, leverage, defaults, credit spreads, financing stress, and the availability of credit. | Credit cycle |

| Stock cycle | Use for equity-market structure that can be analyzed through accumulation, advance, distribution, and decline. | Stock cycle |

| Boom and bust cycle | Use for speculative expansion, excess optimism, leverage buildup, reversal pressure, and unwind dynamics. | Boom and bust cycle |

Which Cycle Concept Fits the Question?

The right cycle lens depends on the object being analyzed. A question about GDP and employment belongs closer to the business cycle. A question about borrowing, spreads, and defaults belongs closer to the credit cycle. A question about equity-market behavior belongs closer to the stock cycle or market cycle, depending on the breadth of the issue.

| Question | Best destination | Reason |

|---|---|---|

| What type of broad cycle are markets moving through? | Market cycle | Market-cycle analysis focuses on asset behavior and risk appetite rather than only the real economy. |

| How does the economy move through expansion and contraction? | Business cycle | Business-cycle analysis focuses on economic activity, growth, recession, recovery, and macro phases. |

| How do lending conditions and leverage change across time? | Credit cycle | Credit-cycle analysis focuses on financing availability, debt conditions, and stress in credit markets. |

| How can equity-market structure be classified? | Stock cycle | Stock-cycle analysis focuses on equity behavior and participation phases, not broad economic-cycle dating. |

| When does expansion become vulnerable to a sharp unwind? | Boom and bust cycle | Boom-bust analysis focuses on speculative excess, reversal pressure, and the transition from expansion to unwind. |

Cycle Type Is Not the Same as Cycle Phase

A cycle type identifies what is being analyzed. A cycle phase describes where that process may be within a sequence. Confusing the two can create weak interpretation. For example, a business-cycle slowdown and an equity-market distribution phase may overlap, but they do not measure the same thing.

This distinction also limits how cycle labels should be used. A label can organize evidence, but it does not independently prove recession timing, inflation durability, policy direction, yields, equity returns, credit-spread movement, FX behavior, or risk appetite.

What Cycle Labels Cannot Confirm Alone

Cycle labels are classification tools, not standalone forecasts. They become more useful when combined with observable evidence such as credit conditions, liquidity pressure, breadth, sector leadership, policy stance, cross-asset behavior, and economic data. Without that evidence, a cycle label can describe a possible context but not confirm timing or outcome.

Related Boundary Path

The closest comparison route is market cycle vs business cycle. That distinction is useful when the question is whether the analysis is about broad asset-market behavior or the real economy. Other weak or unvalidated cycle labels should remain supporting context unless later evidence confirms a separate page role.

How to Choose the Right Cycle Lens

Start with the object of analysis: market behavior, economic activity, credit availability, equity structure, or speculative excess. The correct cycle concept depends on that object. The specific cycle concepts should carry the main explanatory weight, while this distinction keeps the first decision clear before interpretation expands.