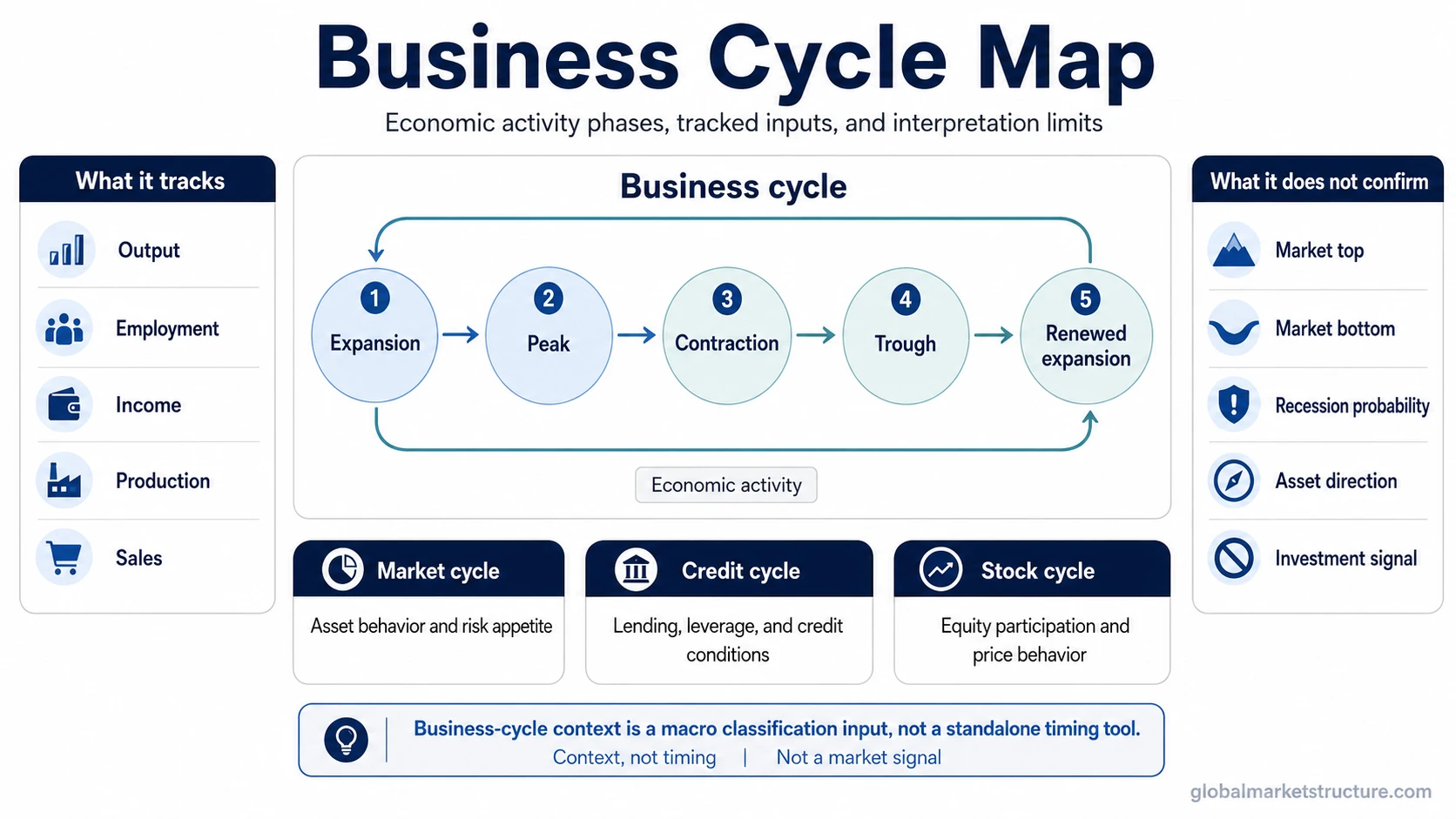

A business cycle describes the broad expansion and contraction of economic activity. It helps classify the macro backdrop, but it does not identify the exact timing of a market top, market bottom, recession call, or asset-price move by itself.

Definition: A business cycle is the recurring movement of an economy between periods of stronger activity and weaker activity. It is usually discussed through expansion, peak, contraction, trough, and renewed expansion.

Boundary: A business-cycle label describes economic context. It is not a standalone market signal, investment rule, or real-time confirmation of asset direction.

The useful distinction is the object being measured. A business cycle is centered on broad economic activity such as output, employment, income, production, and sales. Asset prices, credit availability, and investor risk appetite can interact with the business cycle, but they are not the same thing.

What Is a Business Cycle?

A business cycle is the pattern of expansion and contraction in aggregate economic activity. During expansion, output, employment, income, production, and sales often improve. During contraction, those measures weaken or slow. The cycle is not a fixed calendar schedule, and each episode can vary in length, strength, and transmission path.

The concept is most useful as a classification tool. It gives structure to the economic backdrop, but it does not remove uncertainty. A phase label can describe broad conditions while still leaving major questions open about liquidity, credit, valuation, positioning, policy response, and asset-market behavior.

How the Business Cycle Moves Through Expansion and Contraction

The business cycle is often described through several positions rather than one continuous straight line. The common sequence is expansion, peak, contraction, trough, and renewed expansion. That sequence is useful, but it should not be treated as a mechanical countdown.

| Phase / position | What it describes | Interpretation limit |

|---|---|---|

| Expansion | Economic activity is generally growing, with stronger production, employment, income, sales, or demand conditions. | Asset prices can still diverge if liquidity, valuation, credit, or risk appetite weakens. |

| Peak | The economy reaches a high point before activity starts to weaken. | The turning point may only become clear after enough data is available. |

| Contraction | Economic activity slows or declines across broad measures. | Formal recession dating and asset-market behavior may differ in timing. |

| Trough | The economy reaches a low point before activity begins to recover. | Market recovery and economic recovery may not occur at the same speed. |

| Recovery / renewed expansion | Activity begins improving after a weak period and may transition into a new expansion. | Credit, liquidity, earnings, and risk appetite may improve unevenly. |

Recession belongs inside this framework, but it should not absorb the whole concept. A recession is associated with broad contraction in economic activity. A business cycle includes both the weaker side and the expansionary side of the economic sequence.

What Economic Activity the Business Cycle Tracks

Business-cycle analysis focuses on broad activity rather than one isolated indicator. Common inputs include output, employment, income, industrial production, retail or business sales, demand conditions, and other measures that show whether the economy is expanding or contracting.

No single measure captures the full cycle by itself. Employment can lag, production can react quickly in some sectors, income can be affected by policy or labor-market structure, and sales can shift differently across consumer and business segments. Stronger classification usually comes from a combination of indicators rather than one headline number.

Core idea: The business cycle is about the direction and breadth of economic activity, not one market price, one data release, or one sentiment reading.

Why Business-Cycle Labels Can Mislead Market Interpretation

A business-cycle label can be useful and still be incomplete. Markets can move before formal economic data confirms a turning point. Policy expectations, liquidity changes, credit stress, valuation, and positioning can all affect asset prices before the economic phase is obvious in the data.

This creates a common mistake: treating a macro label as if it were a market-timing tool. Expansion does not automatically mean risk assets must rise, and contraction does not automatically identify the exact moment when markets should fall or recover. The label describes a backdrop. It does not settle the investment conclusion.

Interpretation limit: A business-cycle phase should be read alongside liquidity, credit conditions, valuation, earnings expectations, policy stance, and market structure. Used alone, it can create false precision.

Business Cycle vs Market Cycle, Credit Cycle, and Stock Cycle

The business cycle is related to other cycle concepts, but it should not be merged with them. Each cycle label answers a different question. Confusing them can lead to weak analysis because economic activity, asset behavior, lending conditions, and equity participation do not always turn at the same time.

| Cycle concept | Main object | How it differs from the business cycle |

|---|---|---|

| Market cycle | Broad asset-market behavior and risk appetite | It focuses on market participation, sentiment, liquidity, and price behavior rather than only economic activity. |

| Business cycle | Economic activity | It focuses on output, employment, income, production, sales, and broad expansion or contraction. |

| Credit cycle | Lending, leverage, borrowing standards, and credit availability | It can tighten or loosen before economic activity fully reflects the change. |

| Stock cycle | Equity-market participation and price structure | It can lead, lag, or diverge from the economic cycle depending on valuation, liquidity, and expectations. |

For broader cycle routing, the Cycle Foundations section separates the main cycle labels so that each one keeps a clear analytical role.

How to Use the Business Cycle Without Turning It Into a Signal

The safest use of the business cycle is as a context layer. It can help organize whether the economic backdrop is improving, mature, weakening, or recovering. That context can then be compared with market behavior, credit conditions, liquidity, and policy response.

A practical scenario is late-cycle strength. Economic data may still look firm, but credit conditions may start tightening, market breadth may weaken, and risk appetite may become narrower. That does not automatically identify a market top, but it can show that the economic label is not enough. The broader interpretation depends on how multiple conditions interact.

Another scenario is early recovery. Economic data may still look weak because lagging indicators have not improved yet, while markets begin pricing better future conditions. Again, the business-cycle label helps frame the environment, but it does not provide a complete market conclusion by itself.

Common Mistakes When Reading the Business Cycle

| Mistake | Why it matters | Better interpretation |

|---|---|---|

| Using one indicator as the whole cycle | One data point can lag, revise, or reflect only one part of the economy. | Use a broader activity set and check whether signals are consistent. |

| Treating expansion as a market buy signal | Asset prices can respond to valuation, liquidity, and expectations before activity changes. | Separate economic context from asset-market conclusions. |

| Assuming contraction confirms immediate market weakness | Markets may have already priced part of the slowdown or may react to expected policy support. | Compare the economic phase with credit, liquidity, earnings expectations, and positioning. |

| Confusing business cycle with credit cycle | Lending conditions can tighten or loosen before broad activity data confirms the move. | Track the economic cycle and credit cycle as related but separate layers. |

FAQ

What is a business cycle?

A business cycle is the recurring movement of an economy between stronger and weaker activity. It is commonly described through expansion, peak, contraction, trough, and renewed expansion.

What are the main phases of the business cycle?

The common phases are expansion, peak, contraction, trough, and recovery or renewed expansion. The sequence is useful for classification, but the timing is not mechanical.

Is a recession part of the business cycle?

Yes. A recession is associated with the contraction side of the business cycle, but the full business cycle also includes expansion, peak, trough, and renewed expansion.

Is a business cycle the same as a market cycle?

No. A business cycle focuses on economic activity such as output, employment, income, production, and sales. A market cycle focuses more on asset prices, sentiment, risk appetite, and market participation. They can interact, but they are not the same object.

Is a business cycle the same as a credit cycle?

No. A business cycle is centered on output, employment, income, production, and broad activity. A credit cycle is centered on lending, leverage, borrowing standards, and credit availability.

Does the business cycle predict the stock market?

No. A business-cycle label can provide macro context, but it does not confirm asset direction, exact timing, market tops, market bottoms, or investment outcomes by itself.

Why are business-cycle turning points difficult to identify?

Turning points are difficult because economic data can lag, get revised, and move unevenly across sectors. A peak or trough often becomes clearer only after enough evidence accumulates.