A business cycle describes broad economic activity, such as expansion, slowdown, contraction, and recovery. A market cycle describes financial-market behavior, including asset prices, risk appetite, valuation, breadth, liquidity, and leadership. They can influence each other, but they classify different objects and neither label is a timing signal by itself.

The useful split is the object being classified. Business-cycle language belongs to the economy. Market-cycle language belongs to financial markets. Confusion starts when a weak market, a strong economy, changing expectations, or narrowing leadership makes both ideas appear in the same discussion.

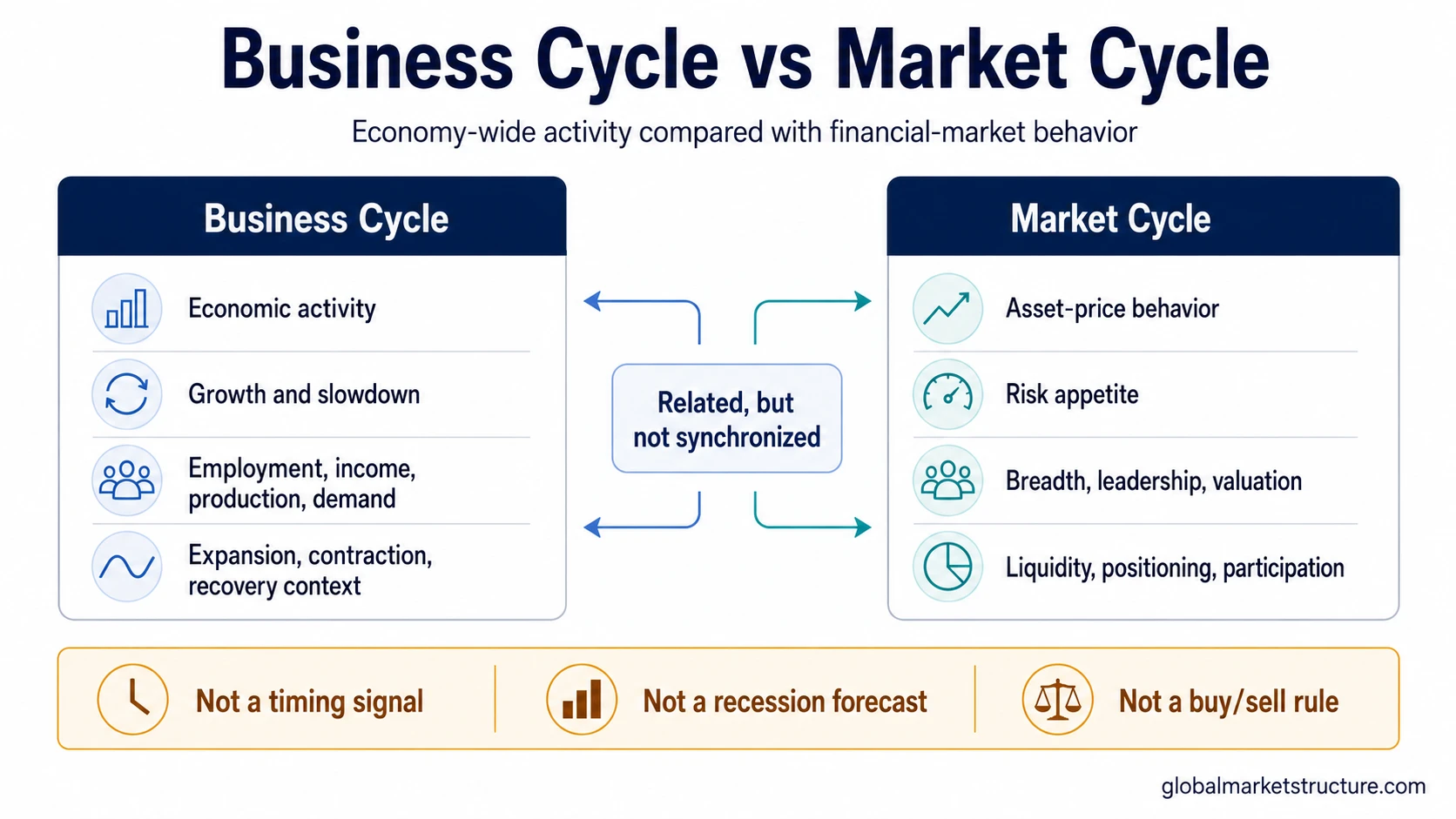

Business cycle vs market cycle: the core difference

A business cycle is about the condition of economy-wide activity. It asks whether production, income, employment, demand, and broad growth conditions are expanding, slowing, contracting, or recovering.

A market cycle is about the condition of financial-market behavior. It asks whether asset prices, risk appetite, valuation, liquidity, breadth, leadership, and positioning are improving, weakening, diverging, or resetting.

The two can overlap because markets respond to expectations about the economy. They are still different readings. The business-cycle reading is a macro activity question. The market-cycle reading is a market behavior question.

How to decide which label applies

The cleanest test is to ask what is being classified. If the evidence is about broad activity in the economy, business-cycle language is usually the better fit. If the evidence is about prices, leadership, liquidity, or risk appetite in financial markets, market-cycle language is usually the better fit.

| Criterion | Business cycle | Market cycle |

|---|---|---|

| Main question answered | What is happening to broad economic activity? | What is happening to financial-market behavior? |

| Object being classified | The economy. | Financial markets and asset prices. |

| Evidence used | Growth, income, employment, production, demand, contraction, recovery, and recession context. | Prices, breadth, leadership, valuation, liquidity, risk appetite, positioning, and market participation. |

| Typical observables | Economic activity data, labor conditions, production trends, income conditions, and demand signals. | Index behavior, sector or style leadership, market breadth, valuation pressure, volatility, liquidity, and risk appetite. |

| Timing relationship | Often identified through economic activity and macro data. | Can sometimes move before, during, or after macro data because markets price expectations. |

| Common misuse | Treating a macro phase as an automatic asset-allocation rule. | Treating market weakness or strength as proof of recession, recovery, or expansion. |

| Go deeper into | Business-cycle concept | Market-cycle concept |

Same scenario, different reading

A common scenario is that growth expectations weaken while equity leadership narrows and risk appetite fades. Both cycle labels may appear in the discussion, but they answer different questions.

Business-cycle reading: the question is whether broad economic activity is slowing, contracting, or moving toward recovery. The focus is the economy: demand, production, income, employment, and the durability of expansion or contraction.

Market-cycle reading: the question is whether financial markets are already repricing expectations. The focus is market behavior: asset prices, breadth, leadership, valuation, liquidity, positioning, and risk appetite.

The same environment can create both readings. The difference is not which label sounds more bearish or bullish. The difference is whether the evidence is classifying the economy or the market.

How business cycles and market cycles interact

Business cycles and market cycles interact because markets discount expectations about growth, policy, earnings, liquidity, and risk. When investors expect economic conditions to weaken, market behavior can change before broad macro data looks clearly weak.

That does not mean the market cycle always leads the business cycle. Market prices and macro data can move on different clocks. Prices may adjust as expectations change, while many economic indicators describe activity that is measured and reported after the fact. Markets can also overshoot, diverge, or reverse as liquidity, positioning, valuation, or policy expectations change.

The relationship is clearest when both readings point the same way, such as weakening macro activity alongside deteriorating market breadth. It is less clear when one reading is healthy and the other is deteriorating. That disagreement is a reason to keep the labels separate, not to force one cycle to explain everything.

Common mistakes when comparing the two

Mistake 1: treating a bull market as economic expansion. Rising asset prices can occur during improving expectations, easier liquidity, valuation expansion, or narrow leadership. That does not automatically classify the whole economy as expanding.

Mistake 2: treating a bear market as recession. Market weakness can reflect falling risk appetite, tighter liquidity, valuation pressure, or positioning stress. It does not by itself prove a business-cycle contraction.

Mistake 3: using a business-cycle label as a market-timing rule. A macro phase can provide context, but it does not create a direct buy/sell decision by itself.

Mistake 4: using a market-cycle label as a recession forecast. Market-cycle deterioration can reflect changing expectations, but it does not prove that the economy has entered recession or that recovery has started.

Mistake 5: assuming the two cycles map one-to-one. Economic expansion can coexist with a weakening market cycle, and market repair can begin before economic data fully recovers. The labels are related, not interchangeable.

What the distinction cannot do

Business-cycle and market-cycle labels classify context. They do not produce deterministic forecasts, portfolio instructions, recession calls, or market timing signals.

A safer interpretation keeps the two readings separate. The business cycle helps classify economy-wide activity. The market cycle helps classify financial-market behavior. When the two readings disagree, the disagreement is information, not a reason to force one label to explain everything.

Where each concept belongs

Use the business cycle concept when the question is about economy-wide expansion, slowdown, contraction, recovery, recession context, or broad macro activity.

Use the market cycle concept when the question is about asset-price behavior, risk appetite, market phases, breadth, leadership, valuation, liquidity, and how financial markets move through changing conditions.

Credit conditions can affect both readings, but they are a separate cycle lens. If borrowing conditions, lending standards, spreads, leverage, and default pressure are the main subject, the credit cycle becomes the more precise concept.

FAQ

Is a market cycle the same as a business cycle?

No. A business cycle classifies broad economic activity, while a market cycle classifies financial-market and asset-price behavior. They can influence each other, but they are not the same concept.

Can markets weaken while the economy is still expanding?

Yes. Markets can weaken because risk appetite, liquidity, valuation, breadth, or leadership deteriorates even while broad economic activity is still expanding. That is one reason market-cycle and business-cycle labels should stay separate.

Does the market cycle lead the business cycle?

Market behavior can sometimes move ahead of economic data because markets price expectations, but the relationship is not fixed. It should not be treated as a reliable timing rule.

Can either cycle be used as a buy or sell signal?

No. Business-cycle and market-cycle labels can help classify context, but they do not create buy/sell signals by themselves.