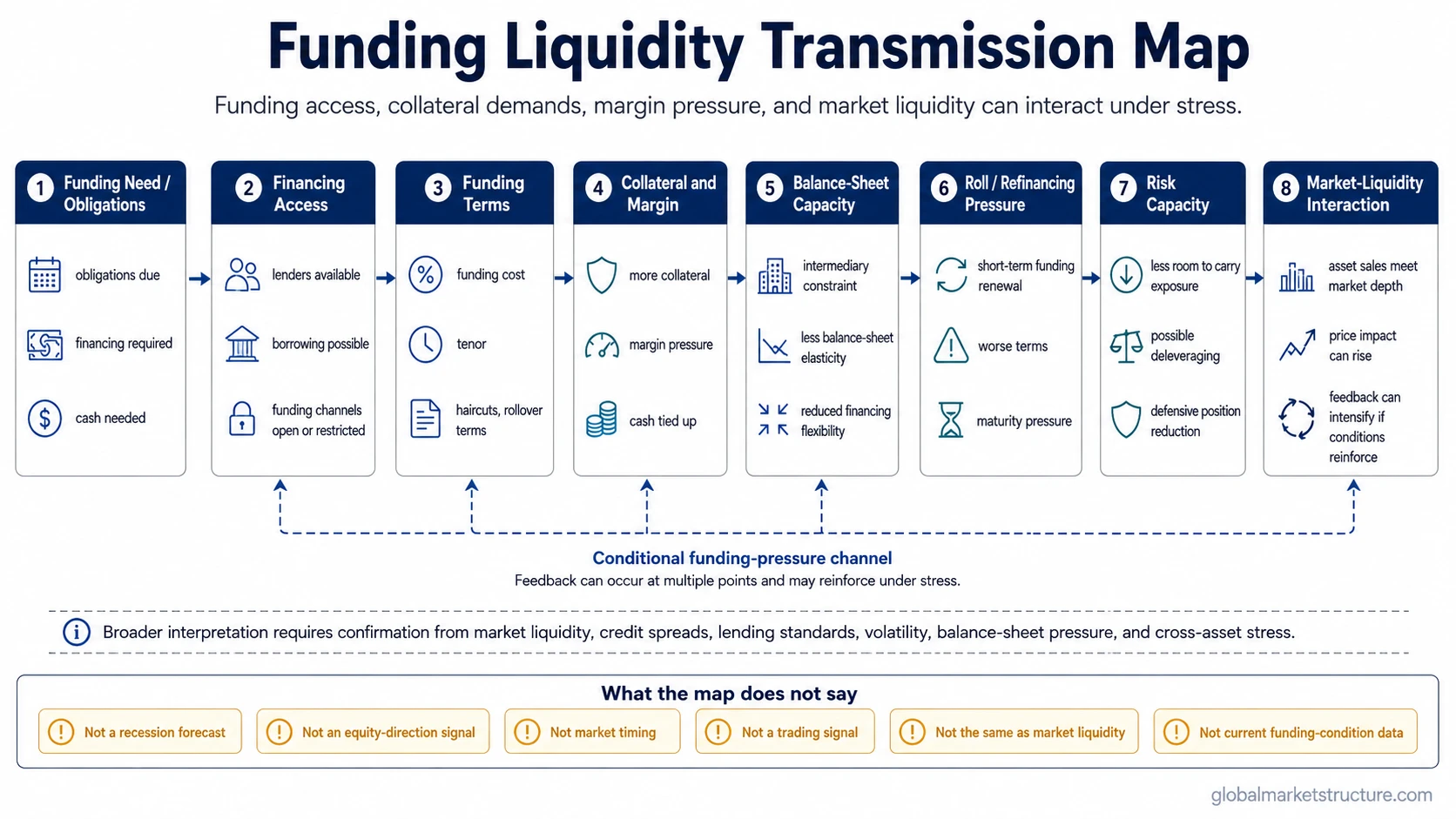

Funding liquidity is the ability of a market participant, institution, or financial system to obtain funding or meet funding obligations when needed. It is about financing access, not how easily an asset can be traded. When funding becomes expensive, short-term, or collateral-intensive, risk capacity can weaken and pressure can interact with market liquidity.

Funding liquidity is not a recession forecast, equity-direction signal, market-timing tool, or trading signal. It is a conditional funding-pressure channel that becomes more important when financing terms, collateral demands, margin pressure, balance-sheet capacity, and market liquidity begin to deteriorate together.

What Is Funding Liquidity?

Funding liquidity means the ability to obtain cash or financing when obligations must be met. For financial institutions, leveraged investors, dealers, or other market participants, that can involve borrowing, rolling short-term funding, posting collateral, meeting margin calls, or financing existing positions.

The concept belongs to liquidity and monetary conditions because it describes the financing side of market activity. A participant may own assets that appear liquid, but still face stress if lenders reduce funding, raise haircuts, shorten terms, demand more collateral, or charge higher funding costs.

Funding liquidity is strongest when financing is available on workable terms. It weakens when funding becomes scarce, costly, uncertain, or dependent on more restrictive collateral conditions.

Funding Liquidity in One View

- Core meaning: access to funding or ability to meet funding obligations.

- Main focus: financing terms, collateral, margin, funding cost, and balance-sheet capacity.

- Main distinction: funding liquidity is about financing access, while market liquidity is about trading assets without large price impact.

- Main risk: tighter funding can reduce risk capacity and may force position reduction under stress.

- Main limitation: funding liquidity does not provide timing, direction, or a standalone forecast.

Funding Liquidity vs Funding Liquidity Risk vs Market Liquidity

The most important distinction is between current funding access, future funding uncertainty, and asset-market tradability. These concepts can interact, but they are not interchangeable.

| Concept | What it means | What it focuses on | Common mistake |

|---|---|---|---|

| Funding liquidity | The ability to obtain funding or meet funding obligations when needed. | Financing access, borrowing terms, collateral, margin, and cash availability. | Treating it as the same thing as money supply or central-bank liquidity. |

| Funding liquidity risk | The risk that future funding becomes unavailable, too expensive, or insufficient. | Rollover risk, refinancing pressure, funding uncertainty, and stress planning. | Treating future funding risk as identical to current funding liquidity. |

| Market liquidity | The ability to buy or sell assets without causing a large price impact. | Bid-ask spreads, depth, transaction size, and price impact. | Assuming a tradable asset eliminates financing stress. |

Funding liquidity can be stable while market liquidity is weak, and market liquidity can appear acceptable while funding pressure is building. Stress becomes more structural when both sides weaken at the same time: financing becomes harder and asset sales become harder to absorb.

How Funding Liquidity Works

Funding liquidity works through the terms that determine whether participants can keep financing assets, meet obligations, and maintain risk exposure. The mechanism is not limited to one market or one institution type. It is a funding channel that can affect risk capacity when conditions tighten.

| Channel | What changes | Why it matters | What not to infer |

|---|---|---|---|

| Funding access | Financing becomes easier or harder to obtain. | Participants may have less room to carry positions or meet obligations. | Do not infer immediate market direction from funding access alone. |

| Funding cost | Borrowing becomes cheaper or more expensive. | Higher cost can reduce the appeal of leveraged exposure or maturity rollover. | Do not treat higher cost as a guaranteed forced-selling trigger. |

| Collateral and margin | Lenders may require more collateral, higher haircuts, or additional margin. | More capital becomes tied up, reducing flexibility and risk capacity. | Do not assume every collateral demand becomes systemic stress. |

| Balance-sheet capacity | Intermediaries may reduce willingness or ability to provide financing. | Funding channels can become less elastic when balance sheets are constrained. | Do not reduce the whole concept to bank balance sheets only. |

| Roll or refinancing pressure | Short-term funding may need to be renewed on worse terms. | Rollover stress can pressure positions even if the underlying asset has not changed. | Do not confuse rollover pressure with a recession forecast. |

| Market-liquidity interaction | Forced or defensive selling may meet thinner trading conditions. | Funding pressure can become more damaging when asset markets cannot absorb sales smoothly. | Do not assume every funding shock creates a liquidity spiral. |

The sequence often matters more than any single input: funding access tightens, funding terms worsen, collateral or margin demands rise, balance-sheet flexibility declines, rollover pressure increases, and risk capacity weakens. Market stress becomes more plausible when that sequence meets poor market liquidity, wider credit spreads, or broader cross-asset pressure.

Why Funding Liquidity Matters for Market Conditions

Funding liquidity matters because many financial positions depend on the ability to finance, roll, or collateralize exposure. When financing remains available, participants have more flexibility to absorb volatility, hold positions, and wait for normal market functioning. When financing becomes constrained, the same market move can become more stressful.

The key market-structure point is risk capacity. Tight funding conditions can force participants to choose between posting more collateral, reducing leverage, selling assets, or declining new risk. That does not make funding liquidity a directional signal, but it can change how fragile the market environment becomes.

Funding liquidity can also shape how shocks travel. A price decline may create collateral pressure. Collateral pressure may require additional cash. Additional cash needs may force asset sales. Asset sales may become more disruptive if trading depth is weak. The pressure path depends on funding terms, leverage, collateral quality, market liquidity, and the willingness of intermediaries to provide balance-sheet capacity.

Practical Funding-Pressure Scenario

A leveraged participant can hold assets comfortably while financing is available on stable terms. Pressure builds if lenders raise funding costs, demand more collateral, shorten funding terms, or reduce the amount they are willing to finance.

At first, the issue may not appear in asset prices. The participant may still meet obligations, and the market may still trade normally. Stress becomes more visible if the participant must sell assets to raise cash, reduce leverage, or satisfy margin requirements. If many participants face similar pressure while trading depth is thin, funding liquidity can begin interacting with market liquidity.

This is an illustrative scenario, not a historical case. The useful lesson is conditional: funding pressure matters most when financing constraints, collateral pressure, reduced risk capacity, and weaker trading conditions reinforce one another.

Common Misreadings of Funding Liquidity

Funding liquidity is often misread because the word liquidity is used across several different market concepts. The same term can refer to financing access, asset tradability, central-bank operations, cash balances, or broad risk appetite. A clean reading separates those layers before drawing conclusions.

Funding liquidity is not market liquidity. A participant can face financing pressure even if the asset still trades. The opposite can also happen: trading can become difficult even when funding access has not collapsed.

Funding liquidity is not a recession forecast. Funding stress can appear during broader macro weakness, but the concept does not predict recession by itself.

Funding liquidity is not an equity-direction signal. Tighter financing conditions can weaken risk capacity, but asset prices still depend on earnings expectations, rates, credit conditions, positioning, policy context, and market liquidity.

Funding liquidity is not one metric. No single indicator fully captures funding access, funding cost, collateral pressure, margin dynamics, rollover risk, and balance-sheet capacity.

What Can Confirm Funding Liquidity Stress?

A funding-pressure interpretation becomes stronger when multiple signals point in the same direction. One isolated sign can be noisy. A broader pattern across financing terms, credit, market liquidity, volatility, and cross-asset stress is more informative.

| Confirmation area | What to look for | Why it matters |

|---|---|---|

| Funding terms | Higher funding costs, shorter terms, tighter access, or reduced lending appetite. | Directly affects the ability to finance exposure and meet obligations. |

| Collateral and margin | More demanding collateral requirements or rising margin pressure. | Can tie up cash and reduce flexibility. |

| Credit conditions | Wider spreads, tighter lending standards, or weaker credit availability. | Shows whether funding stress is isolated or part of broader risk repricing. |

| Market liquidity | Wider bid-ask spreads, thinner depth, or larger price impact. | Funding-driven sales become more disruptive when markets absorb less flow. |

| Cross-asset stress | Pressure across rates, credit, currencies, volatility, or risk assets. | Helps separate broad funding stress from a narrow market-specific issue. |

The strongest interpretation usually comes from alignment. Funding pressure, weaker market liquidity, wider credit risk compensation, and rising volatility create a more serious environment than any single signal alone.

Related Liquidity Concepts

Funding liquidity is one part of the liquidity system. Nearby concepts clarify different parts of the same environment.

- Market liquidity vs funding liquidity separates financing access from asset-market tradability.

- Liquidity crisis describes a more severe breakdown where liquidity pressure spreads and normal market functioning becomes impaired.

- Liquidity risk covers the broader risk that liquidity may not be available when it is needed.

Funding Liquidity FAQ

What is funding liquidity in simple terms?

Funding liquidity is the ability to get cash or financing when obligations must be met. It focuses on funding access, borrowing terms, collateral, margin, and the ability to roll or maintain financing.

Is funding liquidity the same as market liquidity?

No. Funding liquidity is about financing access. Market liquidity is about buying or selling assets without causing a large price impact. The two can interact, especially during stress, but they are separate concepts.

What is funding liquidity risk?

Funding liquidity risk is the risk that future funding becomes unavailable, too expensive, or insufficient. Funding liquidity describes current funding ability, while funding liquidity risk focuses on possible future funding problems.

Can funding liquidity stress lead to forced selling?

It can under certain conditions. If funding costs rise, collateral requirements increase, or margin pressure builds, leveraged participants may need to reduce exposure or sell assets. The effect is stronger when market liquidity is also weak.

Does tight funding liquidity predict stock market direction?

No. Tight funding liquidity can reduce risk capacity, but it does not predict equity direction by itself. Market interpretation requires confirmation from credit conditions, market liquidity, volatility, positioning, rates, and broader cross-asset behavior.