A liquidity spiral is a self-reinforcing deterioration in liquidity conditions where falling prices, funding pressure, margin or collateral stress, forced selling, and weaker market depth can feed into each other.

The feedback loop is the defining feature. A price decline can create cash or collateral pressure. Selling used to meet that pressure can hit thinner market depth, create larger price impact, and add new losses or collateral strain.

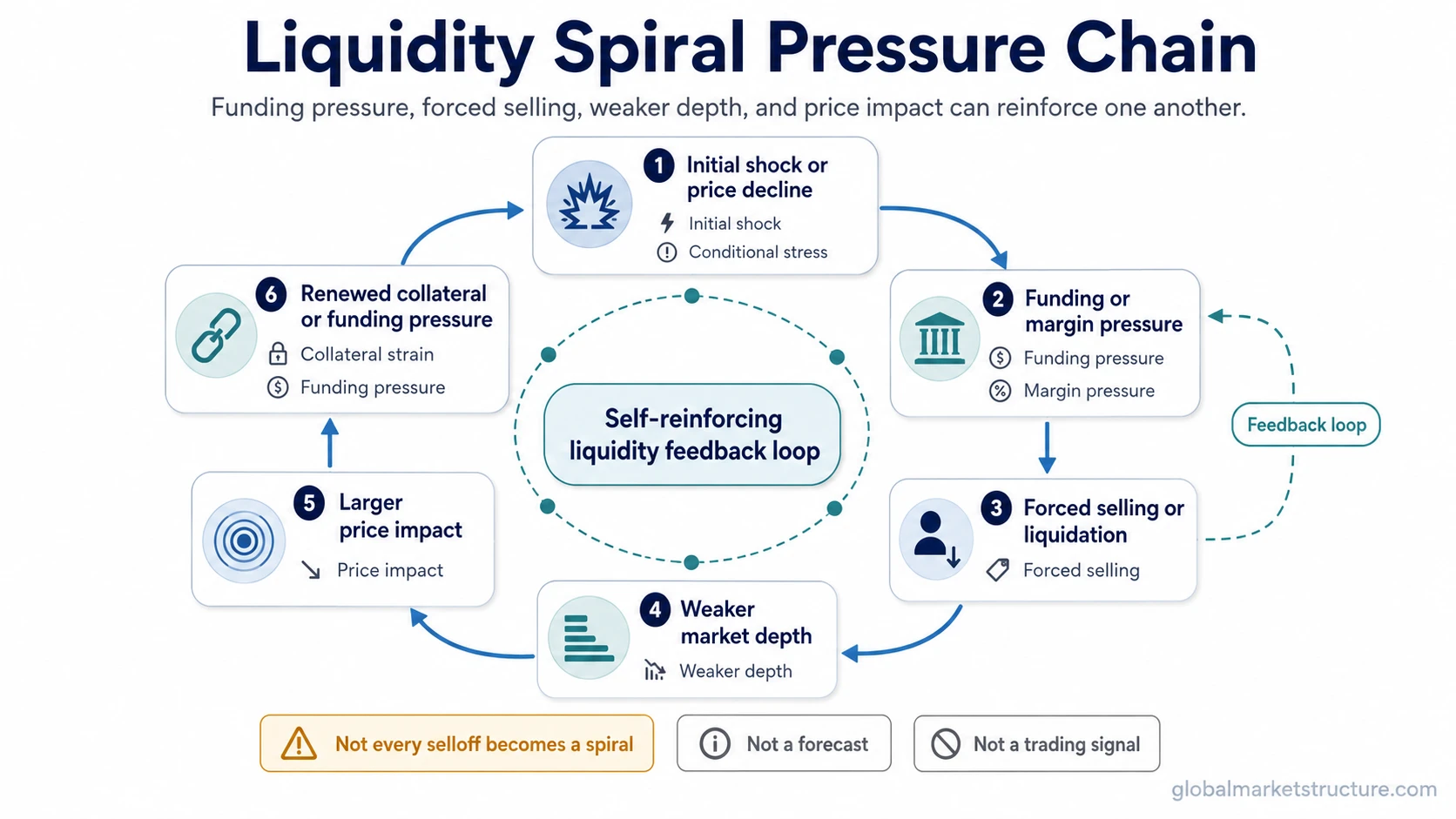

Liquidity spiral definition: a liquidity spiral is a feedback mechanism in which worsening funding conditions and weaker market liquidity reinforce each other, often through forced selling, margin pressure, collateral demands, and rising price impact.

- A liquidity spiral is a mechanism, not just a decline in asset prices.

- Funding pressure and market liquidity can reinforce each other.

- Forced selling can weaken depth and increase price impact, but it is conditional rather than automatic.

- A liquidity spiral is not a recession forecast, insolvency proof, or trading signal.

How a Liquidity Spiral Works

A liquidity spiral usually begins when an initial shock reduces asset prices, available funding, confidence, or balance-sheet capacity. The shock does not need to be large by itself. The spiral risk appears when the response to that shock creates additional strain.

| Stage | What happens | Why it can reinforce the loop |

|---|---|---|

| Initial shock | Prices fall, volatility rises, or funding terms become less favorable. | The first move can reduce confidence, collateral value, or available risk capacity. |

| Funding or margin pressure | Participants may need cash, financing, or additional collateral. | Strain increases when obligations cannot be met easily without selling assets. |

| Forced selling | Assets are sold to raise cash, reduce leverage, or meet collateral calls. | Selling becomes less voluntary and more mechanical. |

| Weaker market depth | Buyers become more cautious and available depth may shrink. | The same amount of selling can move prices more than usual. |

| Larger price impact | Transactions create sharper price moves because liquidity is thinner. | New losses can create new funding, margin, or collateral pressure. |

| Reinforcing loop | Pressure feeds back into more selling and weaker liquidity. | The process can continue until funding pressure eases, depth returns, or forced selling slows. |

The reading becomes stronger when the funding channel and the market-depth channel appear together. If prices fall without forced selling, collateral pressure, or thinner depth, the liquidity spiral label is usually too strong.

Market Liquidity and Funding Liquidity in the Loop

Market liquidity describes the ability to trade without creating large price impact. When market liquidity is strong, buyers and sellers can usually transact with narrower spreads, deeper order books, and less disruption. When market liquidity weakens, trades can move prices more sharply.

Funding liquidity describes the ability of participants to obtain financing, roll funding, meet obligations, or post collateral. When funding liquidity weakens, participants may have less room to hold positions through volatility.

A liquidity spiral connects these two forms of liquidity. Falling prices can reduce collateral values and create funding strain. Funding strain can force asset sales. Forced sales can weaken market liquidity and push prices lower. Lower prices can then create additional collateral or financing strain.

Core interaction: weaker market liquidity increases price impact, while weaker funding liquidity reduces the ability to absorb that price impact. The spiral becomes more dangerous when both forms of liquidity deteriorate at the same time.

Liquidity Spiral vs Liquidity Crisis

A liquidity spiral and a liquidity crisis are related, but they are not the same concept. A spiral describes a feedback mechanism. A crisis describes a broader stress condition in which liquidity becomes insufficient relative to demand for cash, funding, or tradable depth.

| Concept | Main meaning | Common misread |

|---|---|---|

| Liquidity spiral | A self-reinforcing loop between falling prices, funding pressure, forced selling, and weaker market liquidity. | Reading every price decline as a spiral. |

| Liquidity crisis | A broader condition where liquidity demand exceeds available cash, funding access, or market depth. | Treating the crisis label as automatic evidence of insolvency or market direction. |

| Liquidity pressure | A strain on cash, financing, collateral, or trading depth. | Assuming pressure must become a full spiral. |

| Solvency problem | A condition where assets or income may be insufficient relative to obligations. | Confusing temporary liquidity stress with confirmed insolvency. |

A liquidity spiral can contribute to a liquidity crisis, but the spiral is the mechanism inside the pressure chain. The crisis is the broader state of stress that may result when the mechanism becomes severe or widespread.

What a Liquidity Spiral Does Not Mean

Common mistake: treating a liquidity spiral as a synonym for falling prices. Falling prices can be part of the process, but the spiral requires a reinforcing liquidity channel.

A normal selloff can happen because investors change expectations, risk appetite weakens, or valuations adjust. That is not enough to define a liquidity spiral. The spiral reading becomes more relevant when falling prices create strain that forces additional selling into weaker market depth.

- Not every selloff is a liquidity spiral. A decline can occur without forced deleveraging or funding stress.

- Not every spiral proves insolvency. Liquidity pressure and solvency problems can interact, but they are not identical.

- Not a recession forecast. A liquidity spiral is a stress mechanism, not a complete macro forecast.

- Not a trading signal. It does not provide an entry, exit, target, or market-timing rule.

- Not only central-bank money supply. The mechanism can involve financing access, collateral, leverage, market depth, and participant behavior.

The safest interpretation is conditional. A liquidity spiral may be present when funding strain, forced selling, and market-depth deterioration reinforce each other. Without that feedback loop, the term is usually too strong.

A Practical Liquidity Spiral Scenario

A leveraged participant holds assets that decline in price. The price decline reduces collateral value, so the participant faces higher margin or collateral demands. To raise cash, the participant sells part of the position. Market depth is weaker than normal, so the sale creates larger price impact. The lower price then increases strain on other participants with similar exposures.

This scenario is illustrative, not a historical claim. Price decline alone is not the full mechanism. Funding strain alone is not the full mechanism. The spiral appears when liquidity demand and market-depth weakness reinforce each other.

Why the Feedback Loop Matters

Liquidity can look adequate before stress becomes visible. A market may appear liquid when conditions are calm, but the same market can behave differently when many participants need to sell, raise cash, or reduce risk at the same time.

Depth can disappear when buyers step back, dealers reduce balance-sheet commitment, financing becomes more expensive, or participants become less willing to absorb inventory. Under those conditions, selling pressure can have a larger price impact than expected.

Limitation: a liquidity spiral describes how pressure can propagate. It does not identify the exact starting point, predict the final outcome, or prove that authorities, lenders, or counterparties will respond in a specific way.

Related Liquidity Concepts

A liquidity spiral sits inside the broader liquidity framework. The wider concept of liquidity covers the availability of cash, funding, and tradable market depth. Liquidity risk focuses on the possibility that liquidity may not be available when needed.

- Market liquidity: useful for understanding trading depth, spreads, and price impact.

- Funding liquidity: useful for understanding financing access, margin pressure, and collateral needs.

- Liquidity crisis: useful for understanding the broader stress condition that can emerge when liquidity demand overwhelms available supply.

- Liquidity risk: useful for understanding the risk that liquidity may disappear or become expensive under stress.

Liquidity Spiral FAQ

Is a liquidity spiral the same as a liquidity crisis?

No. A liquidity spiral is a feedback mechanism. A liquidity crisis is a broader stress condition in which liquidity becomes insufficient relative to demand for cash, funding, or market depth.

Does every selloff become a liquidity spiral?

No. A selloff becomes more consistent with a liquidity spiral only when price declines, funding pressure, forced selling, and weaker market depth reinforce each other.

Is a liquidity spiral a trading signal?

No. A liquidity spiral is a market-stress mechanism. It does not provide a buy signal, sell signal, entry level, exit level, target, or timing rule.