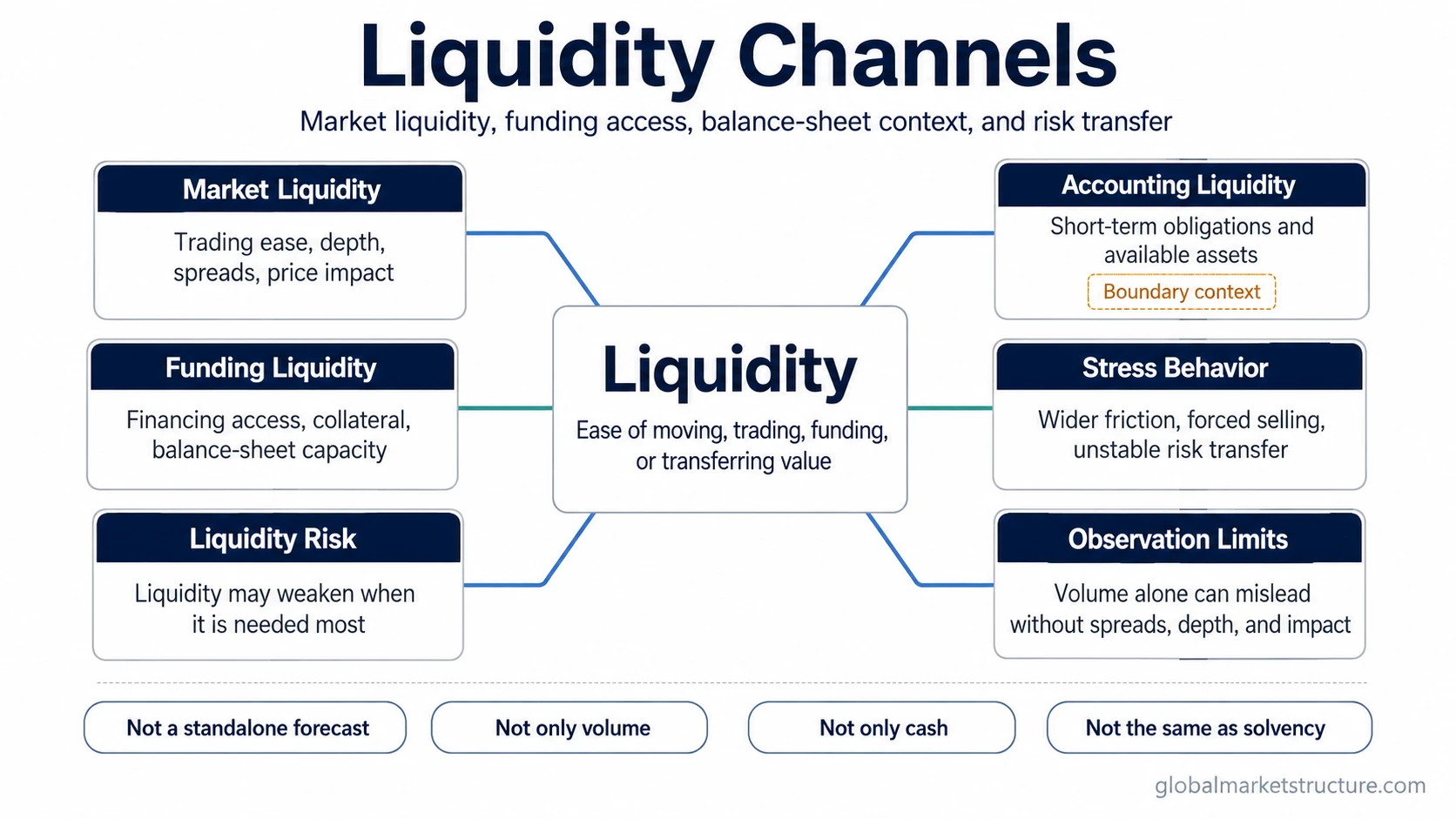

Liquidity describes how easily value can move through markets, funding channels, and risk transfer without excessive friction, cost, delay, or price impact. In market-structure analysis, liquidity is not one single condition. It can refer to how easily an asset trades, how easily participants obtain funding, how quickly balance-sheet pressure spreads, or how costly it becomes to transfer risk when conditions tighten.

Liquidity means: the ability to convert, transfer, trade, or fund value with limited friction. Strong liquidity usually means transactions can happen with lower cost and less disruption. Weak liquidity means transactions, financing, or risk transfer become harder, slower, more expensive, or more price-disruptive.

The key distinction is that market liquidity and funding liquidity are related but not identical. Market liquidity concerns the ability to trade an asset without large price impact. Funding liquidity concerns the ability to obtain financing, roll obligations, post collateral, or maintain balance-sheet capacity.

Key Points

- Liquidity is a broad condition, not a single market signal.

- Market liquidity is about trading ease, transaction cost, depth, and price impact.

- Funding liquidity is about access to financing, collateral, and balance-sheet capacity.

- Accounting liquidity belongs mostly as boundary context because balance-sheet ratios do not explain market functioning by themselves.

- Liquidity risk appears when liquidity weakens or disappears when participants need it most.

- High volume does not automatically mean strong liquidity if spreads widen, depth disappears, or transactions begin to move prices sharply.

What Liquidity Means in Market Structure

Liquidity connects the ease of action with the cost of action. A liquid asset can usually be bought, sold, financed, or risk-managed without forcing a large adjustment in price or funding terms. An illiquid condition appears when that same action requires wider concessions, slower execution, larger discounts, higher collateral pressure, or more uncertainty about whether counterparties will remain available.

In market-structure analysis, liquidity matters because prices are not shaped only by valuation, earnings, inflation, or policy expectations. They are also shaped by whether participants can transact, finance positions, absorb flows, and transfer risk. A market can have an attractive narrative and still behave poorly if liquidity channels become fragile.

Liquidity should not be treated as a direct forecast. Easier liquidity can support risk-taking under some conditions, while tighter liquidity can increase fragility. The interpretation depends on the channel involved, the market being observed, the balance-sheet backdrop, and whether stress is isolated or spreading.

Main Liquidity Channels

Liquidity separates into several channels because different problems can look similar on the surface. A market may trade actively but become harder to transact in size. A borrower may own valuable assets but struggle to obtain funding. A company may hold liquid current assets, while a security issued by that company trades with poor market depth. These are different liquidity questions.

| Liquidity type | Question it answers | Common signals | Primary use |

|---|---|---|---|

| Broad liquidity | How easily value can move through markets or funding channels | Transaction friction, financing conditions, risk-transfer capacity | Broad market-functioning context |

| Market liquidity | Can an asset trade without large price impact? | Bid-ask spreads, market depth, transaction costs, price impact | Market liquidity |

| Funding liquidity | Can participants obtain or roll financing? | Collateral terms, margin pressure, balance-sheet capacity, financing access | Funding liquidity |

| Accounting liquidity | Can an entity meet near-term obligations with available assets? | Cash, current assets, current liabilities, short-term obligations | Balance-sheet context, not a direct measure of market functioning |

| Liquidity risk | What happens if liquidity is not available when needed? | Wider spreads, forced selling, funding pressure, unstable risk transfer | Liquidity risk |

Market Liquidity vs Funding Liquidity

The most important distinction is between trading liquidity and financing liquidity. The two channels often interact, but they answer different questions.

Market liquidity: the ability to transact in an asset without large price impact. It is usually associated with tighter bid-ask spreads, deeper order books, lower transaction costs, and more reliable execution in size.

Funding liquidity: the ability to obtain financing, roll debt, meet margin calls, or use collateral without severe balance-sheet pressure. It is tied to credit access, collateral quality, dealer balance sheets, funding markets, and the willingness of lenders or counterparties to provide capacity.

The difference matters because a market can look tradable until funding pressure forces participants to sell. It can also look risky at the asset level while funding conditions remain stable. The relationship becomes more important when leverage, collateral, and forced deleveraging enter the picture. For a direct distinction, the deeper comparison is market liquidity vs funding liquidity.

Accounting Liquidity Is Only a Boundary Context

Accounting liquidity refers to whether an entity can meet near-term obligations with cash or assets that can be converted into cash. It is useful in corporate finance and balance-sheet analysis, but it should not be confused with market liquidity or funding liquidity.

A company may have a liquid balance sheet while one of its securities trades poorly. A bond may be issued by a solvent borrower but still be hard to trade in stressed markets. A bank or dealer may hold assets that are theoretically valuable but difficult to convert quickly without a discount. These distinctions prevent liquidity from being reduced to cash balances or accounting ratios.

How Liquidity Can Be Observed

Liquidity is not directly visible through one number. It is usually inferred from a set of conditions that describe whether transactions and financing can happen without unusual friction.

| Observation | What it may suggest | Main limitation |

|---|---|---|

| Bid-ask spreads | Wider spreads can indicate higher transaction cost or lower dealer confidence | Spreads can vary by asset class, market hours, and event risk |

| Market depth | Thin depth can mean larger trades move price more easily | Displayed depth may not capture hidden liquidity or fast order cancellation |

| Price impact | Large price response to normal flow can signal weaker tradability | Price impact can also reflect new information, not only liquidity stress |

| Transaction volume | Heavy activity can indicate participation | Volume alone does not prove strong liquidity |

| Funding access | Easy financing can support balance-sheet flexibility | Funding access can tighten quickly if collateral values or counterparty confidence change |

Market-liquidity measurement is a separate topic because spreads, depth, transaction costs, price impact, turnover, and execution quality can point in different directions. The measurement process belongs in how to measure market liquidity.

Why Volume Alone Can Mislead

High volume can make a market look liquid, but activity is not the same as easy execution. During stress, volume may rise because participants are forced to transact, not because liquidity is strong. If bid-ask spreads widen, depth falls, and trades move prices sharply, high activity can coexist with poor liquidity.

Illustrative scenario: a market trades far more contracts than usual after a major repricing. At first glance, the high volume appears to signal strong liquidity. The read becomes weaker if spreads widen, resting depth disappears, and moderate orders begin moving price more than normal. Under those conditions, the market is active, but actual liquidity may be deteriorating.

The stronger interpretation compares volume with spreads, depth, transaction cost, price impact, volatility, and funding conditions. Liquidity analysis becomes more useful when activity is separated from the cost and stability of that activity.

When Liquidity Becomes a Risk

Liquidity becomes a risk when participants assume they can transact, finance, or transfer exposure, but those channels weaken when they are needed. This can happen through wider spreads, thinner depth, higher funding costs, margin pressure, reduced dealer balance-sheet capacity, or a loss of counterparty confidence.

The risk is not only that prices move. The deeper issue is that participants may lose flexibility. They may have to accept worse execution, sell assets into weak markets, reduce exposure, post more collateral, or withdraw from risk-taking. In that environment, liquidity affects both market functioning and the ability of participants to respond.

If the pressure spreads across assets or funding channels, the condition can develop into a liquidity crisis. If selling pressure weakens liquidity, and weaker liquidity creates more selling pressure, the feedback loop becomes a liquidity spiral.

What Liquidity Does Not Prove

Liquidity should not be treated as a standalone forecast. It can influence market conditions, but it does not automatically predict direction, returns, timing, or asset performance.

- Liquidity is not a buy or sell signal.

- High volume does not always mean strong liquidity.

- Cash or current assets do not equal market liquidity.

- Liquidity and solvency are related in stress, but they are not the same concept.

- Market liquidity and funding liquidity can interact, but they should not be used interchangeably.

- Current liquidity stress should not be claimed without dated evidence and appropriate data.

How Liquidity Affects Markets

Liquidity affects markets through the conditions under which participants trade, finance, and transfer risk. When liquidity is abundant, participants may find it easier to transact and maintain exposure. When liquidity weakens, the same exposure can become harder to trade, fund, or hedge without larger costs.

The effect depends on what is changing. Wider spreads affect trading cost. Thinner depth affects price impact. Funding constraints affect balance-sheet flexibility. Collateral pressure can force position reduction. Risk-transfer limits can make hedging more expensive or less reliable.

A broader treatment of transmission, market impact, and related conditions belongs in how liquidity affects markets.

Related Liquidity Concepts

Liquidity becomes clearer when each related concept keeps its own job.

| Concept | Use it for |

|---|---|

| Market liquidity | Trading conditions, spreads, depth, transaction cost, and price impact |

| Funding liquidity | Financing access, collateral, margin pressure, and balance-sheet capacity |

| Liquidity risk | The risk that liquidity weakens or disappears when needed |

| Liquidity crisis | Stress conditions where liquidity problems become broad or severe |

| Liquidity spiral | Feedback loops between selling pressure, price impact, and funding strain |

| Market liquidity vs funding liquidity | The difference between trading ease and financing access |