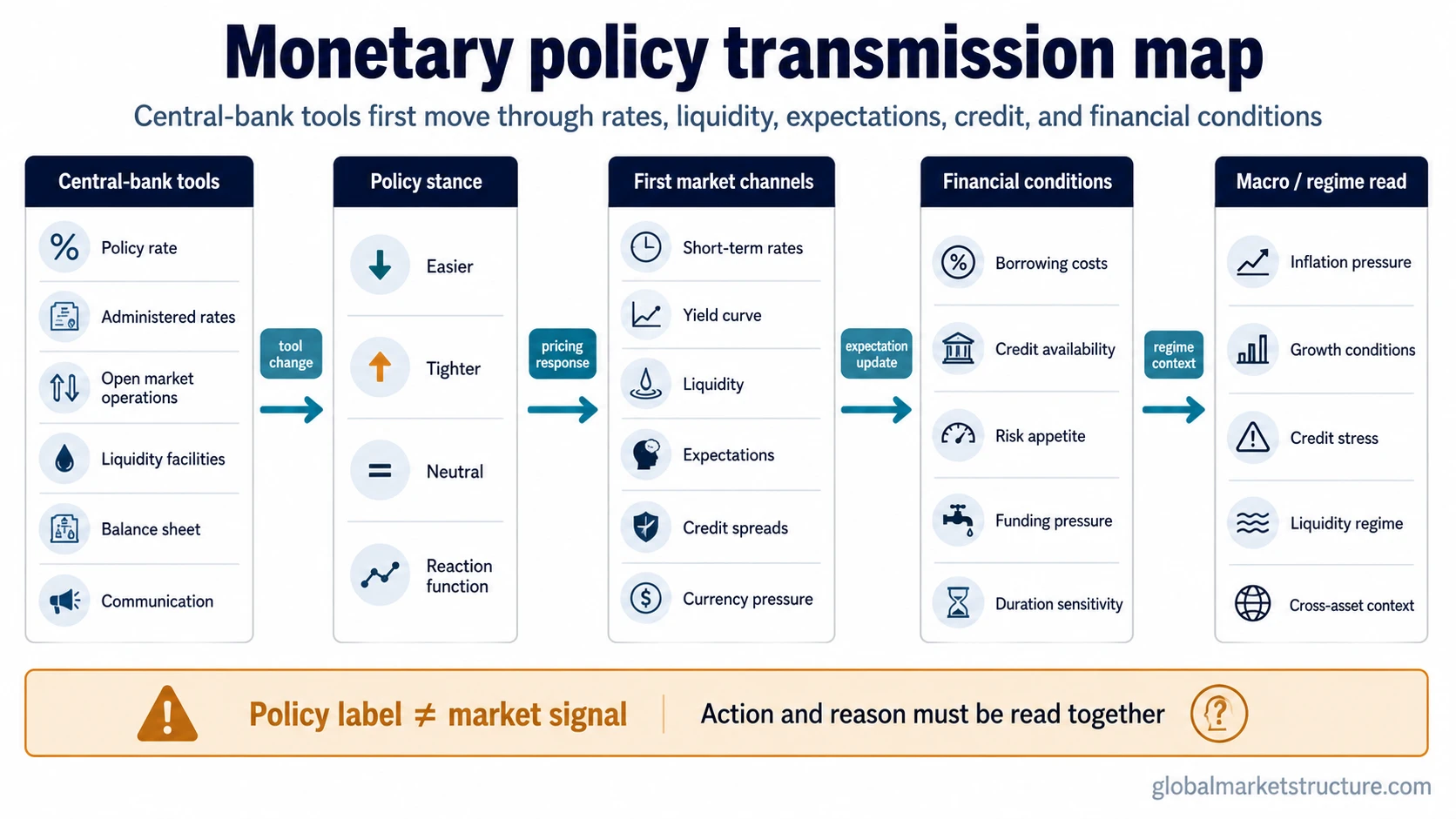

Monetary policy is the set of actions a central bank uses to influence money-market conditions, interest rates, credit, liquidity, expectations, and broader financial conditions. It can affect inflation, employment, economic activity, and market-regime interpretation, but it is not a standalone forecast for asset prices.

Core idea:

- Monetary policy is controlled by a central bank or monetary authority, not by the government budget process.

- Its tools include policy rates, administered rates, open market operations, reserve and liquidity tools, balance-sheet policy, and communication.

- The first market channels are usually rates, liquidity, expectations, credit conditions, the yield curve, currencies, and financial conditions.

- The same policy action can mean different things depending on inflation, growth, credit stress, fiscal policy, and market positioning.

What Monetary Policy Controls

Monetary policy controls the stance and tools of the central bank. It does not directly control every price in the economy or every market outcome. The central bank changes the policy environment, and private markets, banks, borrowers, investors, and households respond through financing costs, credit availability, risk appetite, and expectations.

In the United States, monetary policy is tied to the Federal Reserve’s goals of stable prices and maximum employment. Other central banks use different legal language, but the broad idea is similar: monetary policy adjusts financial conditions to influence inflation, economic activity, credit conditions, and, in some frameworks, financial stability risks.

| Policy layer | Meaning | Why it matters |

|---|---|---|

| Authority | Central bank or monetary authority | Separates monetary policy from government spending and taxation |

| Tools | Rates, reserves, liquidity facilities, balance-sheet policy, communication | Shows how policy is implemented rather than only announced |

| Stance | Easier, tighter, or neutral policy conditions | Frames whether the central bank is trying to support or restrain demand and inflation pressure |

| First channels | Interest rates, liquidity, expectations, credit, yield curve, currency pressure | Connects central-bank decisions to financial conditions |

| Common misread | Treating policy stance as a direct market signal | Markets also react to why policy changed, not only what changed |

Monetary Policy Tools

The most visible monetary policy tool is the policy interest rate. When a central bank raises or lowers its target rate, it changes the reference point for short-term borrowing costs and money-market pricing.

Modern monetary policy also uses administered rates and implementation tools. These can include interest paid on reserve balances, overnight reverse repurchase facilities, discount-window lending, open market operations, and other mechanisms that help the central bank keep short-term rates near its intended range.

Balance-sheet policy is another tool. Asset purchases, reinvestment decisions, and balance-sheet runoff can influence reserves, liquidity conditions, term premia, and the supply of safe assets available to the market. These tools are still monetary policy, but they work differently from a simple policy-rate change.

Central-bank communication also matters. Forward guidance, projections, press conferences, and policy statements can change expectations before or after a tool is adjusted. Markets often respond not only to the action itself, but also to how the central bank describes inflation, labor markets, growth, risks, and future policy reaction functions.

Expansionary vs Contractionary Monetary Policy

Expansionary monetary policy means the central bank is trying to make financial conditions easier. It may lower policy rates, add liquidity, buy assets, or communicate that policy is likely to remain supportive. The intended effect is usually to reduce borrowing costs, support credit creation, and ease pressure on economic activity.

Contractionary monetary policy means the central bank is trying to make financial conditions tighter. It may raise policy rates, reduce balance-sheet support, drain reserves, or signal a more restrictive stance. The intended effect is usually to restrain inflation pressure, cool demand, and slow excessive credit growth.

Important limitation:

Easier policy is not automatically bullish, and tighter policy is not automatically bearish. A rate cut during calm disinflation can carry a different message from a rate cut driven by credit stress or growth deterioration. A rate hike during strong growth can carry a different message from a rate hike that exposes funding pressure. The policy stance must be interpreted together with the reason for the change.

How Monetary Policy First Reaches Markets

Monetary policy reaches markets through first-channel effects before it becomes a broad macro outcome. The first reaction is usually visible in money markets, short-term rates, bond yields, the yield curve, credit spreads, currency pressure, liquidity conditions, and expectations about future policy.

First-channel sequence:

- Central-bank stance: the policy signal becomes easier, tighter, or more neutral.

- Money-market pricing: short-term rates, administered rates, and liquidity tools adjust.

- Expectations: investors update the expected path of inflation, growth, and future policy.

- Credit conditions: lending standards, refinancing costs, credit spreads, and risk appetite may change.

- Financial conditions: the combined effect appears across yields, currencies, equity risk appetite, funding markets, and broader market-regime context.

This sequence is why monetary policy matters for Global Market Structure. It connects central-bank decisions to rates, liquidity, credit, currency pressure, and cross-asset behavior. The useful question is not only whether policy is easier or tighter. The useful question is what policy is changing first and what that change says about the broader regime.

Monetary Policy vs Fiscal Policy

Monetary policy is controlled by central banks. Fiscal policy is controlled through government spending, taxation, transfers, and borrowing decisions. Both can influence demand, inflation, employment, and market conditions, but they begin from different authorities and move through different first channels.

The distinction matters because the same macro environment can contain easy monetary policy and tight fiscal policy, or tight monetary policy and expansionary fiscal policy. That interaction belongs to the policy mix, not to monetary policy alone.

For a direct side-by-side distinction, compare fiscal policy vs monetary policy. The monetary policy concept stays focused on central-bank tools, stance, first channels, and interpretation limits.

Monetary Policy vs the Monetary Transmission Mechanism

Monetary policy is the stance and toolset chosen by the central bank. The monetary transmission mechanism is the detailed path through which those choices move through banks, borrowers, asset prices, exchange rates, expectations, inflation, and economic activity.

The difference is simple: monetary policy is the decision and tool layer; the transmission mechanism is the channel layer. Monetary policy explains the main tools and first effects. Transmission analysis goes deeper into how those effects travel through the economy and financial system.

Why Monetary Policy Can Be Misread

Monetary policy can be misread when the policy label is separated from the macro context. A rate cut can occur because inflation is cooling in a stable economy, or because growth and credit conditions are deteriorating. A rate hike can occur because demand is strong, or because inflation pressure is forcing the central bank to tighten into a fragile environment.

Policy also works with lags. Borrowers do not all refinance at once. Banks do not adjust credit supply instantly. Investors may reprice expectations before households and businesses change behavior. A policy lag can make the effect of monetary policy appear uneven across markets and the real economy.

False-reading risk:

Monetary policy should not be treated as a buy or sell signal. The same easing or tightening label can produce different market outcomes depending on inflation, growth momentum, credit stress, valuation, positioning, fiscal stance, and whether the market had already priced the policy shift.

A useful interpretation separates the action from the reason. The action is what the central bank changed. The reason is the inflation, employment, credit, or growth condition that made the change necessary. Markets often react more strongly to the reason than to the policy label itself.

Where Monetary Policy Fits in Global Market Structure

Monetary policy is a core macro driver because it influences the price and availability of money. It affects the discount-rate environment, liquidity conditions, credit creation, currency pressure, duration sensitivity, and risk appetite across asset classes.

Its market-structure value is strongest when it is read alongside other drivers. A central-bank tightening cycle means something different when inflation is supply-driven, credit spreads are widening, and fiscal policy is expansionary. A central-bank easing cycle means something different when liquidity is improving, credit stress is fading, and growth expectations are stabilizing.

Monetary policy is therefore best used as a regime input. It helps classify the environment, but it does not replace analysis of credit, liquidity, inflation, fiscal stance, market breadth, positioning, or cross-asset confirmation.