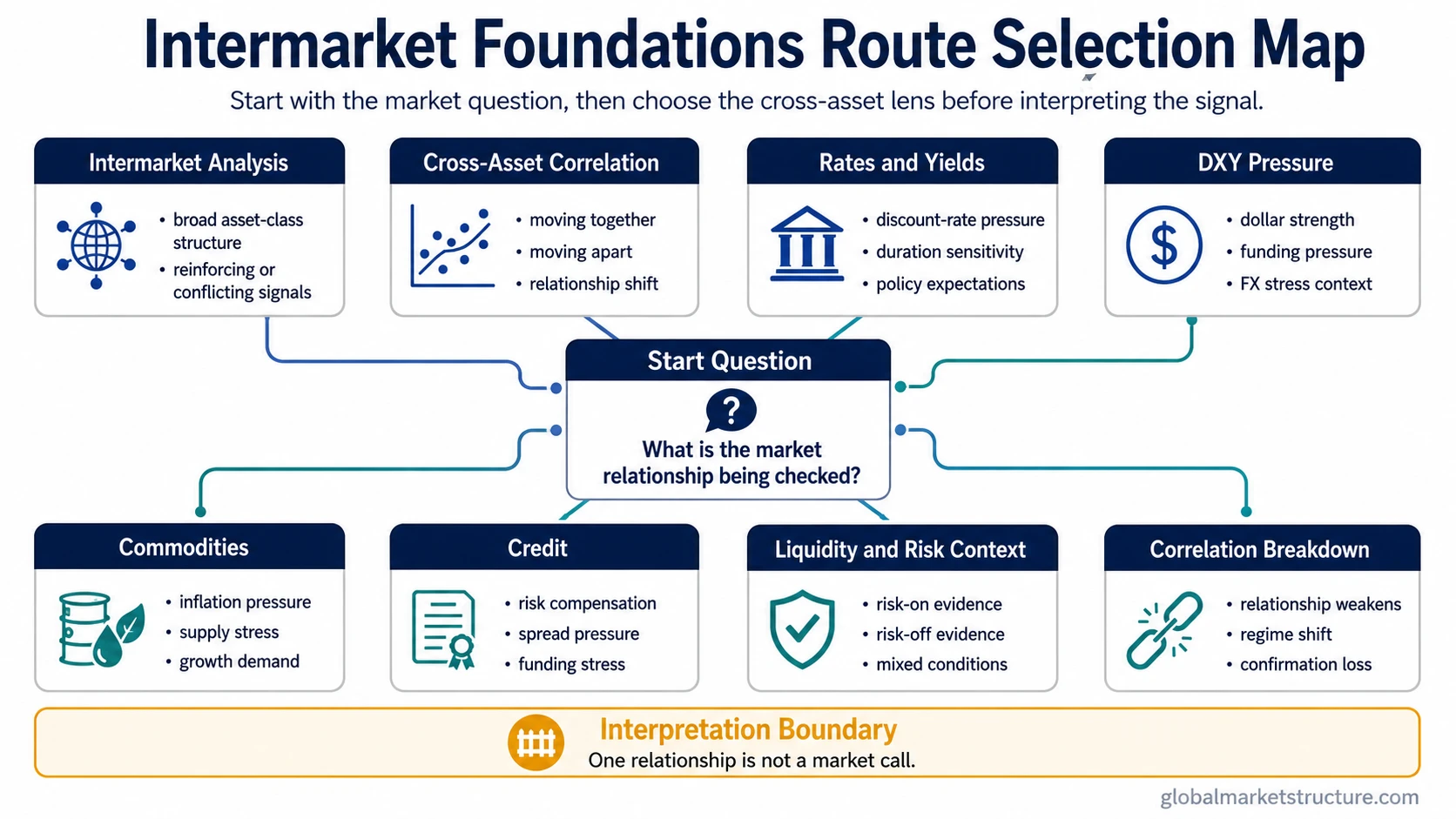

Intermarket Foundations organizes the first routes into cross-asset market structure: intermarket analysis, cross-asset correlation, rates and yields, currency pressure, commodities, credit, liquidity, risk-on/risk-off conditions, and interpretation limits. The useful starting point depends on whether the market question is about a broad relationship map, a correlation lens, a rates channel, dollar pressure, credit stress, commodity behavior, or a boundary where cross-asset readings can mislead.

Start With the Intermarket Question

Intermarket work becomes clearer when the question is separated before the assets are combined. Stocks, bonds, commodities, currencies, yields, credit, and liquidity can all matter, but they do not answer the same question.

A broad intermarket question asks how asset classes are interacting. A correlation question asks whether assets are moving together or apart. A regime question asks whether the surrounding conditions are rewarding risk exposure, demanding safety, or producing mixed evidence.

Choose the Right Intermarket Route

| Market question | Primary lens | Best route | Boundary |

|---|---|---|---|

| How do stocks, bonds, commodities, currencies, and yields fit together? | Broad cross-asset structure | intermarket analysis | Broad relationships need separate confirmation, not one controlling asset. |

| Are asset classes moving together, diverging, or changing their relationship? | Correlation lens | cross-asset correlation | Correlation describes movement, not causation. |

| Are yield changes affecting discount rates, duration sensitivity, or risk appetite? | Rates and yields | Rates and yield analysis | A yield move can reflect growth, inflation, policy expectations, or risk stress. |

| Is currency strength or weakness adding pressure across markets? | DXY and currency pressure | Currency-pressure analysis | Dollar pressure needs liquidity, rates, and global funding context. |

| Are commodity moves pointing to inflation pressure, supply stress, or growth demand? | Commodity context | Commodity-market analysis | Commodity strength can come from different drivers with different market meanings. |

| Is risk compensation changing beneath equity or bond markets? | Credit conditions | Credit-risk analysis | Credit signals become stronger when liquidity and breadth confirm the pressure. |

| Why did a relationship that usually works stop working? | Breakdown risk | correlation breakdown | Relationships can weaken, invert, or disappear when market regimes change. |

Intermarket Analysis vs Cross-Asset Correlation

Intermarket analysis is the broader discipline. It compares asset classes and macro-sensitive markets to understand whether their behavior is reinforcing, conflicting, or changing the interpretation of risk conditions.

Cross-asset correlation is narrower. It focuses on whether assets move together, move apart, or shift relationship over time. A correlation reading can support intermarket analysis, but it cannot replace the broader interpretation of rates, currencies, credit, liquidity, and risk appetite.

The useful distinction is simple: intermarket analysis asks what the relationships may mean; cross-asset correlation asks how closely different markets are moving together.

Core Route Families

Intermarket analysis: Best for broad questions about how equities, bonds, commodities, currencies, yields, and liquidity interact.

Cross-asset correlation: Best for questions about co-movement, diversification behavior, relationship shifts, and correlation instability.

Rates and yields: Best for questions about discount rates, duration pressure, risk-free-rate comparison, real yields, nominal yields, and policy expectations.

DXY and currency pressure: Best for questions about dollar strength, global funding pressure, currency divergence, and the effect of FX stress on risk assets and commodities.

Commodities: Best for questions about inflation pressure, supply shocks, growth demand, real-asset behavior, and commodity-linked macro signals.

Credit: Best for questions about risk compensation, spread widening, stress transmission, funding pressure, and the quality of risk appetite.

Liquidity and risk-on/risk-off: Best for questions about whether markets are rewarding risk exposure, demanding safety, or sending mixed signals across asset classes.

A Simple Route-Selection Scenario

A market can show rising yields, a stronger dollar, weaker commodities, and wider credit spreads at the same time. That combination does not automatically create one conclusion. The cleaner starting point is to separate the rates channel, currency-pressure lens, commodity message, and credit-risk lens before combining them into a broader risk-environment reading.

Where Intermarket Readings Can Mislead

One cross-asset relationship is incomplete on its own. A yield move, currency move, commodity move, spread move, or correlation shift can have more than one driver.

Correlation is especially easy to overread. Two assets moving together does not prove that one caused the other, and a familiar relationship can break down when policy expectations, liquidity, positioning, or risk appetite change.

Current market readings require dated source context. Without current data and a defined time period, intermarket signals should stay at the level of structural interpretation rather than market calls.

What Belongs Outside the Intermarket Foundation Layer

Intermarket foundations do not create trade instructions, stock-picking conclusions, short-term market calls, or single-signal forecasts.

Execution methods belong to trading-process education. Company-level valuation belongs to company-analysis work. Current market claims require dated evidence. Intermarket structure is most useful when it organizes conditions without turning them into unsupported prediction.

Related Routes

Use intermarket analysis when the main question is how major markets interact across equities, bonds, commodities, currencies, yields, liquidity, and risk appetite.

Use cross-asset correlation when the main question is whether assets are moving together, diverging, or changing relationship under different conditions.

Use correlation breakdown when the main question is why a relationship that often matters has weakened, inverted, or stopped giving useful confirmation.