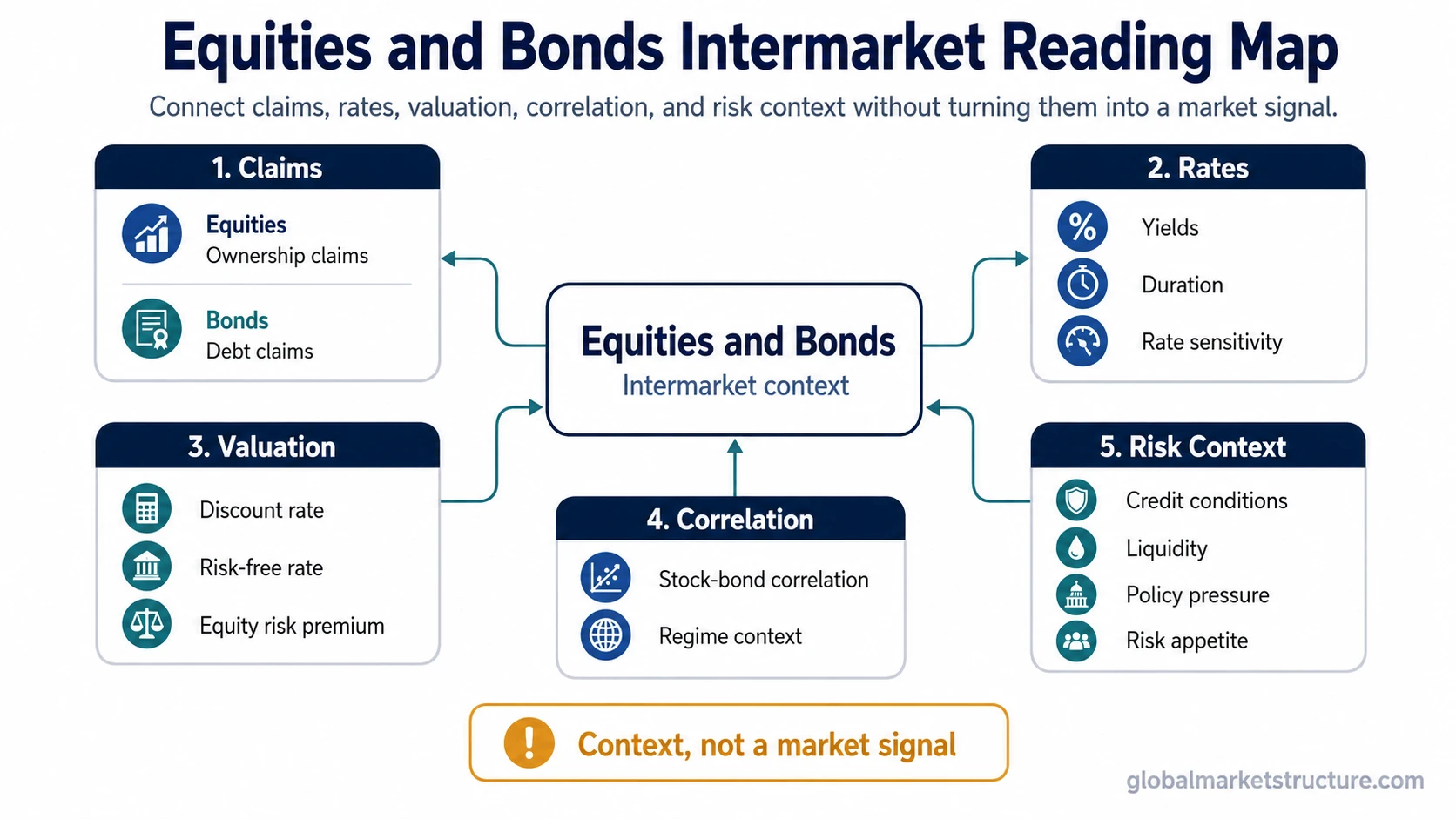

Equities and bonds connect stock-market ownership claims with bond-market debt claims, rate sensitivity, discount-rate effects, credit conditions, equity risk premium, and stock-bond correlation. The relationship is contextual, not a mechanical forecast.

Start With the Question You Are Trying to Answer

Equities and bonds can be compared as asset classes, but the more useful market-structure reading starts by identifying whether the question is about claims, rates, valuation, duration, correlation, or risk context.

| Reader question | Start with | Why it belongs there |

|---|---|---|

| What is the equity side of the relationship? | Equities | Use this when the question is about ownership claims, equity-market participation, earnings sensitivity, and equity-side market behavior. |

| What is the bond side of the relationship? | Bond market | Use this when the question is about debt claims, issuance, secondary trading, yield behavior, and bond-market structure. |

| Do stocks and bonds move together or apart? | Stock-bond correlation | Use this when the question is about changing correlation regimes, inflation context, policy stress, and risk-off interpretation. |

| Why do rate changes affect market sensitivity? | Duration risk | Start here when the main issue is sensitivity to changes in rates, yields, and discounting conditions. |

| How are equities judged against benchmark returns? | Equity risk premium | Use this when the question is about equity compensation relative to a risk-free benchmark. |

| Why do valuation assumptions change when rates change? | Discount rate | Use this when the question is about the valuation channel that links future cash flows, present value, and rate assumptions. |

| Why do longer bonds react more to yield changes? | Bond duration | Use this when the question is about bond-price sensitivity, maturity structure, and the mechanics of rate exposure. |

| What benchmark connects bonds and equity valuation? | Risk-free rate | Use this when the question is about the baseline rate used in valuation, opportunity cost, and risk-premium interpretation. |

Equities Versus Bonds in One Distinction

Equities are ownership claims. Bonds are debt claims. That distinction matters because equity holders participate in business upside and downside, while bondholders are tied to contractual payment structure, credit quality, maturity, and yield conditions.

The distinction is only the starting point. Intermarket analysis asks how the two markets interact when rates, inflation expectations, credit spreads, policy conditions, liquidity, and risk appetite change.

How the Equity-Bond Mechanisms Split

Claims: questions about ownership, earnings exposure, and equity-market participation belong with equities. Questions about debt, coupons, maturity, issuance, and yield behavior belong with the bond market.

Rates: questions about why yields and rate expectations change market sensitivity belong with duration risk, bond duration, discount rate, and risk-free rate.

Valuation: questions about how rate assumptions affect present value, required return, and relative compensation belong with discount rate and equity risk premium.

Correlation: questions about whether stocks and bonds offset each other, move together, or stop diversifying the same way belong with stock-bond correlation.

Risk context: questions about stress, liquidity, credit pressure, and changing market regime should be read as context, not as a standalone signal from either asset class.

What Equity-Bond Readings Cannot Tell You Alone

Equity-bond relationships are not mechanical. A rise in yields does not automatically forecast equity weakness, and a changing stock-bond correlation does not create a direct market signal. The same move can mean different things depending on inflation expectations, policy pressure, growth expectations, credit conditions, and liquidity.

The safer reading is to identify the mechanism first, then interpret the broader market environment.

A Simple Reading Sequence

| Step | Question | Interpretation path |

|---|---|---|

| 1 | Is the question about the asset claim itself? | Separate equities as ownership claims from bonds as debt claims. |

| 2 | Is the question about rate sensitivity? | Move into duration risk, bond duration, discount rate, and risk-free rate. |

| 3 | Is the question about valuation pressure? | Check discount-rate assumptions and equity risk premium. |

| 4 | Is the question about diversification or co-movement? | Move into stock-bond correlation and regime context. |

| 5 | Is the question about stress or risk appetite? | Read credit, liquidity, and broader market regime before forming a conclusion. |

Not an Allocation Guide

Equities and bonds are often discussed in portfolio-allocation language, but this Global Market Structure section is not designed to tell readers which asset to own. The stronger use is to understand which market mechanism is being observed and which concept explains it.