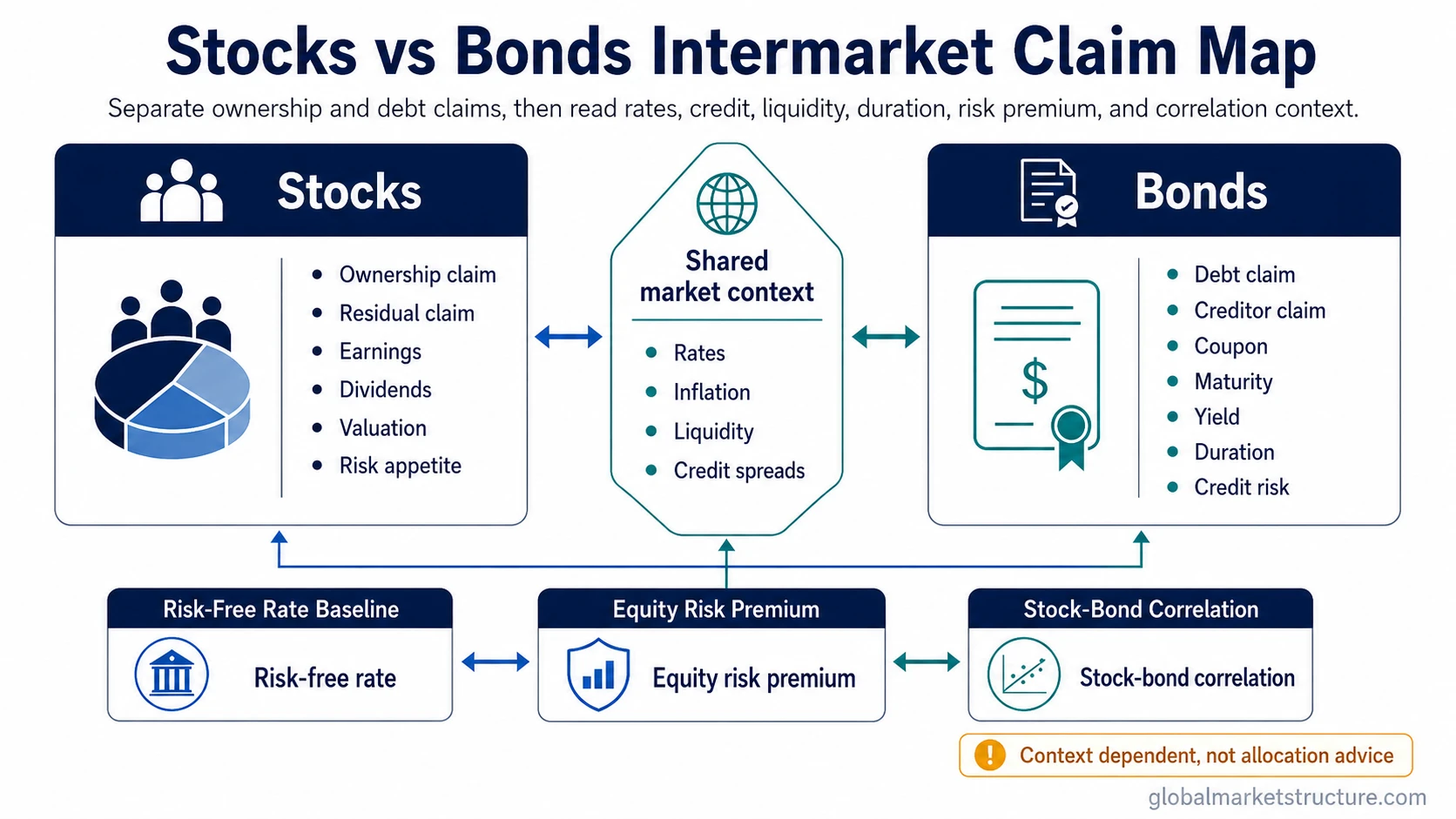

Stocks are ownership claims on businesses, while bonds are debt claims on issuers. Stocks are mainly read through earnings, dividends, valuation, and risk appetite. Bonds are mainly read through coupon, maturity, yield, duration, issuer credit, and rate context. In market-structure analysis, the comparison also depends on the risk-free-rate baseline, equity risk premium, credit conditions, liquidity, and stock-bond correlation.

Stocks vs Bonds: Direct Comparison

The cleanest distinction is claim type. A stock represents residual ownership in a business. A bond represents a contractual lending claim against an issuer. That difference changes how each security responds to growth expectations, rates, credit stress, liquidity, and investor risk appetite.

| Comparison point | Stocks | Bonds |

|---|---|---|

| Claim type | Ownership claim on a business | Debt claim on an issuer |

| Cash-flow source | Earnings, dividends, buybacks, and changing business value | Coupon payments, principal repayment, and yield |

| Main return driver | Growth, margins, valuation multiples, and risk appetite | Coupon income, yield changes, maturity, duration, and credit quality |

| Main risk lens | Business risk, valuation risk, earnings risk, and liquidity conditions | Interest-rate risk, duration risk, credit risk, inflation risk, and liquidity risk |

| Rate sensitivity | Often works through discount rates, valuation pressure, and equity risk premium | Often works directly through the price-yield relationship and duration |

| Market-structure role | Risk-asset claim tied to earnings and risk appetite | Rates and credit claim tied to yield, maturity, and issuer solvency |

What Stocks Represent

Stocks represent equity ownership. Common shareholders participate in the upside and downside of a business after contractual obligations have been considered. That makes equities sensitive to earnings expectations, valuation multiples, dividends, buybacks, margins, liquidity, and changes in risk appetite.

The stock side of the comparison is not only about volatility. A stock is a residual claim. If business expectations improve, valuation support may strengthen. If margins compress, funding conditions tighten, or risk appetite falls, the same ownership claim can reprice even when the company still operates normally.

What Bonds Represent

Bonds represent debt claims. A bond issuer borrows capital and agrees to defined payment terms, usually including coupon payments and principal repayment at maturity. The bond market therefore connects issuer financing, investor income demand, interest-rate expectations, and credit risk.

The bond side of the comparison is not automatically risk-free. Bond prices can change when yields move, credit quality changes, inflation expectations shift, or liquidity weakens. Longer cash-flow timing can increase sensitivity to yield changes, which is why bond duration matters when rates move.

Where Stocks and Bonds Are Similar

Stocks and bonds both help issuers access capital. Both can trade in secondary markets. Both can be affected by liquidity, risk appetite, inflation expectations, and changes in the cost of capital.

The similarity ends where the claim structure changes. A stockholder owns a residual business claim. A bondholder owns a contractual debt claim. That distinction changes the cash-flow profile, risk hierarchy, valuation logic, and market reaction to the same macro input.

Main Differences Between Stocks and Bonds

Claim structure: Stocks sit on the ownership side of the capital structure. Bonds sit on the lending side. That difference affects how upside, downside, and issuer stress are interpreted.

Cash-flow uncertainty: Stock cash flows depend on business performance and corporate decisions. Bond cash flows are more contractual, but still depend on issuer solvency and market pricing.

Valuation driver: Stocks are often valued through earnings power, growth, margins, and multiples. Bonds are often valued through coupon, maturity, yield, duration, and credit spread.

Macro sensitivity: Stocks often respond to rates through discount-rate pressure, valuation changes, and risk appetite. Bonds often respond more directly to yield movement and duration exposure.

Risk interpretation: Stocks are not simply “growth assets,” and bonds are not simply “safe assets.” Both need context from rates, inflation, credit, liquidity, and correlation behavior.

How Rates Connect Stocks and Bonds

Rates connect the two markets because they shape the baseline return available from safer instruments and influence how investors price risk. The risk-free rate acts as a reference point for valuation, yield comparison, and required compensation for uncertainty.

For stocks, that link often appears through the equity risk premium. If safer yields rise, investors may demand more compensation for holding uncertain equity cash flows. For bonds, the rate link is more direct because yield movement changes the present value of fixed payments, especially when duration is high.

Mechanism Contrast: Same Macro Input, Different Transmission

| Macro input | Stock-market channel | Bond-market channel |

|---|---|---|

| Higher yields | Can pressure valuation multiples, raise return hurdles, and change risk appetite | Can reduce prices of existing bonds, especially when duration is high |

| Wider credit spreads | Can signal weaker risk appetite, tighter financing, or concern about earnings quality | Can lower risky bond prices and raise borrowing compensation demanded from issuers |

| Tighter liquidity | Can reduce speculative appetite and weaken support for higher-multiple assets | Can widen bid-ask conditions and pressure lower-quality or less-liquid bonds |

| Falling growth expectations | Can weaken earnings expectations and equity leadership | Can support higher-quality bonds if yields fall, but credit risk may still matter |

Why “Stocks Are Risky and Bonds Are Safe” Is Too Simple

Bonds can carry duration risk, credit risk, liquidity risk, and inflation risk. A government bond, an investment-grade corporate bond, and a high-yield bond do not carry the same market-structure meaning.

Stocks can carry more visible price volatility, but the reason for that volatility matters. Equity weakness caused by lower earnings expectations is different from equity weakness caused by rising discount rates, credit stress, or forced liquidity reduction.

Diversification is also regime-dependent. If inflation or rate pressure affects both markets at the same time, stocks and bonds can weaken together. If growth fear dominates and yields fall, higher-quality bonds may behave differently from equities. The difference depends on the surrounding regime, not on a fixed rule.

Same-Scenario Example: Rising Yields

Consider a generic environment where yields rise quickly. Existing longer-duration bonds may fall because their fixed payments become less attractive relative to newer yields. The effect can be stronger when maturity is longer and duration is higher.

Stocks can react through a different channel. Higher yields can raise the discount rate applied to future earnings, make valuation multiples harder to justify, and increase the return hurdle for risk assets. That does not mean rising yields always hurt stocks. The interpretation changes if yields are rising because growth expectations are improving rather than because inflation pressure, policy stress, or liquidity tightening is increasing.

The same yield move can therefore affect both markets, but not for the same reason. Bond prices are usually closer to the rate and duration channel. Stock prices are usually filtered through earnings expectations, valuation, risk appetite, and the relative appeal of safer yields. The broader mechanics behind how bond yields affect stocks depend on the source of the yield move.

Stock-Bond Correlation and Regime Context

Stock-bond correlation describes whether stocks and bonds are moving together or in opposite directions over a given period. The correlation is not fixed. It can change when inflation pressure, policy expectations, credit conditions, liquidity, or growth risk becomes the dominant market input.

Negative correlation can make bonds behave as a stronger diversifier against equity weakness. Positive correlation can reduce that protection when both markets are responding to the same pressure, such as a sharp rates shock or broad liquidity tightening. For market-structure interpretation, the correlation regime often matters as much as the basic stock-versus-bond distinction.

How to Interpret the Comparison Without Turning It Into Allocation Advice

The practical distinction is not that one asset class is always better than the other. Stocks and bonds answer different questions in the market structure.

Stocks help read business expectations, earnings confidence, valuation tolerance, and risk appetite. Bonds help read rates, credit conditions, duration pressure, income demand, and financing stress. Together, they can show whether markets are rewarding risk, demanding yield, seeking safety, or repricing the cost of capital.

FAQ

What is the main difference between stocks and bonds?

Stocks are ownership claims on businesses. Bonds are debt claims on issuers. That difference changes cash-flow rights, risk exposure, valuation logic, and market sensitivity.

Are bonds always safer than stocks?

No. Bonds can carry duration risk, credit risk, inflation risk, and liquidity risk. The risk profile depends on issuer quality, maturity, rate sensitivity, and market conditions.

Can stocks and bonds fall at the same time?

Yes. Stocks and bonds can both fall when the dominant pressure affects both markets, such as a sharp rates shock, inflation pressure, liquidity tightening, or broad risk repricing.

Why do higher yields matter for stocks?

Higher yields can raise the return hurdle for equities, affect discount rates, pressure valuation multiples, and change the relative appeal of risk assets. The effect depends on why yields are rising.

Is the stock-bond split enough to understand market risk?

No. The split is useful, but market risk also depends on rates, credit spreads, liquidity, inflation expectations, earnings conditions, and correlation behavior.