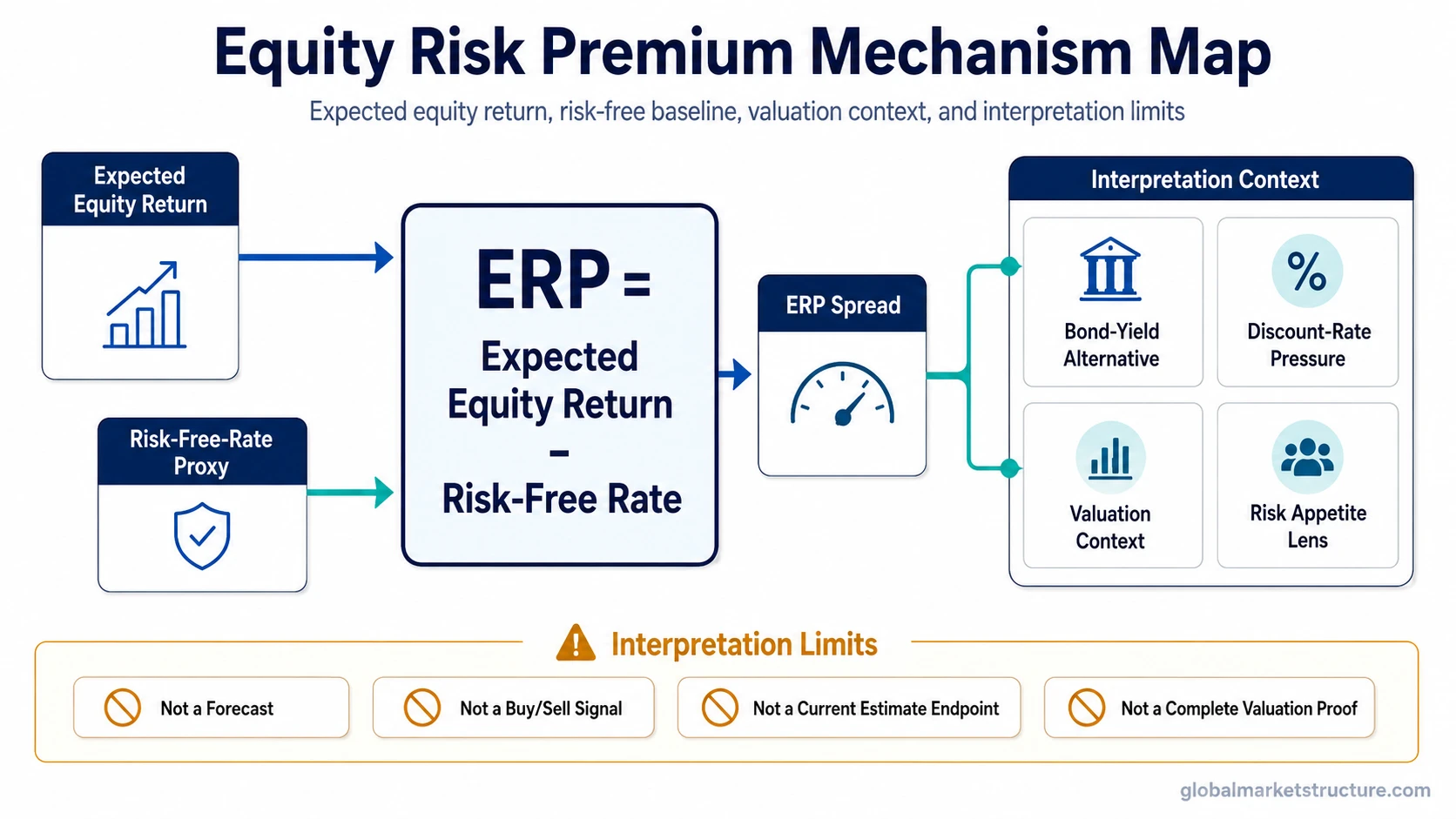

Equity risk premium is the extra expected or required return investors demand from equities above a risk-free baseline. In compact form, it is the expected equity return minus the risk-free rate. It helps compare equity compensation against safer rate benchmarks, but it is not a guaranteed return forecast, not a trading signal, and not a complete risk model.

Direct definition: Equity risk premium, often shortened to ERP, is the compensation spread between the return expected from equities and the return available from a risk-free rate proxy. The concept exists because equities carry uncertainty around earnings, valuation, liquidity, and market risk that a baseline government-rate proxy is not meant to capture.

Compact formula: Equity risk premium = expected equity return – risk-free rate.

Key Points

- ERP measures expected or required equity compensation above a risk-free baseline.

- A narrower ERP can mean equities offer less extra compensation relative to rates, but that reading still depends on earnings expectations, liquidity, and risk appetite.

- A wider ERP can mean investors require more compensation for equity risk, but it can also reflect fear, uncertainty, or weaker confidence.

- ERP estimates vary because expected equity returns are modeled, not directly quoted like a market price.

- ERP is most useful as an intermarket concept connecting equities, bond yields, discount rates, risk appetite, and valuation pressure.

What Equity Risk Premium Means

Equity risk premium means the additional return investors expect, or require, for holding equities instead of a lower-risk baseline asset. The baseline is usually represented by a government bond yield or another risk-free-rate proxy, depending on the market, currency, and model being used.

The key word is premium. ERP is not the whole expected equity return. It is the portion above the baseline rate. If the baseline rate rises while expected equity returns do not rise by the same amount, the premium can narrow. If expected equity returns rise faster than the baseline rate, the premium can widen.

| ERP means | ERP does not mean |

|---|---|

| Extra expected or required equity compensation above a risk-free baseline. | A guaranteed return that investors will receive. |

| A valuation and cost-of-equity input. | A complete valuation proof by itself. |

| A way to compare equity compensation against bond-rate alternatives. | A direct instruction to buy or sell equities. |

| A useful lens for risk appetite and required return. | A forecast of where stocks, bond yields, or the economy will go next. |

Equity Risk Premium Formula

The simplest equity risk premium formula is:

Equity risk premium = expected equity return – risk-free rate

The expected equity return is not directly observable. It may be estimated from historical returns, earnings yields, dividend and growth assumptions, implied valuation models, analyst expectations, or survey-based methods. Because the expected return input is modeled, ERP estimates can differ across providers and methods.

The risk-free-rate input is also a proxy, not a perfect real-world certainty. In many market discussions, a government bond yield is used as the baseline because it represents a widely watched reference point for required return. The chosen maturity, currency, inflation adjustment, and model horizon can change the interpretation.

ERP also appears in cost-of-equity models, including CAPM-style frameworks. ERP is broader than CAPM-style cost-of-equity modeling because market-structure interpretation also depends on bond yields, liquidity conditions, expected returns, and risk appetite.

How ERP Connects Equities and Bonds

ERP sits directly between equity return expectations and bond-market alternatives. When government bond yields are low, equities may appear to offer a larger spread over the baseline, all else equal. When government bond yields rise, the same expected equity return can look less attractive because the baseline has moved higher.

This is why ERP belongs inside intermarket analysis. It connects the equity market to the bond market through required return. A move in bond yields can change the compensation investors require from equities even if company earnings have not changed immediately.

The relationship is conditional. Higher yields do not automatically hurt equities, and lower yields do not automatically support equities. The interpretation depends on why yields are moving. A yield rise driven by stronger real growth expectations may be read differently from a yield rise driven by inflation pressure, policy tightening, or rising term premium.

| Market condition | Possible ERP interpretation | Key limitation |

|---|---|---|

| Risk-free-rate proxy rises while expected equity return is unchanged. | ERP can narrow because the baseline return has increased. | This does not prove equities are overvalued without checking earnings expectations and risk appetite. |

| Expected equity return rises faster than the risk-free baseline. | ERP can widen, suggesting investors require or expect more equity compensation. | A wider premium may reflect fear, uncertainty, or weaker confidence, not only opportunity. |

| Real yields rise while equity growth expectations weaken. | Valuation pressure can increase because the required-return hurdle becomes harder to clear. | The effect depends on sector mix, earnings durability, and liquidity conditions. |

| Credit spreads widen and liquidity weakens. | ERP may be read alongside broader risk compensation and risk-off behavior. | ERP alone does not identify the cause or timing of market stress. |

ERP, Discount Rates, and Valuation Pressure

Equity risk premium is closely related to the discount rate, but the two are not the same. ERP is the extra equity compensation above the risk-free baseline. A discount rate is the broader required-return rate used to convert expected future cash flows into present value.

In many valuation frameworks, the required return for equities combines a risk-free-rate component with one or more risk premium components. When either component rises, the discount rate can rise. A higher discount rate can reduce the present value of future cash flows if cash-flow expectations do not increase enough to offset it.

This is the valuation-pressure channel. It does not require a short-term market prediction. It simply explains why rising required returns can change the price investors are willing to pay for the same expected cash-flow stream.

Important boundary: ERP helps explain required-return pressure, not market timing. A valuation framework can show why the hurdle rate has changed, but it cannot prove the next equity-market move by itself.

Bond Yields, Real Yields, and ERP Interpretation

Bond yields matter for ERP because they help define the baseline return available outside equities. Real yields can matter materially for valuation-sensitive assets because they reflect the return after expected inflation, depending on the model and market context.

A useful scenario is a period where real yields rise while expected equity returns do not rise by the same amount. The equity risk premium can look narrower because the safer baseline has improved relative to equities. That can create valuation pressure, especially for longer-duration equity cash flows. The read becomes stronger if earnings expectations weaken, liquidity tightens, and market breadth deteriorates at the same time.

The same yield move can have a different interpretation if it reflects stronger growth, resilient earnings, and stable credit conditions. In that case, the higher baseline rate may be partly offset by better equity cash-flow expectations. For broader yield transmission, the related mechanism is covered by how bond yields affect stocks.

Illustrative scenario: Suppose the risk-free-rate proxy rises from a low level while expected equity returns remain broadly unchanged. The ERP narrows because the baseline moved higher. That does not automatically mean equities should fall. It means the equity market may need stronger earnings growth, easier liquidity, lower risk perception, or a lower valuation multiple to justify the same price level.

ERP Versus Duration Risk

Equity risk premium should not be confused with duration risk. ERP measures compensation above a risk-free baseline. Duration risk measures sensitivity to changes in yields, interest rates, or required returns.

ERP: asks how much extra equity compensation exists above a baseline rate.

Duration risk: asks how sensitive an asset’s value may be when required returns or yields change.

The concepts can interact. A market with a narrow ERP and high duration sensitivity may be more exposed to required-return pressure than a market with a wider ERP and lower sensitivity. But ERP itself is not a duration measure, and duration risk is not an equity compensation spread.

Why ERP Estimates Vary

ERP estimates vary because expected equity return is not a directly quoted market price. Different analysts and providers may use historical return averages, implied valuation models, earnings-yield methods, dividend growth assumptions, survey estimates, or forward-looking cash-flow assumptions.

The risk-free-rate proxy also changes the result. A short-term bill rate, a 10-year government bond yield, a real yield, or a currency-specific benchmark can lead to different readings. Time horizon matters as well because a near-term risk premium estimate may not mean the same thing as a long-run equity premium assumption.

Source-endpoint boundary: Current ERP values should come from dated provider, academic, or official datasets that disclose method and assumptions. The durable use of ERP is conceptual and interpretive; live values require dated methodology and source disclosure.

Common False Readings of Equity Risk Premium

ERP is useful because it keeps equity return expectations tied to a baseline rate instead of reading equities in isolation. It becomes dangerous when it is treated as a mechanical signal.

False reading 1: A low ERP means investors should sell equities. A low ERP may suggest less compensation for equity risk, but the interpretation still depends on earnings expectations, liquidity, positioning, and why the risk-free baseline changed.

False reading 2: A high ERP means equities are automatically cheap. A high ERP may reflect elevated fear, recession risk, earnings uncertainty, or liquidity stress rather than a clean opportunity.

False reading 3: ERP predicts future equity returns directly. ERP is a modeled compensation spread. It can support valuation and regime interpretation, but it does not guarantee realized returns.

False reading 4: ERP can be read without bonds. Because the formula depends on a risk-free-rate baseline, bond yields and real yields are part of the interpretation.

How to Use ERP in Market Structure Analysis

ERP is most useful in market-structure analysis as a cross-asset interpretation tool. It helps explain how equity valuation pressure can change when bond yields, real yields, earnings expectations, and risk appetite move in different directions.

A better read combines ERP with surrounding evidence. Equity compensation looks more fragile when the premium is narrow, real yields are rising, liquidity is tightening, and earnings expectations are weakening. The same ERP level may be less restrictive when earnings expectations are improving, credit conditions are stable, and liquidity is supportive.

ERP defines one compensation spread: expected or required equity return above a risk-free-rate proxy. A broader stocks vs bonds comparison also has to account for duration, credit risk, volatility, income stability, inflation exposure, and portfolio role.

FAQ

What is the basic equity risk premium formula?

The compact formula is equity risk premium = expected equity return – risk-free rate. The expected equity return is usually modeled, while the risk-free rate is usually represented by a government-rate proxy.

Is equity risk premium the same as the discount rate?

No. Equity risk premium is one risk compensation component. A discount rate is the broader required-return rate used to value future cash flows. The discount rate may include a risk-free-rate component plus risk premium components.

Does a low equity risk premium mean stocks should fall?

No. A low ERP can suggest that equities offer less extra compensation relative to the baseline rate, but it is not a market-timing signal. Earnings expectations, liquidity, real yields, positioning, and risk appetite still matter.

Why do equity risk premium estimates differ?

ERP estimates differ because expected equity returns are modeled rather than directly quoted. Historical, implied, survey-based, and earnings-based methods can produce different results, especially when the risk-free-rate proxy or time horizon changes.