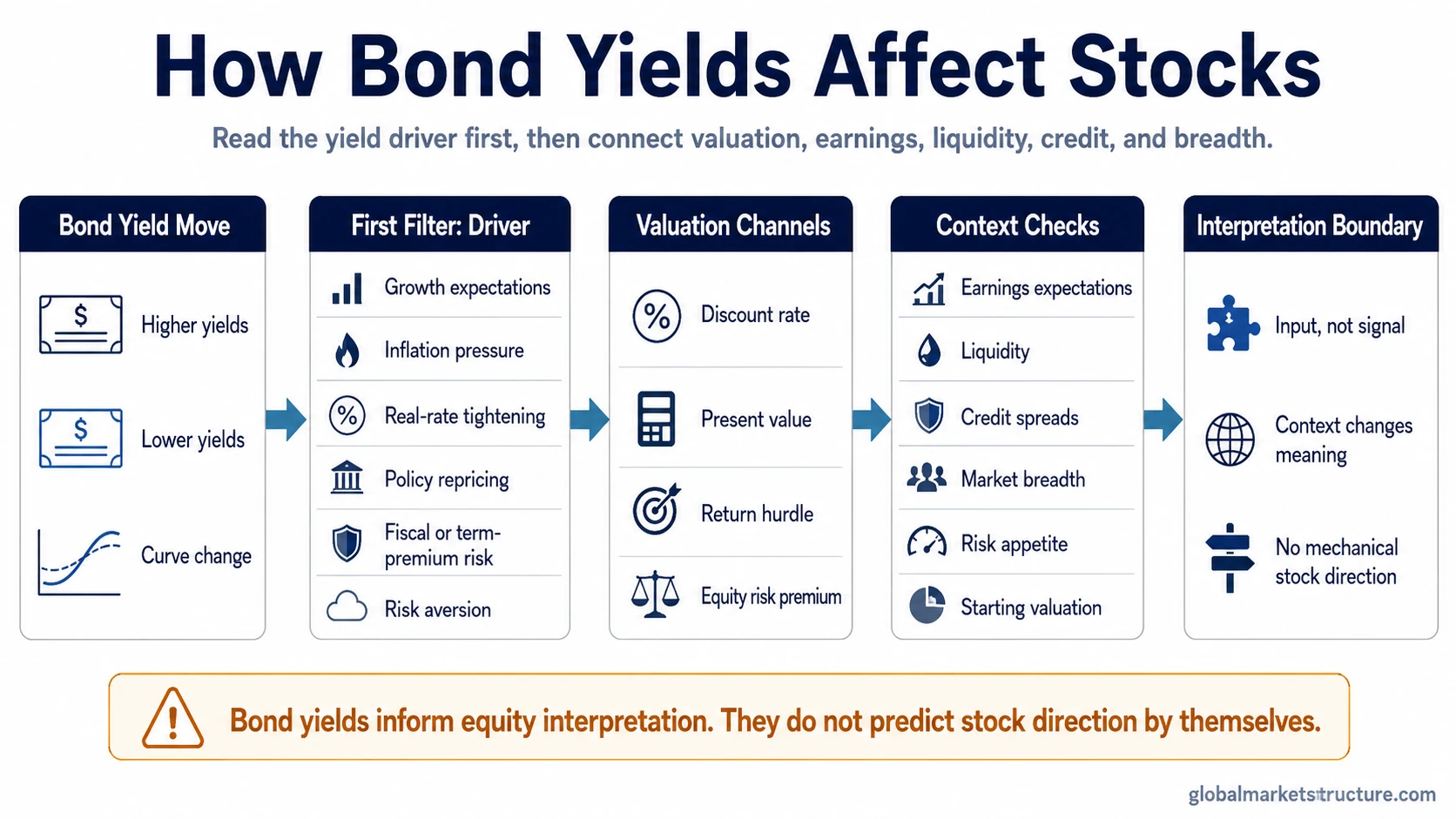

Bond yields affect stocks mainly by changing the discount rate applied to future corporate cash flows and by changing the return hurdle equities must clear. Higher yields can pressure valuation multiples, especially when real yields rise or financial conditions tighten, but the equity effect depends on why yields are moving and whether earnings, liquidity, credit, and risk appetite confirm or offset the pressure. After direction, the first filter is the driver of the yield move.

Direct answer: Bond yields are an intermarket input for equity valuation. They influence stocks through discount rates, risk-free-rate comparison, equity risk premium, earnings expectations, and the broader risk environment. They do not mechanically predict stock direction.

Key Points

- Bond yields affect stock valuations because higher benchmark yields can raise the discount rate used to value future earnings and cash flows.

- The reason yields move matters. A yield rise driven by stronger growth can affect equities differently from a yield rise driven by inflation pressure, real-rate tightening, fiscal risk, or risk aversion.

- Bond yields should be read with earnings expectations, liquidity, credit spreads, market breadth, valuation starting point, and risk appetite rather than treated as a standalone equity signal.

Why Bond Yields Affect Stock Valuations

The core valuation channel is the discount rate. When benchmark yields rise, the rate used to discount future corporate cash flows can also rise. A higher discount rate reduces the present value of distant cash flows, all else equal, which can pressure valuation multiples.

The second channel is the return hurdle. Government bond yields often act as a reference point for the risk-free-rate component in market valuation. When that reference yield rises, equities may need stronger earnings growth, lower risk perception, or a wider expected return premium to remain attractive relative to bonds.

That does not mean higher yields automatically push stocks lower. If yields rise because growth expectations and earnings expectations are improving, the earnings side of the equity equation can offset some valuation pressure. If yields rise because real rates, policy pressure, inflation uncertainty, or fiscal risk are tightening financial conditions, the pressure on equity multiples can become harder to absorb.

The Yield Driver Matters

The same yield move can carry different equity meaning depending on its driver. Yield direction is only the first observation. The more useful question is what the yield move is repricing.

| Yield condition | Possible driver | Equity channel | Limitation |

|---|---|---|---|

| Higher yields with stronger growth | Better growth and earnings expectations | Valuation pressure may be partly offset by stronger expected cash flows | Requires confirmation from margins, breadth, liquidity, and earnings revisions |

| Higher real yields | Tighter real discount-rate pressure | Longer-duration equities may face greater multiple pressure | Strong earnings, cash-flow durability, and improving risk appetite can soften the impact |

| Higher nominal yields from inflation pressure | Inflation expectations or policy repricing | Higher cost pressure and rate uncertainty can weigh on valuation | Sector exposure, pricing power, margin structure, and policy response change the reading |

| Falling yields from growth fear | Risk-off behavior or weaker growth expectations | Discount-rate relief may not help if earnings expectations fall faster | Lower yields can still be negative for equities when they reflect deteriorating growth |

| Steeper yield curve | Growth, inflation, term premium, or fiscal-risk repricing | Can change sector leadership and macro interpretation | Curve shape is context, not an equity timing model |

Boundary: A yield move is not enough by itself. The interpretation improves when the yield driver is checked against earnings expectations, liquidity conditions, credit spreads, valuation levels, and market breadth.

Real Yields vs Nominal Yields

Nominal yields show the stated yield before adjusting for inflation expectations. They can rise because investors are repricing stronger growth, higher inflation, tighter policy, higher term premium, or more compensation for fiscal and duration risk.

Real yields adjust the yield picture for inflation expectations. For equities, rising real yields can create clearer valuation pressure because they point more directly to a higher real discount-rate hurdle. This tends to matter more for companies whose expected value depends heavily on cash flows far in the future.

The distinction matters because a nominal yield rise caused by stronger growth can be easier for equities to absorb than a real-yield rise caused by tighter financial conditions. The equity reading depends on which part of the yield move is doing the work.

Equity Risk Premium and the Return Hurdle

The equity risk premium is the extra compensation investors require for owning equities instead of lower-risk bonds. When benchmark yields rise, equities may need stronger expected earnings growth or lower perceived risk to justify the same valuation multiple.

This is why bond yields can affect stocks even when company fundamentals have not changed immediately. A higher risk-free-rate reference can change the comparison set. The same stream of expected earnings may look less valuable if the safer benchmark return has risen.

Equity risk premium should not be reduced to a simple threshold. Its interpretation changes with the earnings cycle, inflation regime, policy conditions, credit risk, liquidity, investor positioning, and valuation starting point.

Yield Curve Context

The level of bond yields matters, but the shape of the yield curve can also change the reading. A move in short-term yields can reflect policy-rate expectations. A move in long-term yields can reflect growth expectations, inflation expectations, term premium, or fiscal-risk repricing.

A flattening curve, steepening curve, or inversion can help classify the macro backdrop, but it should not be treated as a direct stock-market timing model. Equity interpretation still depends on whether the curve move is aligned with earnings revisions, credit conditions, liquidity pressure, and risk appetite.

Which Stocks Can Be More Sensitive

Stocks with more of their expected value tied to distant future cash flows can be more sensitive to changes in discount rates. This is why long-duration growth equities are often discussed when real yields rise.

The sensitivity is not automatic. A company with strong earnings revisions, durable margins, high cash-flow visibility, or improving demand can absorb higher yields better than a company whose valuation depends mainly on distant expectations. Starting valuation matters because a richly valued equity has less room for the discount-rate assumption to move against it.

Rate-sensitive sectors can also react differently depending on the reason yields are moving. A yield rise from stronger nominal growth is not the same as a yield rise from restrictive policy pressure or deteriorating bond-market risk appetite.

Failure-Mode Example

Illustrative scenario: Suppose the 10-year yield rises in two different environments. In the first, yields rise while earnings revisions improve, credit spreads remain contained, liquidity conditions stay orderly, and market breadth broadens. Stocks may absorb part of the valuation pressure because the expected cash-flow outlook is improving at the same time.

In the second, yields rise while real rates move higher, earnings revisions soften, credit spreads widen, liquidity becomes less forgiving, and market breadth narrows. The same yield direction now carries a different message. The pressure is not just a higher discount rate; it is a tighter financial backdrop with weaker confirmation from the equity side.

The failure mode is reading the yield move alone. The more useful process is to ask whether earnings, credit, liquidity, breadth, and valuation starting point confirm the yield story or contradict it.

Common Mistakes

- Assuming higher yields always hurt stocks: Higher yields can pressure valuation, but stronger growth and earnings expectations may offset part of that pressure.

- Assuming lower yields always help stocks: Lower yields can support valuation math, but they can also reflect weaker growth, risk aversion, or falling earnings expectations.

- Treating the yield curve as a stock timing model: Curve shape helps interpret the macro backdrop, but it does not provide a direct equity timing rule.

- Ignoring the yield driver: Growth, inflation, real-rate, policy, liquidity, and fiscal-risk repricing can create different equity implications.

Related Concepts

- Bond yields: the benchmark yield layer behind rate-sensitive equity interpretation.

- Discount rate: the valuation channel that connects benchmark yields to the present value of future cash flows.

- Equity risk premium: the extra compensation investors require for equity risk relative to safer benchmarks.

FAQ

Do higher bond yields always hurt stocks?

No. Higher bond yields can pressure stock valuations by raising the discount-rate hurdle, but the result depends on why yields are rising. Stronger growth and earnings expectations can offset some of the pressure, while tighter real rates or weaker liquidity can make the pressure more significant.

Can falling bond yields be bad for stocks?

Yes. Falling yields can help valuation math, but they can also reflect weaker growth expectations, risk aversion, or falling earnings expectations. In that case, lower yields may not be enough to support equities.

Are bond yields a stock-market signal?

No. Bond yields are an input for market interpretation, not a standalone stock-market signal. They should be read with earnings expectations, credit spreads, liquidity, valuation starting point, and risk appetite.