Regime Foundations separates the core regime concepts used to interpret broad market environments. A market regime focuses on observable market behavior and risk appetite, a macro regime focuses on growth, inflation, liquidity and policy context, and an inflation regime focuses on inflation behavior itself. These lenses organize evidence; they do not create forecasts or trading instructions.

Start with the concept that matches the evidence question, then use classification or asset-behavior frameworks only when the basic regime lens is already clear.

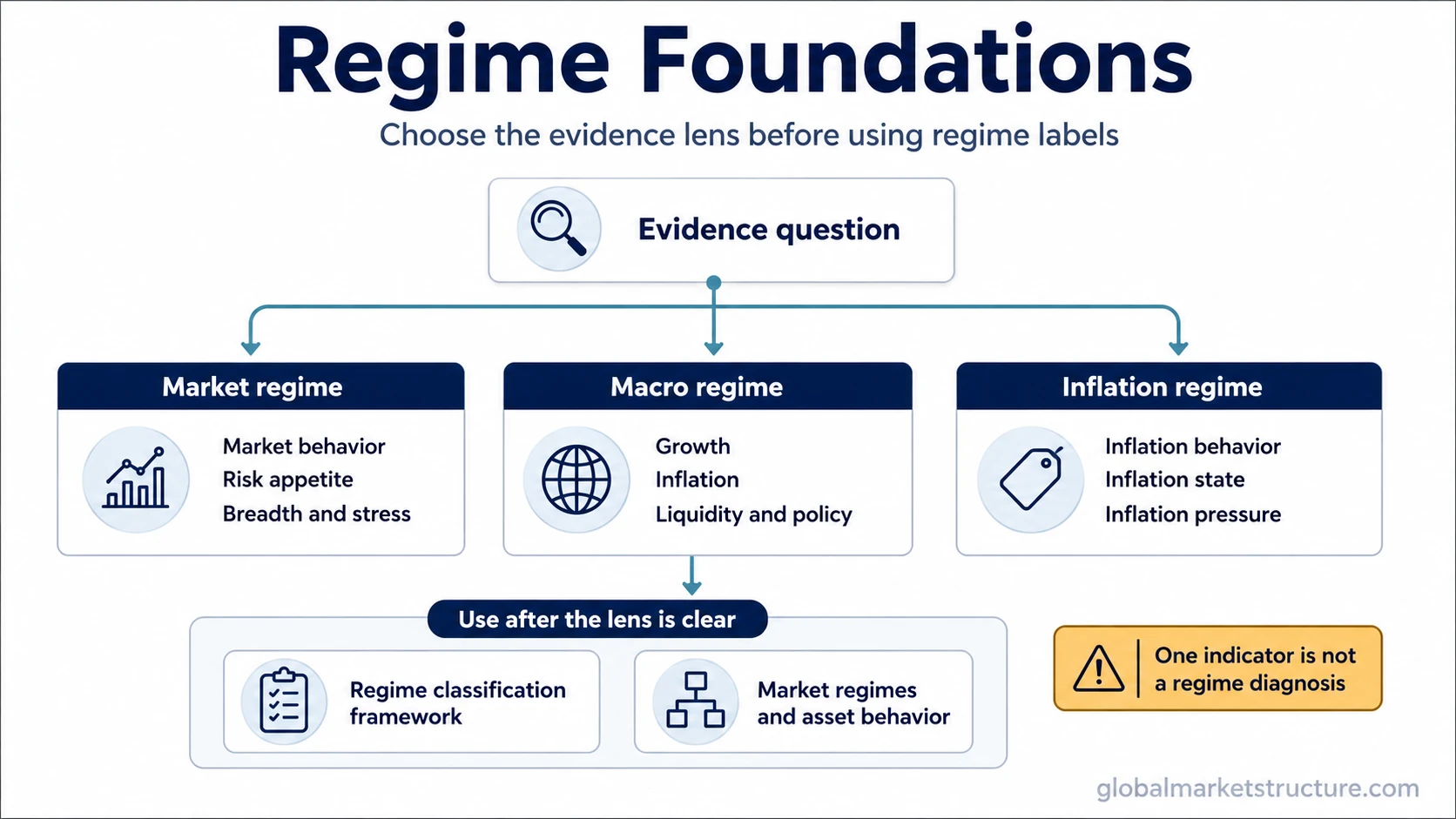

Start with the right regime lens

The fastest way to avoid confusion is to separate the evidence question first. Some questions are about how markets are behaving, some are about the macro backdrop, and some are specifically about inflation behavior.

| Starting question | Best concept to start with | What that concept clarifies | Next analytical question |

|---|---|---|---|

| Is the question about observable market behavior, risk appetite, breadth, stress, or risk-on / risk-off conditions? | Market regime | The market-side evidence that helps describe the current risk environment. | Ask whether several market evidence categories point toward the same classification. |

| Is the question about growth, inflation, liquidity, policy pressure, or the broader economic backdrop? | Macro regime | The broader backdrop that shapes how market evidence may be interpreted. | Ask how the macro backdrop connects with observable market behavior. |

| Is the question specifically about inflation behavior, inflation state, or how inflation changes regime interpretation? | Inflation regime | The inflation-specific lens inside the broader regime picture. | Ask how inflation compares with growth, liquidity, policy, or asset behavior. |

Use frameworks after the core lens is clear

Classification and asset-behavior frameworks work best after the market, macro, or inflation question has been separated.

Use the regime classification framework when the question is how multiple evidence categories fit together. Use market regimes and asset behavior when the question is how broad asset behavior can differ across regime states.

A regime label needs more than one signal

One indicator is not enough to diagnose a regime. Volatility alone does not prove a crisis environment, and a single risk-on or risk-off move does not explain the whole backdrop. Risk appetite, stress evidence, credit confirmation, liquidity and policy context, growth conditions, and inflation behavior can point in different directions.

A common mistake is starting with the label instead of the evidence. If volatility is rising, the first question is not whether a crisis label applies. The better starting point is whether market behavior, credit conditions, liquidity pressure, and macro context are confirming the same interpretation.

Where related regime ideas fit

Growth conditions and policy conditions usually sit within macro-regime interpretation because they describe the broader backdrop. Regime persistence and transition risk need a sequence of market, macro, or classification evidence rather than a standalone shortcut.

Market-regime indicators work best as inputs inside classification logic. A list of indicators is less useful than a framework that separates what each signal is measuring, what can weaken it, and what additional evidence would be needed before a regime label becomes more defensible.

Use the concept that answers the question

Start with market regime when the question is about observable risk behavior. Start with macro regime when the question is about growth, inflation, liquidity, and policy backdrop. Start with inflation regime when the question is specifically about inflation behavior. Use classification and asset-behavior frameworks once the basic lens is clear.