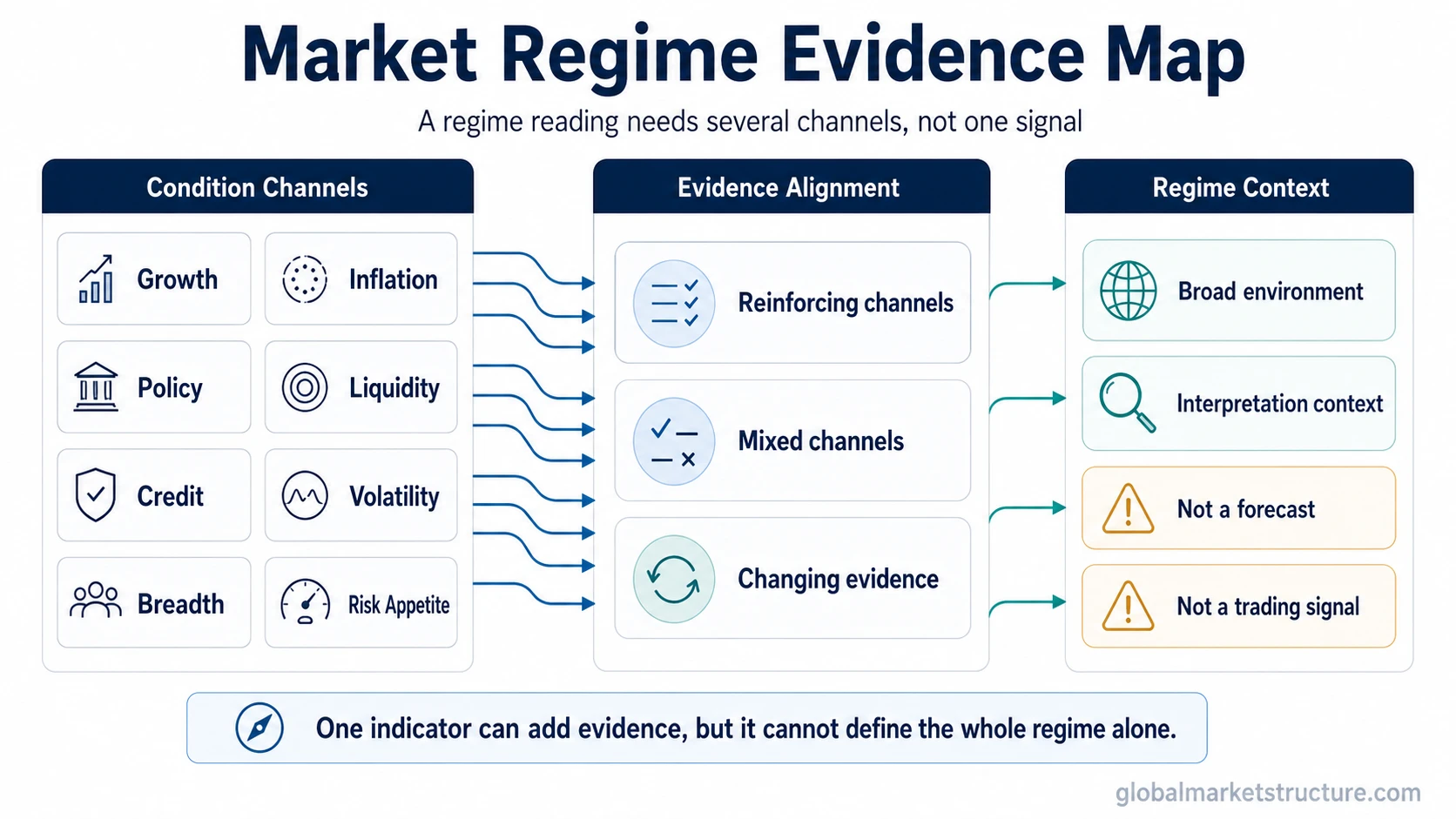

A market regime is a persistent market environment shaped by the dominant mix of growth, inflation, policy, liquidity, credit, volatility, breadth, and risk appetite. It helps interpret broad market behavior by showing which conditions are reinforcing each other. A regime label is not a forecast, a buy/sell signal, or a conclusion that can be created from one indicator alone.

Market regime: a durable condition set that describes how major market forces are interacting across time. The useful question is not whether one signal looks bullish or bearish, but whether several market channels point toward the same environment.

- A market regime describes a persistent environment, not a single signal.

- Regime readings become stronger when several channels confirm the same condition set.

- A regime label gives context for interpretation, not a mechanical trading instruction.

Market Regime Dimensions

Market regimes become more useful when the evidence is separated into dimensions. Each dimension can add context, but each can also mislead when treated as the whole regime.

| Dimension | Observable evidence | Limitation if used alone |

|---|---|---|

| Growth | Economic activity, earnings expectations, production, employment, and demand-sensitive data. | Growth data can lag or conflict with market pricing before the regime is clear. |

| Inflation | Price pressure, wage pressure, commodity sensitivity, breakeven inflation, and inflation expectations. | Inflation pressure does not define the whole environment without growth, policy, and liquidity context. |

| Policy stance | Rate policy, balance-sheet direction, fiscal impulse, and the market’s expectation of policy reaction. | Policy can support or restrain risk, but its effect depends on starting valuations, liquidity, and credit conditions. |

| Liquidity and financial conditions | Funding availability, financial conditions, market depth, collateral pressure, and broad liquidity conditions. | Liquidity can look supportive in one channel while stress appears in another. |

| Credit stress | Credit spreads, default risk, refinancing conditions, and demand for risk compensation. | Credit stress can be early, late, or sector-specific, so it needs confirmation from other risk channels. |

| Volatility | Realized volatility, implied volatility, volatility clustering, and volatility across asset classes. | High or low volatility is a condition, not a full regime by itself. |

| Breadth and leadership | Participation across sectors, factors, regions, and asset classes. | Narrow leadership can persist, so breadth needs to be read with liquidity, credit, and risk appetite. |

| Risk appetite | Demand for cyclical exposure, credit risk, duration, defensive assets, safe havens, and liquidity protection. | Risk appetite can shift quickly when policy, yields, credit, or liquidity change. |

How Market Regimes Become Observable

A market regime becomes more credible when several channels persist in the same direction. Slowing growth, tighter liquidity, wider credit spreads, higher volatility, weaker breadth, and defensive leadership together create a stronger risk-environment reading than any one of those signals alone.

Divergence weakens the label. For example, volatility may rise while credit spreads stay contained and breadth remains healthy. That can indicate temporary turbulence rather than a broader regime shift. The interpretation changes as the evidence set changes.

Confirmation matters: a regime reading is strongest when market behavior, macro conditions, policy expectations, credit, liquidity, and participation reinforce the same environment over time.

What a Market Regime Is Not

A market regime is not volatility alone. Volatility can describe market turbulence, but it does not explain growth, inflation, liquidity, credit, policy, or breadth.

A market regime is not a trend or range label. A trending index can exist inside very different environments, including liquidity expansion, inflation pressure, defensive positioning, or narrow leadership.

A market regime is not the same as risk-on/risk-off. Risk appetite is one important lens, but the full regime also includes macro, policy, credit, liquidity, and market-structure evidence.

A market regime is not a mechanical indicator filter. Indicators and models can help classify conditions, but their output is not the regime itself.

A market regime is not a current market call. Without dated evidence and current data, a regime label should stay conceptual rather than becoming a live forecast.

Market Regime vs Related Concepts

A macro regime focuses more directly on the broader economic environment, including growth, inflation, policy, and cycle conditions.

An inflation regime is narrower because it centers on price pressure and how that pressure interacts with policy, yields, margins, and demand.

A regime classification framework deals with the process for organizing evidence, while market regime names the condition set being interpreted.

Market regimes and asset behavior belongs to the consequence layer: how different assets, sectors, or risk factors may behave when the broader environment changes.

A Simple Market Regime Scenario

A common scenario is that growth momentum softens, credit spreads begin widening, liquidity becomes tighter, volatility rises, and market leadership narrows. That combination can make the risk environment look more defensive because several channels are pointing in the same direction.

The label remains provisional. If policy expectations ease, liquidity improves, breadth recovers, and credit stress fades, the earlier interpretation weakens. The regime reading changes because the evidence changed.

Why Market Regime Labels Can Change

Regime labels are interpretations, not permanent facts. Markets often pass through mixed phases where growth, inflation, policy, credit, liquidity, and breadth do not move together. In those phases, a confident label can create more confusion than clarity.

The useful role of a market regime is context. It helps organize the surrounding conditions so that market behavior is not reduced to one chart, one data point, one headline, or one model output. The label becomes stronger when the evidence is persistent, broad, and internally consistent.

FAQ

What is a market regime in simple terms?

A market regime is the dominant environment shaping broad market behavior. It reflects how conditions such as growth, inflation, policy, liquidity, credit, volatility, breadth, and risk appetite interact over time.

Is a market regime the same as a market trend?

No. A trend describes price direction, while a market regime describes the broader condition set around that trend. The same trend can have different meaning under different liquidity, policy, credit, and breadth conditions.

Can one indicator define a market regime?

No. One indicator can contribute evidence, but a regime label is stronger when several independent channels point toward the same environment.

Is a market regime a forecast?

No. A market regime is an interpretation of conditions. It can help organize context, but it does not predict the next market move or create a buy/sell signal.