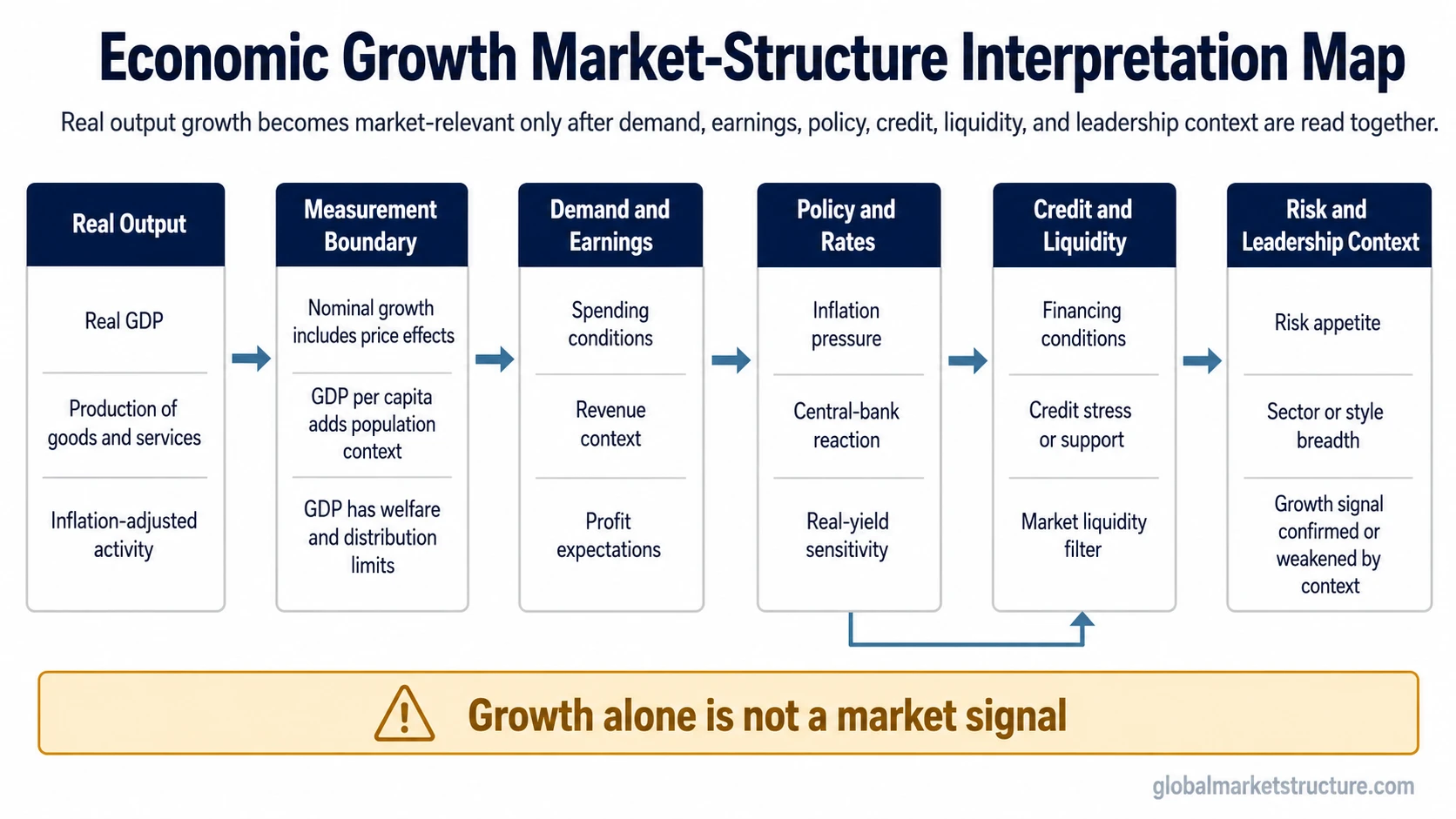

Economic growth is the expansion of an economy’s real output over time. It is commonly discussed through GDP or real GDP, but its market-structure value is contextual: growth helps frame cycle conditions, earnings pressure, policy sensitivity, liquidity conditions, risk appetite, and leadership trends.

Growth data is not a market forecast by itself. The same growth rate can carry different meaning when inflation, interest rates, credit conditions, liquidity, valuations, or earnings expectations change around it.

Definition: Economic growth means an increase in inflation-adjusted economic output over time. Real GDP is the most common measurement frame, while nominal GDP can rise because of both real output gains and higher prices.

- Economic growth is a macro growth-and-activity concept, not a buy or sell signal.

- GDP and real GDP are common measurement frames, but they do not capture every welfare, distribution, or living-standard question.

- Real growth is usually more useful than nominal growth when the goal is to separate output expansion from price-level effects.

- For market interpretation, growth must be read together with inflation, policy, rates, credit, liquidity, earnings, and valuations.

What Is Economic Growth?

Economic growth describes an economy producing more goods and services over time. In macro analysis, the cleanest version is real growth because it adjusts for inflation and focuses more directly on changes in actual output.

Activity sits near the center of the cycle because it affects income, demand, corporate revenue, and earnings expectations. Slower activity can pressure those same channels. The market meaning is conditional because asset prices also respond to inflation, policy reaction, liquidity, valuation, and risk appetite.

A growth expansion is not the same thing as a favorable market environment. If inflation remains high, rates rise, credit tightens, or liquidity deteriorates, positive growth can still coincide with market stress.

How Economic Growth Is Measured

Economic growth is most often measured with gross domestic product. GDP estimates the value of goods and services produced within an economy over a period. Real GDP adjusts that output measure for inflation, which makes it more useful when comparing activity across time.

Nominal GDP measures output at current prices. It can rise because the economy is producing more, because prices are higher, or because both forces are present at the same time. That makes nominal growth useful for revenue, income, and debt-service context, but weaker as a pure output measure.

GDP per capita adds population context by comparing output with the number of people in the economy. It can help frame living-standard questions, but it still does not show how gains are distributed across households, sectors, regions, or income groups.

Current GDP releases belong with official data endpoints. For U.S. data, the Bureau of Economic Analysis is the primary source for current GDP releases. A stable concept explanation should not become a live GDP dashboard because current figures change, revisions matter, and the interpretation depends on surrounding conditions.

Real Growth vs Nominal Growth

Real growth and nominal growth answer different questions. Real growth asks whether the economy is producing more after adjusting for inflation. Nominal growth asks whether the money value of output has increased at current prices.

The difference becomes important when inflation is high. An economy can report strong nominal growth while real growth is weaker because much of the increase comes from higher prices rather than higher output. For market-structure interpretation, that distinction changes how growth connects to margins, policy pressure, real yields, credit demand, and household purchasing power.

Nominal growth: useful for revenue, tax receipts, income totals, and debt ratios, but influenced by price changes.

Real growth: more useful for output momentum because it adjusts for inflation.

Market interpretation: stronger nominal growth can still be stressful if inflation forces tighter policy or compresses real purchasing power.

Economic Growth Components and Market Relevance

The headline number becomes more useful once the underlying components are separated.

| Component | What it shows | Market-structure relevance | Limitation |

|---|---|---|---|

| Real GDP | Inflation-adjusted output growth | Helps frame real activity momentum and cycle conditions | Backward-looking and subject to revision |

| Nominal GDP | Output measured at current prices | Can matter for revenue, income, and debt-service context | Can be lifted by inflation rather than real output gains |

| GDP per capita | Output relative to population | Adds living-standard context to aggregate growth | Does not show distribution by itself |

| Productivity | Output produced per unit of input | Can improve growth quality, margins, and long-run capacity | Often measured with delay and uncertainty |

| Demand conditions | Whether spending and activity are expanding | Connects growth to revenue, earnings, and cycle interpretation | Can overheat or fade depending on policy and credit |

| Earnings context | How activity may affect sales, margins, and profit expectations | Links macro growth to profit-cycle interpretation | Sector exposure, margins, costs, and expectations can dominate |

| Policy sensitivity | How central banks may respond to growth and inflation | Connects growth to rates, real yields, and financial conditions | Policy reaction depends on inflation, labor conditions, and stress |

| Credit and liquidity conditions | Whether financing supports or restricts activity | Separates healthier expansion from strained or fragile growth | Credit and liquidity conditions may shift before headline growth data clearly reflects a turn |

How Economic Growth Enters Market-Structure Interpretation

Economic growth enters market interpretation through several channels rather than through one mechanical signal. Output growth affects demand, demand affects revenue and earnings expectations, and earnings expectations influence how investors price risk across sectors and styles.

Policy is the next filter. Strong growth with contained inflation can support a different environment than strong growth with persistent inflation pressure. If central banks respond with tighter policy, the rate and liquidity effect can offset the positive demand effect.

Credit and liquidity add another layer. Growth supported by healthy credit creation and stable funding conditions is different from growth that depends on expensive financing, fragile balance sheets, or deteriorating market liquidity. In that case, the headline growth number may look stable while the underlying risk environment weakens.

Market leadership also matters. Broad growth that supports many sectors sends a different signal from narrow growth concentrated in a few areas. A growth expansion can look healthier when earnings breadth, credit conditions, and liquidity confirm the macro signal.

Growth Interpretation Chain

- Real output: Is activity expanding after inflation?

- Demand and earnings: Does growth support revenue and profit expectations?

- Policy and rates: Does growth invite easier, neutral, or tighter financial conditions?

- Credit and liquidity: Are financing conditions supporting or restricting activity?

- Risk appetite and leadership: Is market participation broadening or narrowing?

- Limitation: Growth alone does not determine asset direction.

When Economic Growth Can Mislead Market Interpretation

Growth can mislead when it is read in isolation. Strong growth can coincide with market stress if inflation pressure forces tighter policy, if credit spreads widen, if liquidity deteriorates, or if valuations already assume a very strong earnings path.

Weak growth does not automatically mean recession or falling asset prices. Markets may respond differently if inflation is easing, policy expectations are becoming less restrictive, liquidity is improving, or earnings expectations have already adjusted downward.

The common mistake is treating growth as a single-switch signal. Growth is more useful as part of a condition set that includes inflation, rates, credit, liquidity, earnings revisions, market breadth, and valuation context.

Illustrative Growth Scenario

Consider a generic environment where real growth improves while inflation cools, credit spreads stay contained, and financial conditions ease. That mix can support risk appetite because output, earnings expectations, and liquidity conditions are aligned.

The interpretation changes if growth remains strong but inflation pressure rises, rates move higher, credit conditions tighten, and market breadth narrows. In that case, the growth number still shows activity, but the market-structure reading becomes more cautious because the policy, liquidity, and credit filters are working against the headline.

Economic Growth vs Related Growth Signals

Economic growth is the broad concept. Related indicators help narrow the interpretation, but they do not replace the concept.

| Related concept | How it differs | Why it matters |

|---|---|---|

| Output gap | Compares actual output with estimated potential output | Helps frame slack, overheating, and policy pressure |

| Purchasing Managers Index | Survey-based activity signal rather than total output measure | Can offer timelier growth-cycle clues than GDP |

| Soft landing | Describes a slowdown path where inflation cools without severe contraction | Connects growth, inflation, policy, and labor-market resilience |

| Hard landing | Describes a sharper growth deterioration after restrictive conditions | Helps separate mild cooling from more damaging activity stress |

| Growth indicators for markets | Groups multiple signals used to track activity momentum | Helps avoid relying on one backward-looking growth number |

Common Questions About Economic Growth

Is economic growth the same as GDP growth?

GDP growth is the most common way to discuss economic growth, but the concept is broader. GDP measures aggregate output, while economic growth can also be interpreted through real output, productivity, income, per-capita output, and the quality of expansion.

What is the difference between real and nominal economic growth?

Nominal growth measures output at current prices. Real growth adjusts for inflation, which makes it more useful for judging whether actual output is expanding rather than prices simply rising.

Does economic growth predict markets?

Economic growth does not predict markets by itself. Market interpretation changes with inflation, policy reaction, rates, credit conditions, liquidity, earnings expectations, valuations, and market breadth.

Where should current GDP data be checked?

Current GDP data should be checked through official statistical sources. For U.S. GDP releases, the Bureau of Economic Analysis is the primary official source. Current figures need dates and revision context because they change over time.