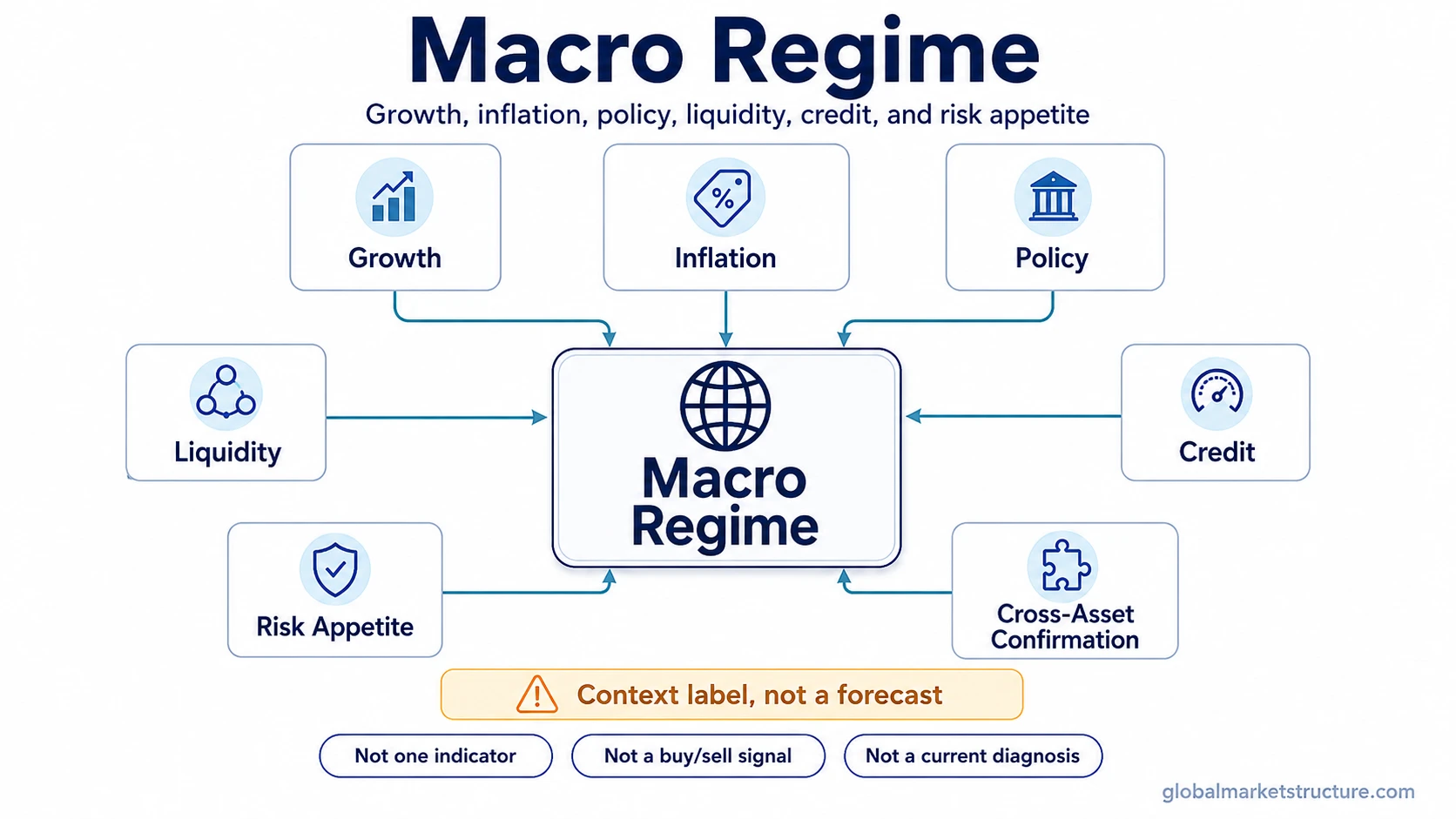

A macro regime is the broad macro environment that shapes how market conditions are interpreted. It is usually read through a stack of conditions such as growth, inflation, policy, liquidity, credit, and risk appetite. A macro regime is not confirmed by one data point, one asset move, or one headline, and it does not predict a specific market outcome by itself.

What a Macro Regime Means

A macro regime describes the background condition layer around markets. It combines economic momentum, inflation pressure, policy stance, liquidity, credit stress, and the willingness of investors to hold risk. The concept is useful because market signals can look different depending on the surrounding macro environment.

The same equity move, rate move, commodity move, or volatility spike can carry different meaning when growth is accelerating than when growth is weakening. A macro regime helps organize that context, but it does not turn context into certainty.

Macro Regime vs Nearby Concepts

A macro regime is broader than a market regime. A market regime focuses more on how markets behave: risk-on or risk-off conditions, volatility behavior, leadership quality, breadth, and cross-asset pricing. A macro regime focuses on the macro condition layer behind that behavior.

An inflation regime is narrower. It focuses on whether inflation pressure is easing, persistent, reaccelerating, or unstable. Inflation can be one major part of a macro regime, but it is not the whole regime by itself.

A regime classification framework is also different. Classification deals with how regimes are grouped, labeled, and monitored. A macro regime is the concept being interpreted; classification is the process used to organize that interpretation.

What Shapes a Macro Regime

A macro-regime reading becomes stronger when several independent channels point in the same direction. It becomes weaker when the case depends on one isolated indicator or when the signals conflict.

Growth, inflation, policy, liquidity, credit, and risk appetite can each affect the reading. None of them is enough alone. A single inflation print, rate move, credit spread change, volatility spike, or equity decline can be noisy, temporary, or driven by positioning rather than a durable change in the macro environment.

| Macro regime input | What it shows | Why it is not enough alone |

|---|---|---|

| Growth direction | Whether activity is strengthening, slowing, contracting, or recovering. | Growth can shift while inflation, policy, credit, or risk appetite point elsewhere. |

| Inflation pressure | Whether price pressure is easing, persistent, or reaccelerating. | Inflation is one dimension inside the regime, not the full macro regime. |

| Policy stance | Whether central-bank or policy conditions are easing, tightening, restrictive, or supportive. | Policy can lag conditions, vary across regions, or be offset by liquidity and credit conditions. |

| Liquidity conditions | Whether financing and market functioning are easier or tighter. | Liquidity can differ across funding markets, asset markets, and policy channels. |

| Credit stress | Whether risk aversion, default concern, or financing pressure is rising. | Credit weakness can be local or sector-specific without defining the whole macro environment. |

| Risk appetite | How markets are pricing uncertainty and willingness to hold risk. | Market pricing can overshoot, lag, or reflect positioning rather than macro reality. |

| Cross-asset confirmation | Whether rates, credit, equities, commodities, currencies, and volatility are telling a consistent story. | Cross-asset behavior can be noisy, transitional, or temporarily distorted by positioning. |

Inflation Is One Dimension, Not the Whole Regime

An inflation regime can strongly affect the macro backdrop, especially when policy pressure, real yields, currency behavior, and credit conditions respond to inflation persistence. Still, inflation alone does not define the full macro regime.

Inflation may be easing while growth slows, or inflation may remain persistent while credit conditions tighten. Those combinations can produce different regime readings even when the inflation label looks similar. The broader macro regime depends on how inflation interacts with growth, policy, liquidity, credit, and risk appetite.

Risk Appetite and Stress Confirmation

Risk appetite is an observable channel, not the macro regime itself. It reflects how markets are pricing uncertainty, liquidity, credit risk, volatility, and the willingness to own risk-sensitive assets. It can support a regime reading, but it can also move ahead of the macro data or reverse quickly when positioning changes.

Stress confirmation becomes more useful when credit spreads, liquidity conditions, rates, volatility context, and risk appetite align. A risk-off move becomes more meaningful when it appears alongside tighter financing, weaker credit behavior, and less supportive policy conditions. A risk-on move becomes more internally consistent when liquidity, credit, and growth expectations also improve.

When the signals conflict, the interpretation should stay provisional. A regime classification framework can organize those inputs, but classification still depends on evidence quality rather than one dominant headline.

What a Macro Regime Is Not

A macro regime is a context label, not a forecast. It does not guarantee equity direction, bond returns, commodity behavior, currency moves, or volatility outcomes.

It is not a buy signal, sell signal, allocation rule, or proof that a specific market outcome must follow. It is also not confirmed by one indicator. A single CPI print, yield move, equity selloff, volatility spike, credit spread move, or policy headline can matter, but it cannot define the macro regime by itself.

A Simple Macro-Regime Scenario

Growth expectations weaken, inflation remains sticky, credit spreads widen, and risk appetite deteriorates. That combination can support a macro-regime reading because several independent channels are moving in the same direction. The label still does not predict a specific asset outcome.

The interpretation weakens when the evidence becomes mixed. For example, credit stress might fade, liquidity might improve, or risk appetite might recover before the macro data fully confirms a durable shift. A stronger reading needs persistence and confirmation across more than one channel.

Related Concepts

Market-regime analysis focuses more directly on market behavior, volatility conditions, breadth, leadership, and risk-on or risk-off pricing. Macro-regime analysis focuses on the broader condition layer that can influence those market behaviors.

Inflation-regime analysis isolates the behavior of inflation pressure. Macro-regime analysis includes inflation, but also adds growth, policy, liquidity, credit, and risk appetite.

Classification work belongs to the process layer. It deals with how evidence is grouped and labeled when the macro backdrop is changing or mixed.

Asset-behavior questions belong to a separate interpretation layer. Different market environments can affect risk assets, defensive assets, rates, commodities, and currencies in different ways, but how market regimes affect asset behavior requires a separate evidence framework from the definition of macro regime.

FAQ

Can one indicator confirm a macro regime?

No. One indicator can support a reading, but a macro regime depends on a broader condition stack. Growth, inflation, policy, liquidity, credit, risk appetite, and cross-asset behavior need to be interpreted together.

Is a macro regime the same as a market regime?

No. A macro regime focuses on the broad macro condition layer. A market regime focuses more on market behavior, risk appetite, volatility, leadership, and cross-asset pricing.

Does a macro regime predict asset returns?

No. A macro regime can provide context for interpretation, but it does not predict a specific asset return or guarantee a market direction.