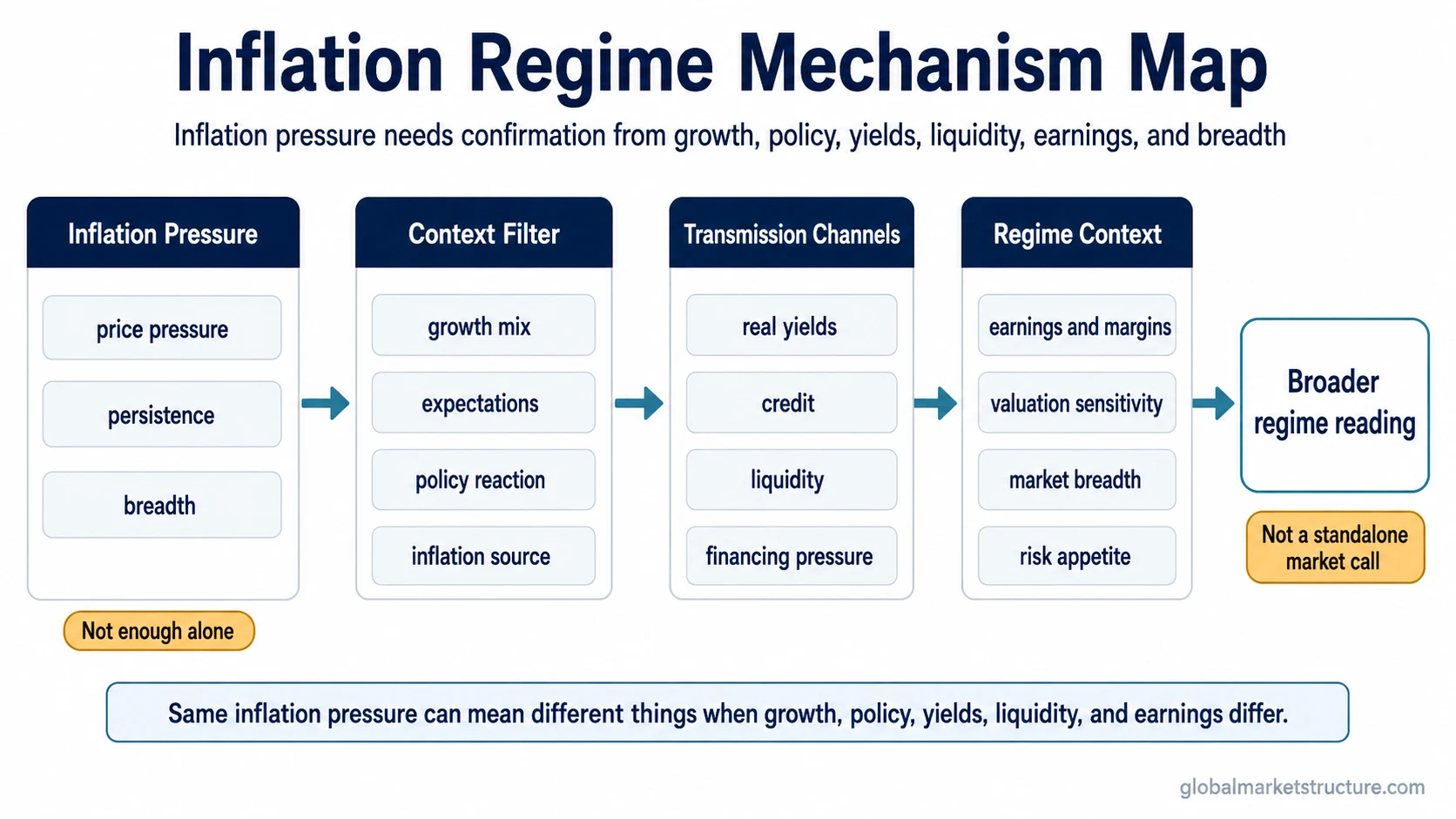

An inflation regime describes how inflation pressure behaves and how that pressure changes broader market interpretation. It is not the same as the latest inflation rate, and it is not a complete market regime by itself. The reading becomes more useful when inflation persistence, growth, policy reaction, real yields, liquidity, credit, earnings pressure, and market breadth point in a coherent direction. It is not a forecast or standalone asset signal.

Key Points

- An inflation regime describes the behavior of inflation pressure, not only one inflation print.

- Inflation pressure becomes regime-relevant when it is persistent, broad, and tied to expectations, policy reaction, yields, liquidity, credit, and earnings conditions.

- Inflation regime is one layer of market interpretation, not the whole macro or market environment.

- Asset behavior remains conditional because growth, policy, real yields, liquidity, valuation, and earnings pressure can change the outcome.

What an inflation regime is

An inflation regime is a classification of inflation behavior inside a broader market environment. It looks at whether inflation pressure is isolated or persistent, narrow or broad, anchored or unstable, and whether policy reaction is easing, restrictive, credible, or constrained.

Definition: An inflation regime is the inflation-pressure layer of regime analysis, shaped by persistence, breadth, expectations, policy reaction, real yields, liquidity, credit, earnings pressure, and market breadth.

The useful distinction is that inflation does not become a regime reading just because a headline number rises. A single inflation print is a measurement. A regime reading asks whether inflation pressure is durable enough to influence policy, financing conditions, earnings assumptions, valuation sensitivity, and cross-asset behavior.

What an inflation regime is not

Several nearby terms can look similar, but they answer different questions. Keeping the boundaries clean prevents inflation pressure from being treated as a one-factor explanation for the entire market environment.

| Concept | What it means | How it differs from inflation regime |

|---|---|---|

| Inflation rate | A measured change in prices over a specific period. | An inflation regime looks at persistence, breadth, and transmission, not only the latest number. |

| Inflation expectations | Forward-looking beliefs or market-implied views about future inflation. | Expectations can influence the regime reading, but they are not the full regime by themselves. |

| Monetary regime | The policy framework, target system, or reaction function used by a central bank. | Monetary regime describes the policy setup; inflation regime describes the behavior of inflation pressure inside the environment. |

| Macro-regime | The broader mix of growth, inflation, policy, liquidity, and cycle conditions. | Inflation regime is one dimension inside the wider macro mix. |

| Market-regime | The broader risk environment across assets, volatility, leadership, liquidity, and positioning. | Inflation regime can influence the market reading, but it does not classify the whole market environment alone. |

| Stagflation | Inflation pressure combined with weak growth or growth stress. | High inflation alone is not stagflation unless the growth side also deteriorates. |

| Reflation | Inflation pressure or price recovery alongside improving growth conditions. | The same inflation pressure can mean something different when growth is improving rather than weakening. |

| Asset-allocation regime | A portfolio interpretation layer built around expected asset behavior. | Inflation regime does not automatically decide which assets should outperform. |

How inflation pressure becomes regime-relevant

Inflation pressure becomes more useful for market interpretation when several channels line up. The strongest reading usually comes from the combination, not from any single indicator.

| Channel | What to check | Why it changes the reading |

|---|---|---|

| Persistence | Whether inflation pressure keeps appearing across multiple periods. | Persistent pressure is more likely to affect policy, expectations, contracts, and valuation assumptions. |

| Breadth | Whether price pressure is narrow or spread across several categories. | Broad pressure can be harder to dismiss as a temporary shock. |

| Growth mix | Whether real activity is accelerating, steady, slowing, or contracting. | The same inflation pressure can look different in reflation, overheating, slowdown, or stagflation-like conditions. |

| Policy reaction | Whether policy is becoming easier, tighter, constrained, or credibility-focused. | Policy response shapes discount rates, liquidity, financing pressure, and risk appetite. |

| Inflation expectations | Whether expectations remain anchored or become more sensitive to recent price pressure. | Expectations can affect wages, pricing behavior, and the credibility burden on policymakers. |

| Real yields | Whether nominal yields are rising faster or slower than inflation expectations. | Real yields can change valuation pressure, duration sensitivity, and financial conditions. |

| Credit and liquidity | Whether financing conditions are loose, stable, tightening, or stressed. | Inflation becomes more restrictive when it appears alongside tighter credit or weaker liquidity. |

| Earnings and margins | Whether companies can pass through costs or margins are being squeezed. | Inflation can be easier for risk assets when revenue growth and pricing power absorb cost pressure. |

| Market breadth | Whether leadership is broad, narrow, defensive, cyclical, or unstable. | Breadth helps separate a broad risk appetite regime from a fragile market carried by a small group of assets. |

Why inflation alone is not enough

Inflation pressure does not classify the full market environment by itself. A high inflation reading can appear during strong nominal growth, late-cycle overheating, supply stress, policy tightening, or growth deterioration. Each setting can produce a different market interpretation.

Core limitation: inflation regime is not a market call. It does not prove risk-on behavior, risk-off behavior, stagflation, reflation, or fixed asset winners. The broader reading depends on inflation source, growth, policy reaction, real yields, liquidity, credit, earnings, valuation, and breadth.

The most common mistake is treating inflation as a single switch. Inflation can support nominal revenue in some environments, compress valuation multiples in others, pressure margins when costs rise faster than pricing power, or tighten financial conditions when central banks respond aggressively.

A practical inflation-regime scenario

A generic inflation-regime scenario can begin with persistent price pressure and a central bank that remains restrictive because expectations are at risk. If real yields rise, credit conditions tighten, liquidity weakens, and margins come under pressure, inflation becomes part of a more restrictive market backdrop. That still does not classify the full market regime unless growth, breadth, credit, and risk appetite confirm the same message.

A different scenario can have similar inflation pressure but stronger growth, wider earnings participation, healthier credit, and more stable liquidity. In that setting, the inflation component may still matter, but the broader interpretation is not the same. The growth side changes the meaning of inflation pressure.

Common misuses of inflation regime

- Calling every high-inflation period stagflation: stagflation requires weak growth or growth stress alongside inflation pressure.

- Using inflation as an asset-winner list: commodities, gold, real assets, equities, bonds, and cash can behave differently depending on policy, real yields, liquidity, valuation, and growth.

- Ignoring policy credibility: the same inflation pressure can produce different market behavior when policymakers are credible, constrained, behind the curve, or aggressively tightening.

- Using universal thresholds: inflation-regime definitions can vary by country, period, model, and research method.

- Making current-country claims without dated evidence: a live inflation-regime classification needs current data, a stated method, and source verification.

Related regime concepts

A macro-regime includes the full growth, inflation, policy, liquidity, and cycle mix. Inflation regime is one input inside that wider macro structure.

A market-regime describes the broader risk environment across assets, volatility, liquidity, leadership, and positioning. Inflation pressure can influence that environment, but it does not define it alone.

Stagflation and reflation are useful neighboring ideas because they show why the growth side matters. Inflation pressure with weakening growth carries a different implication from inflation pressure with improving growth and broader earnings participation.