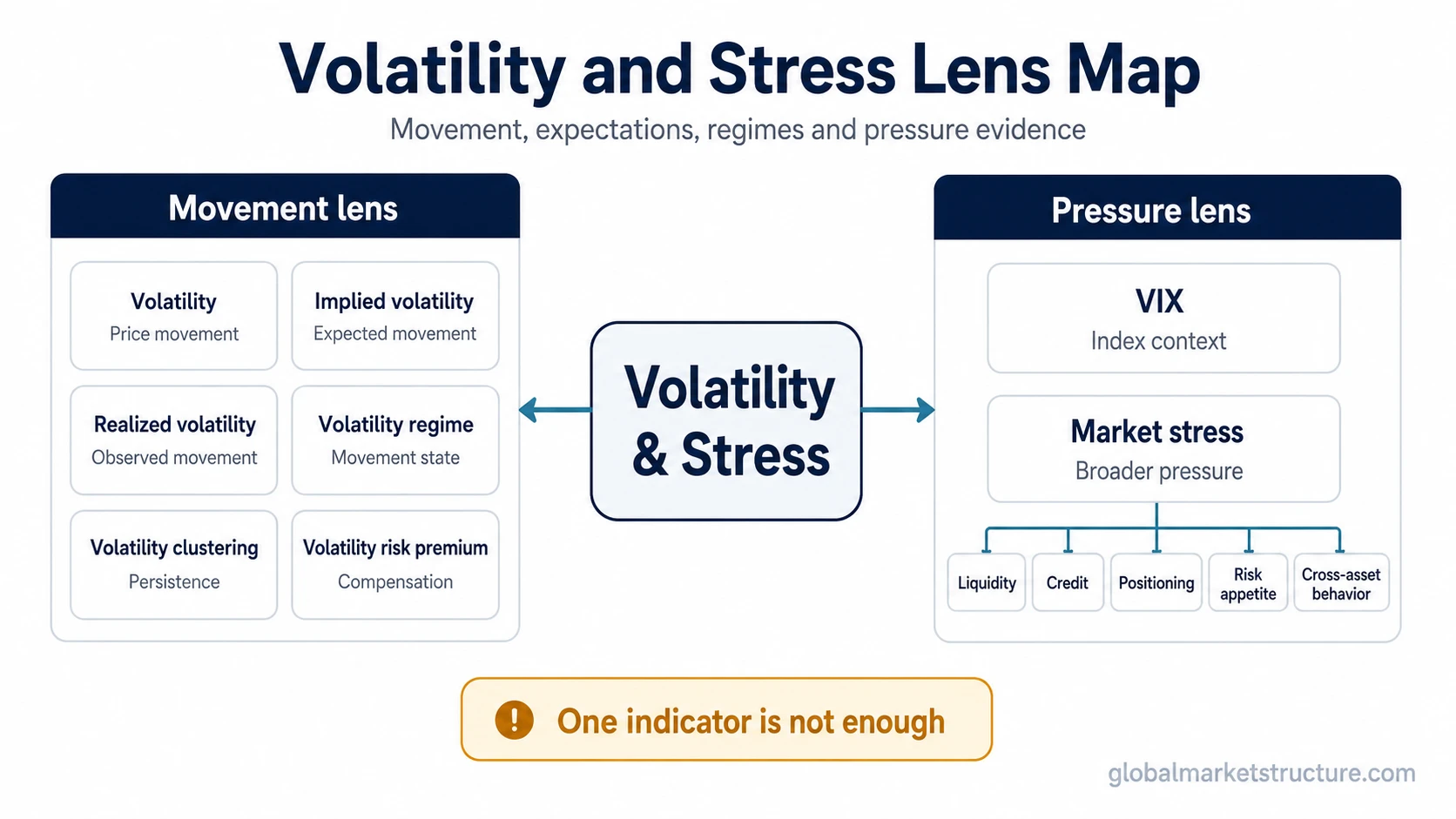

Volatility and stress describe different parts of market-risk behavior. Volatility tracks how much prices move, while stress asks whether those moves reflect pressure in liquidity, credit, positioning or risk appetite. A volatility spike can be noise, repricing or an early warning. The reading becomes stronger only when it aligns with broader confirmation, not one isolated indicator.

Core distinction: volatility is movement, stress is pressure, and broader evidence separates ordinary repricing from wider risk-environment strain.

Key Points

- Volatility measures movement; stress requires broader market pressure.

- Implied volatility, realized volatility, VIX and volatility regimes answer different market questions.

- Market stress becomes more credible when volatility aligns with liquidity, credit, positioning or risk-appetite pressure.

- One isolated volatility signal should not diagnose the whole risk environment.

How volatility and stress differ

Volatility is the scale and pattern of price movement. It can rise because markets are repricing new information, reacting to event risk, adjusting option expectations or moving through a different volatility state.

Stress is broader than movement alone. It asks whether price movement is connected to pressure in liquidity, credit, positioning, breadth, cross-asset behavior or risk appetite. The same volatility move can carry different meaning depending on whether other pressure signals confirm it.

That distinction keeps the major concepts separate: movement, expected movement, observed movement, volatility state, persistence, compensation for volatility risk, index-based volatility tracking and broader market stress.

Choose the right volatility or stress concept

Different volatility terms answer different market questions. The useful starting point is the question being asked, not the broad label.

| Market question | Concept to use | What it focuses on |

|---|---|---|

| How much are markets moving? | volatility | The size and pattern of price movement across markets. |

| What movement is priced into options? | implied volatility | Market-priced expectations for future movement. |

| What movement already happened? | realized volatility | Observed price movement over a past measurement window. |

| What volatility state is the market in? | volatility regime | The broader volatility environment rather than one single move. |

| Why does volatility persist after shocks? | volatility clustering | The tendency for high-volatility periods to group together. |

| How is volatility risk compensated? | volatility risk premium | The compensation linked to bearing volatility exposure. |

| Is pressure broader than movement alone? | market stress | Pressure across volatility, liquidity, credit, positioning and risk appetite. |

| What does the common volatility index represent? | VIX | A widely watched index-based view of equity-index volatility expectations. |

When volatility becomes a stress signal

A volatility spike can reflect temporary event risk, repricing, uncertainty or changing option demand. It becomes more useful as a stress signal when other parts of the market confirm that pressure is spreading beyond price movement.

Limitation: high volatility alone does not prove market stress. The interpretation is stronger when volatility aligns with weaker risk appetite, tighter liquidity, wider credit pressure, fragile positioning or confirming cross-asset behavior.

| Pressure lens | Why it changes interpretation |

|---|---|

| Risk appetite | Price movement carries more stress meaning when markets stop rewarding risk exposure. |

| Liquidity pressure | Stress is more structural when participants cannot transact or finance positions smoothly. |

| Credit pressure | Credit deterioration can show that risk compensation is changing beyond equity volatility alone. |

| Positioning pressure | Crowded exposure can turn movement into forced adjustment when liquidity or risk tolerance weakens. |

| Cross-asset behavior | Stress readings become stronger when several markets point toward the same pressure pattern. |

Related volatility paths

Some questions need a narrower comparison or mechanism before the broader stress label is useful.

- implied vs realized volatility separates expected movement from observed movement.

- volatility spikes focus on what a sudden jump may or may not mean.

- volatility and liquidity connects price movement with market depth and trading conditions.

Use the narrow concept that matches the question: movement, expectation, observed movement, regime state, persistence, compensation, broad pressure or VIX context. Market stress should remain a context problem, not a single-number label.