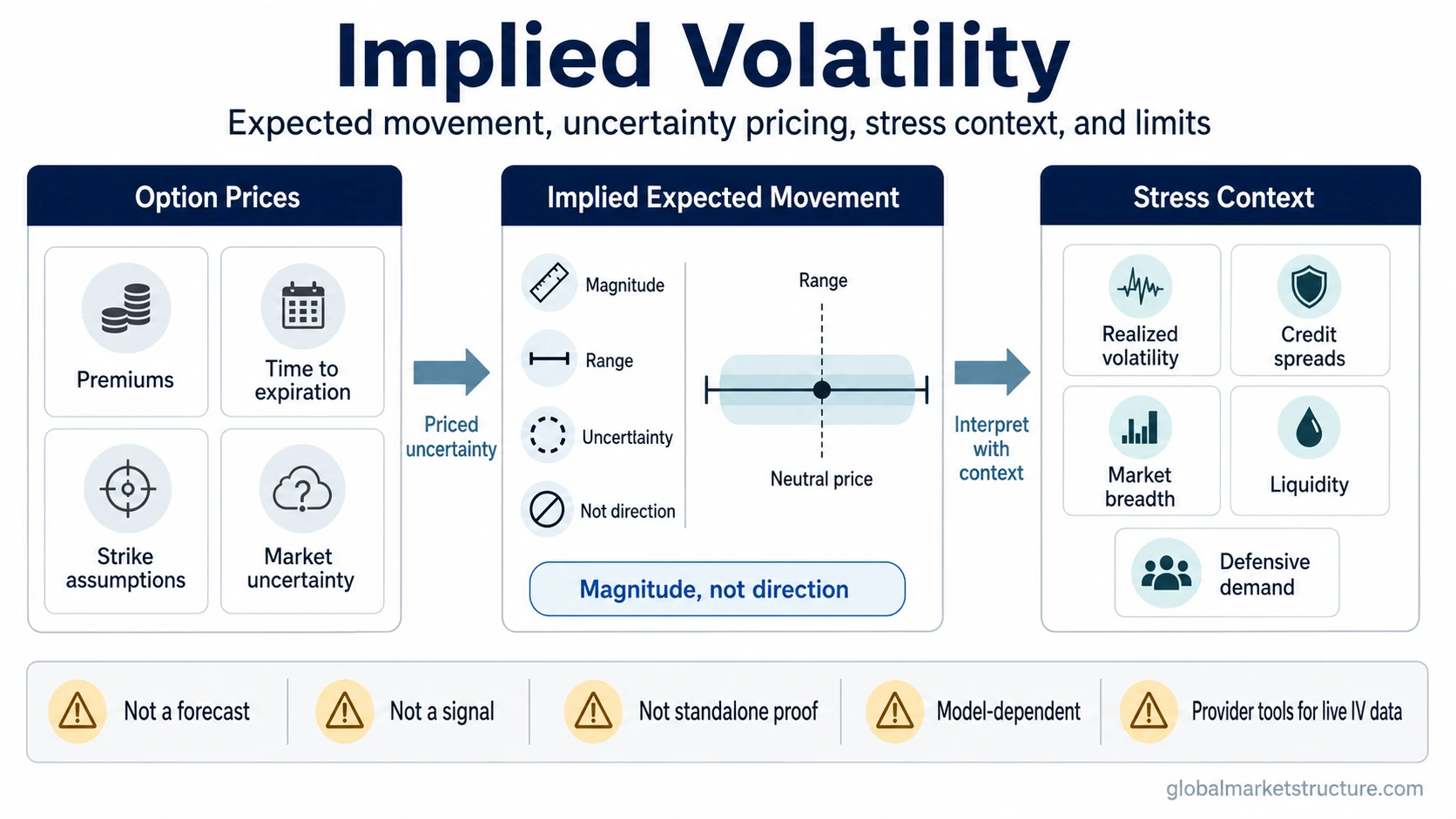

Implied volatility is the expected volatility, or movement range, implied by option prices. It reflects the magnitude of movement the options market is pricing, not the direction of that movement. In market-structure analysis, implied volatility can help interpret uncertainty, protection demand, and stress pricing, but it is not a forecast, a trading signal, or standalone proof of market stress.

Definition: Implied volatility is an options-derived estimate of expected future volatility. It is backed out from option prices rather than measured directly from past price movement.

That distinction matters because implied volatility belongs to the forward-looking side of volatility analysis. It shows how much uncertainty is being priced into options, but it does not reveal whether the underlying market is expected to rise or fall.

How Implied Volatility Works

Option prices contain assumptions about possible future movement. When an option price rises or falls, part of that change can reflect shifts in expected volatility, not only changes in the underlying asset price.

An option-pricing model can translate an observed option price into an implied volatility estimate, using assumptions such as the underlying price, strike, time to expiration, interest rates, and other model inputs. The result is not a separately observed market fact. It is the volatility estimate that makes the option price consistent with the model and its inputs.

The useful point is conceptual rather than mathematical: implied volatility tends to rise when the options market prices a wider range of possible outcomes and tends to fall when that priced range narrows. Option demand, event risk, time to expiration, liquidity, skew, and protection demand can all affect how an IV reading should be interpreted.

What Implied Volatility Shows and Does Not Show

Implied volatility is often misread because it sounds like a directional forecast. It is better treated as a measure of priced uncertainty.

| What implied volatility can show | What implied volatility does not show |

|---|---|

| Expected movement magnitude priced into options | The exact direction of the next market move |

| Option-market uncertainty or demand for protection | A guaranteed realized outcome |

| Event risk, wider outcome ranges, or stress pricing | Standalone proof that a market is already in stress |

| Pressure on option premiums when uncertainty is high | A recommendation to buy or sell options |

| A forward-looking market-implied volatility input | The same thing as measured historical movement |

Why Implied Volatility Matters in Stress Analysis

Implied volatility can become useful when market participants begin pricing a wider distribution of possible outcomes. That can happen before major scheduled events, during uncertainty around policy or earnings, or when investors are willing to pay more for protection against adverse moves.

The key limitation is that implied volatility does not identify the reason by itself. A rise can reflect genuine stress, event uncertainty, dealer positioning, lower liquidity, skew in demand for protection, or a temporary repricing of option premiums.

In broader risk-environment analysis, implied volatility becomes more useful when it aligns with other evidence. The reading is stronger when rising implied volatility appears alongside widening credit spreads, weaker market breadth, deteriorating liquidity, rising realized volatility, or greater demand for defensive assets. It is weaker when implied volatility rises in isolation while broader market evidence remains calm or mixed.

Implied Volatility vs Realized Volatility

Implied volatility and realized volatility answer different questions. Implied volatility reflects what the options market is pricing for future movement. Realized volatility describes movement that has already occurred over a measured period.

The difference between the two can reveal a useful tension. Implied volatility may rise before realized volatility moves if the options market begins pricing uncertainty ahead of an event. Realized volatility may rise after large price moves have already happened, even if implied volatility later falls as uncertainty is resolved.

For a full distinction between forward-looking option-implied pricing and measured historical movement, see implied vs realized volatility.

Common Mistakes When Reading Implied Volatility

Mistake 1: Treating high implied volatility as automatically bearish. High IV can mean uncertainty is elevated, but it does not specify whether the next large move is up or down.

Mistake 2: Treating low implied volatility as safety. Low IV can reflect calm conditions, but it can also reflect complacency, suppressed realized movement, or limited demand for protection before conditions change.

Mistake 3: Treating implied volatility as a trading signal. IV can affect option pricing and risk interpretation, but it does not create a complete decision framework by itself.

Mistake 4: Treating IV as standalone proof of market stress. Stress interpretation requires confirmation from broader market evidence, not only one volatility input.

Practical Scenario

A known event approaches, and market participants begin paying more for options because the range of possible outcomes feels wider. Implied volatility rises as those option prices embed more uncertainty.

That rise does not say whether the market will move higher or lower. It also does not guarantee that stress will persist after the event. If the event passes and uncertainty falls, implied volatility can decline even if the underlying asset still moves.

The more useful question is whether the higher implied volatility is isolated or confirmed elsewhere. If credit spreads are stable, liquidity is normal, and market breadth is not weakening, the rise may be mostly event-related. If those broader inputs deteriorate at the same time, implied volatility becomes part of a stronger stress-context picture.

Limits of Implied Volatility

Implied volatility is one input, not a conclusion. It can help interpret uncertainty, but it should not be used as a standalone market regime label.

High IV can be misread. It may reflect protection demand, event risk, skew, liquidity conditions, or expensive option pricing. It does not automatically mean the underlying market is bearish.

Low IV can also be misread. It may reflect calm, but it can also reflect low recent movement or limited demand for protection before uncertainty returns.

Live data belongs to provider tools. Current IV rankings, option chains, screeners, and contract-level analytics require direct market-data tools rather than a static concept page.

Related Concepts

Use implied volatility as the forward-looking uncertainty-pricing concept inside volatility and stress analysis.

Use realized volatility when the question is about measured historical movement.

Use the implied-versus-realized comparison when the question is about the gap between what the options market prices and what the market later delivers.