Volatility risk premium is the compensation associated with bearing volatility risk, commonly inferred from the gap between option-implied volatility and realized or expected realized volatility. It can reflect protection demand, risk appetite, and option-market pricing pressure, but it is not a standalone market forecast, trading signal, guaranteed edge, or complete market-stress reading.

Core distinction: implied volatility comes from option prices, realized volatility comes from observed price movement, and volatility risk premium describes the difference investors may demand or pay around that uncertainty.

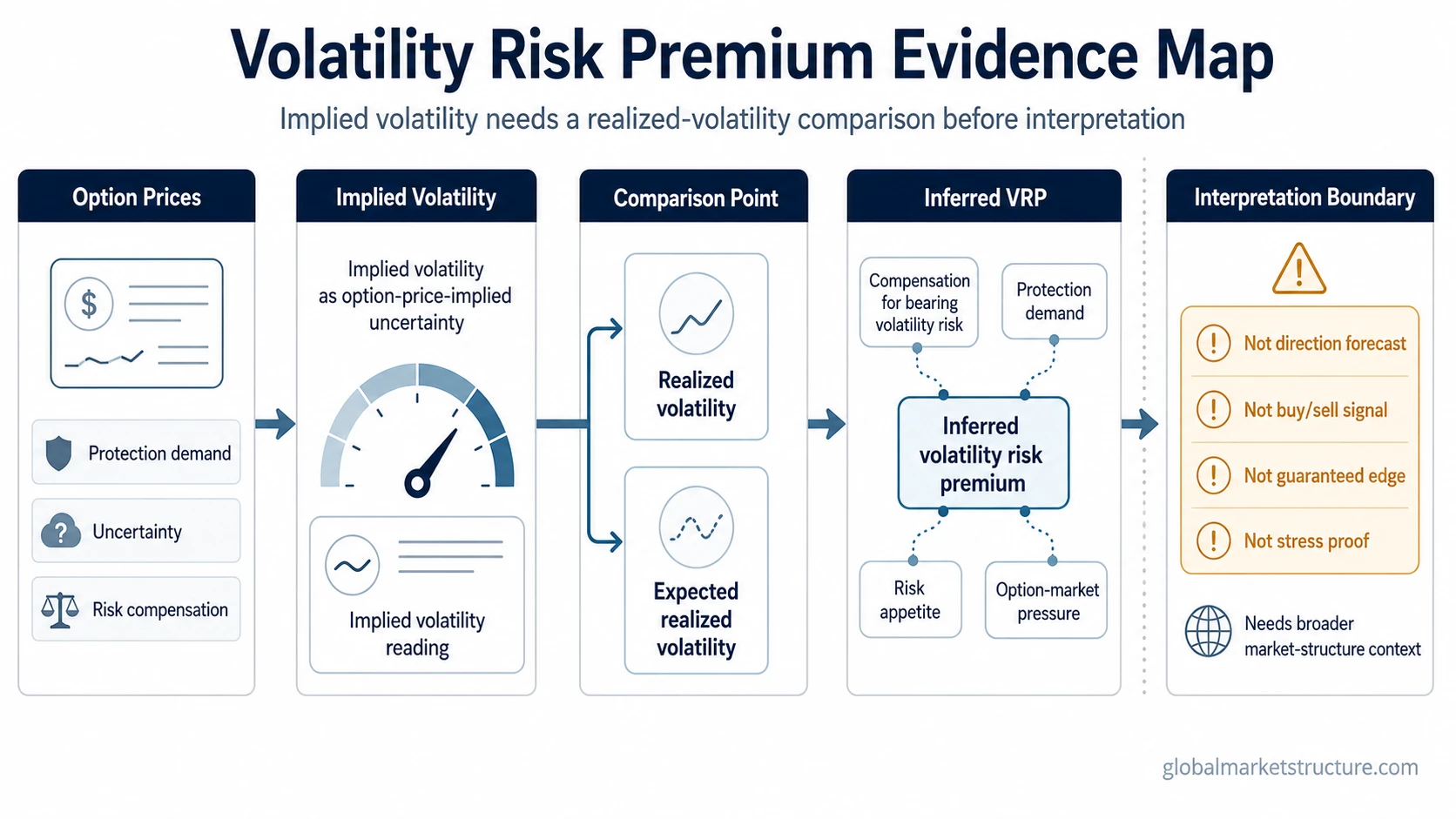

What Volatility Risk Premium Means

Volatility risk premium, often shortened to VRP, refers to the compensation associated with taking the other side of volatility uncertainty. In common market usage, it is discussed when option-implied volatility is higher or lower than realized volatility, or than the realized volatility market participants expect over the same horizon.

The concept is not directly observed like a spot price. It is inferred from a comparison. Option prices embed a market-implied view of future uncertainty, while realized volatility records how much the asset actually moved over a completed period. The gap between those ideas can be interpreted as a premium for bearing volatility risk.

That interpretation stays conditional. A positive premium can reflect protection demand, uncertainty, positioning pressure, liquidity conditions, or compensation for absorbing risk. It should not be reduced to a simple statement that options are always expensive or that selling volatility is automatically rewarded.

How the Premium Is Commonly Inferred

The usual mechanism starts with option prices. When option buyers are willing to pay more for protection or convex exposure, option prices can imply higher expected volatility. That implied reading is then compared with realized volatility or with an estimate of expected realized volatility.

- Option prices reflect demand, supply, uncertainty, and risk compensation.

- Implied volatility translates those option prices into a volatility estimate.

- Realized or expected realized volatility provides the comparison point.

- The inferred premium is the gap between what volatility is priced to be and what it realizes or is expected to realize.

- The interpretation may involve protection demand, risk appetite, volatility uncertainty, or option-market pressure.

- The limitation is that the gap alone does not prove direction, stress, or a repeatable trading edge.

A large gap may mean investors are paying heavily for protection, but it may also reflect genuine uncertainty about future movement. A small or negative gap may suggest less compensation for bearing volatility risk, but it does not automatically mean the market is calm or mispriced.

Volatility Risk Premium Versus Related Terms

Volatility risk premium is easiest to understand when it is separated from the measurements around it. Implied volatility, realized volatility, and variance risk premium are connected, but they do not describe the same thing.

| Concept | What it describes | How it relates to VRP | Main misuse to avoid |

|---|---|---|---|

| Implied volatility | A volatility estimate embedded in option prices. | It is one side of the comparison used to infer volatility risk premium. | Treating implied volatility itself as the premium. |

| Realized volatility | The amount of price movement observed over a completed measurement window. | It is a common comparison point for judging whether implied volatility was high or low relative to actual movement. | Treating past movement as a complete forecast of future volatility. |

| Volatility risk premium | The compensation associated with bearing uncertainty around future volatility. | It is commonly inferred from implied volatility versus realized or expected realized volatility. | Treating it as a mechanical option-selling signal or guaranteed edge. |

| Variance risk premium | A related premium framed in variance terms rather than volatility terms. | It is closely related to VRP, especially in academic or institutional discussions. | Treating the phrase as a completely separate concept without checking the measurement frame. |

The practical distinction is that implied volatility is an input from option pricing, realized volatility is an observed outcome, and VRP is an interpretation of the compensation or pricing gap between the two.

Why Volatility Risk Premium Can Exist

Volatility risk premium can exist because volatility risk is difficult to bear. Option sellers or volatility risk takers may demand compensation for exposure to sudden movement, gap risk, changing correlations, liquidity pressure, and the possibility that realized volatility rises sharply when protection is most valuable.

Protection demand is one common driver. When investors want downside protection, they may bid up option prices. That can lift implied volatility relative to expected realized volatility, creating a wider inferred premium. The premium can also reflect dealer positioning, uncertainty around events, leverage constraints, or a broader shift in risk appetite.

None of those explanations works in isolation. A premium may widen because markets are stressed, but it may also widen because event uncertainty is concentrated in a specific maturity or asset. The interpretation becomes stronger when the same message appears across broader volatility, liquidity, credit, and risk-premium evidence.

What Volatility Risk Premium Does Not Prove

Volatility risk premium can be useful context, but it should not be treated as a standalone forecast, mechanical option-selling edge, crash warning, or complete market-stress reading. The interpretation becomes stronger only when it aligns with broader volatility, liquidity, risk-premium, and market-stress evidence.

VRP does not forecast market direction by itself. A market can have a positive volatility risk premium while prices rise, fall, or move sideways. The premium describes compensation for bearing volatility uncertainty, not a directional view on the underlying asset.

VRP also does not prove that volatility selling is attractive. A premium can exist because the risk being absorbed is real. Periods of calm realized volatility can be interrupted by sudden repricing, and the compensation that looked attractive before the move may not be enough after liquidity conditions change.

For market-structure interpretation, VRP is best treated as one piece of context. It can support a stress reading when it appears alongside persistent volatility behavior, liquidity pressure, wider credit or risk premia, and other signs of market fragility. It is weaker when it appears alone.

Practical Scenario

A common scenario is that investors become more willing to pay for protection before an uncertain policy decision, earnings window, or macro event. Option prices rise, implied volatility increases, and the implied reading may move above the level of volatility that market participants expect to realize.

In that situation, volatility risk premium may widen because the market is paying more for protection and because the participants absorbing that risk demand compensation. That does not automatically mean a crash is coming. It means volatility risk is being priced more aggressively relative to the expected or later observed movement.

The reading becomes more meaningful if it aligns with volatility clustering, deteriorating liquidity, wider risk premia, or broader market stress evidence. Without that broader confirmation, the premium remains a pricing and compensation clue rather than a complete regime signal.

How It Fits Into Volatility and Stress Context

Volatility risk premium belongs in the volatility and stress toolkit because it connects option-market pricing with realized movement and investor demand for protection. It helps explain whether volatility risk is being priced with an extra cushion, but it does not replace the need to check market behavior across time and across related risk measures.

The measurement side depends on the distinction between implied volatility and realized volatility. The interpretation side depends on whether the premium is consistent with broader evidence such as persistent high movement, liquidity stress, forced hedging, or cross-asset risk repricing.

The safest use is conceptual rather than mechanical. VRP can help classify how markets are pricing uncertainty, but it should be read with surrounding market-structure evidence before it supports any broader conclusion about stress, risk appetite, or regime behavior.

FAQ

Is volatility risk premium a trading signal?

No. Volatility risk premium is a pricing and compensation concept. It may help interpret how volatility risk is being priced, but it does not create a buy signal, sell signal, or mechanical option-selling rule by itself.

Is volatility risk premium the same as implied volatility?

No. Implied volatility is derived from option prices. Volatility risk premium is commonly inferred by comparing implied volatility with realized or expected realized volatility.

What is the difference between volatility risk premium and variance risk premium?

They are closely related, but not identical in measurement. Volatility risk premium is usually discussed in volatility terms, while variance risk premium is framed in variance terms. Both relate to compensation for bearing uncertainty around future movement, but the exact calculation depends on the chosen measurement frame.