Realized volatility is the amount of price movement an asset has already shown over a selected measurement window. It is commonly calculated from returns and used to compare observed movement across periods, assets, or market conditions. It can help frame market stress, but it is backward-looking and does not predict future volatility or confirm a regime by itself.

What Realized Volatility Means

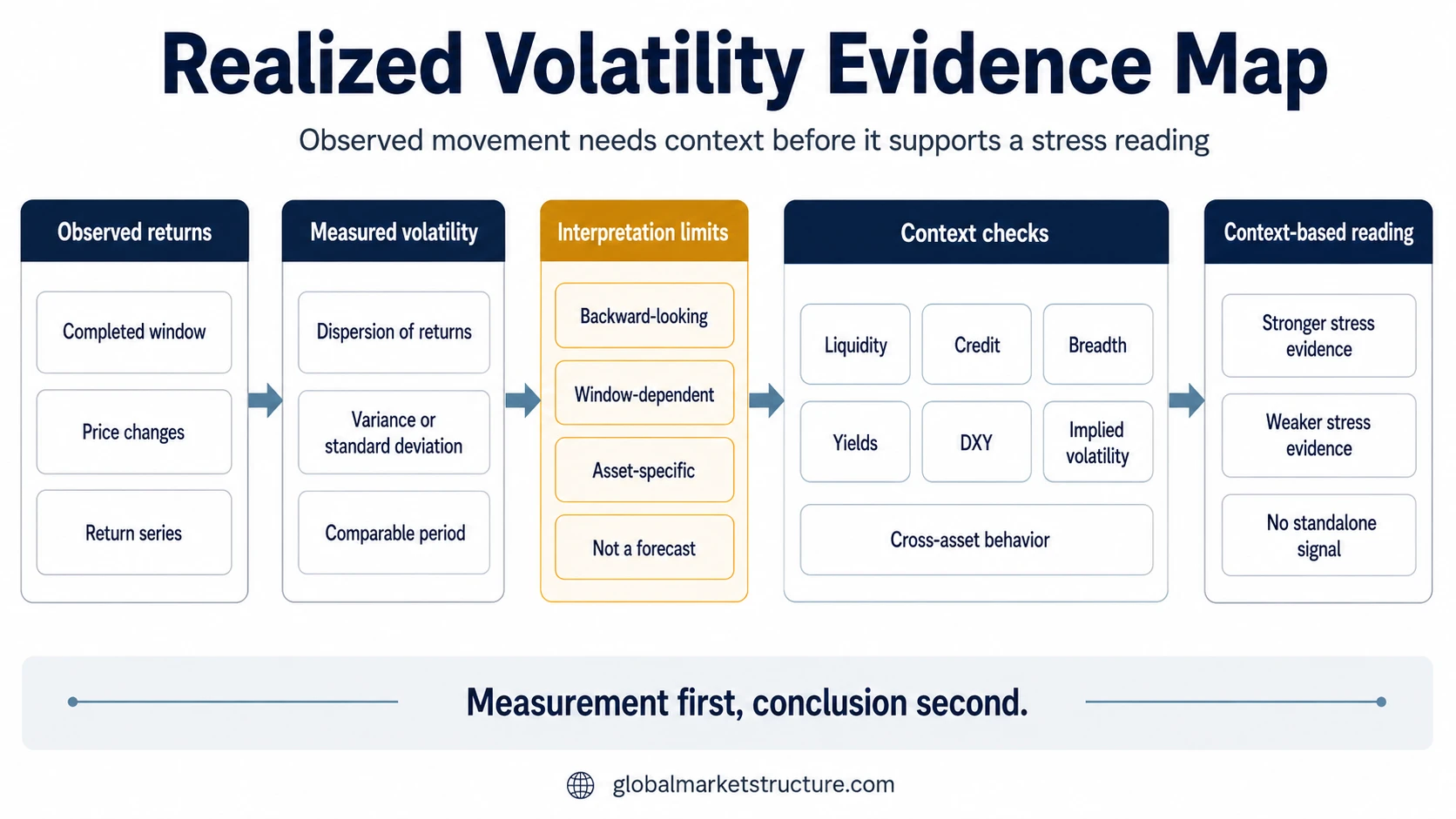

Realized volatility measures movement that has already occurred. It looks at actual price changes over a completed window, such as several days, weeks, months, or another defined period.

That makes realized volatility different from a forecast. It describes observed movement, not the market’s guaranteed next move. A high reading means price changes were larger during the chosen window. A low reading means price changes were smaller during that same kind of measurement window.

In market structure, realized volatility is useful because it turns price movement into a comparable measure. It can help compare calm periods with unstable periods, one asset with another, or one market environment with a previous environment.

How Realized Volatility Is Measured

Realized volatility is usually calculated from a series of returns rather than from raw price levels. The return observations are summarized through variance or standard deviation and are often annualized so different measurement windows can be compared more easily.

A compact way to think about the process is: price changes become returns, returns are summarized into dispersion, and dispersion becomes a volatility reading for the chosen window.

| Component | What it captures | What can distort the reading | Interpretation limit |

|---|---|---|---|

| Measurement window | The period used to observe price movement | Too short or too long a window can hide regime shifts or exaggerate temporary events | The number is window-dependent |

| Return series | The price changes used in the calculation | Gaps, illiquidity, outliers, or stale pricing can affect the reading | It measures observed movement, not cause |

| Variance or standard deviation | Dispersion of returns | Method choice and sampling frequency can change the output | It is a summary, not a full explanation |

| Annualization | Conversion into comparable yearly terms | Annualization can make a short burst of movement look large when expressed in yearly terms | Useful for comparison, not prediction |

| Asset context | The market where volatility is measured | Equities, rates, FX, credit, and commodities can behave differently | The same number can mean different things |

| Confirmation context | Broader market evidence around the volatility reading | Liquidity, credit, breadth, yields, DXY, and implied volatility may agree or conflict | Regime interpretation needs confirmation |

What Realized Volatility Tells You

Realized volatility tells you how much movement occurred during the measured period. It can identify whether price behavior was unusually quiet, unstable, compressed, or active relative to another period or asset.

It does not explain why the movement happened. A higher reading can come from policy repricing, earnings risk, forced selling, liquidity pressure, positioning, macro data, or normal asset-specific behavior. The number captures the movement, not the full cause.

That distinction matters for market stress analysis. Realized volatility becomes more useful when it is checked against credit spreads, liquidity conditions, breadth, yields, DXY behavior, option-priced volatility, and cross-asset participation.

Realized Volatility vs Implied Volatility

Realized volatility looks backward at movement that already occurred. Implied volatility looks forward through option prices and reflects the market’s priced expectation of future movement.

The two measures can move together, but they answer different questions. Realized volatility asks how much movement actually happened. Implied volatility asks how much movement the options market is pricing before the outcome is known.

The gap between priced expectation and observed movement can be useful, but it should not be compressed into a one-line signal. The broader implied vs realized volatility relationship depends on timing, option pricing, event risk, positioning, and whether the move was already anticipated.

Historical Volatility, Actual Volatility, and Realized Variance

Realized volatility is often discussed alongside historical volatility and actual volatility. In many educational contexts, those terms are used as close variants because they all refer to movement observed from past price data.

The terms are not always identical in technical usage. Historical volatility may be used as a broader label for past volatility estimates, while realized volatility often emphasizes measured returns over a specific completed window.

Realized variance is closely related, but it should stay separate from the main definition. In many technical contexts, realized variance and realized volatility are closely connected, with volatility often treated as a scaled square-root expression of variance. The exact treatment depends on the return series, sampling frequency, and scaling method.

Why Realized Volatility Can Mislead

Core limitation: Realized volatility is useful because it shows what has already happened in price movement. Its weakness is the same feature: it is backward-looking. It does not explain why the movement happened, whether it will continue, or whether the market is moving into a different volatility regime.

A high realized-volatility reading is not automatic proof of market stress. It may reflect genuine pressure, but it may also reflect a short-lived repricing, a scheduled event, a thin trading window, or movement that was already expected.

A low realized-volatility reading is not automatic proof of safety. Quiet movement can reflect stable conditions, but it can also reflect compression, crowded positioning, suppressed volatility, or a measurement window that has not yet captured a pending adjustment.

Common mistake: treating realized volatility as a complete market signal. The reading becomes stronger only when surrounding evidence confirms the same interpretation.

How Realized Volatility Fits Market Stress Analysis

Realized volatility is best treated as observed movement evidence inside a broader market-environment check. It can support a stress reading when larger price movement appears together with deteriorating liquidity, wider credit spreads, weaker breadth, unstable yields, defensive currency behavior, rising implied volatility, and broader cross-asset pressure.

The interpretation weakens when surrounding evidence does not confirm the same message. A volatility increase in one asset class can be less meaningful if credit remains calm, liquidity is stable, market breadth holds, and implied volatility had already priced the event.

Repeated or persistent realized-volatility behavior can become part of a broader volatility regime reading, but persistence matters. One measurement window rarely carries enough evidence by itself.

Illustrative Scenario

A market can show higher realized volatility after a sharp move in one asset class. That can look like stress, but the reading remains incomplete if credit spreads are calm, market breadth is stable, liquidity conditions have not deteriorated, and implied volatility had already priced the event.

The same realized-volatility increase becomes more meaningful when those surrounding conditions begin to confirm pressure. The number has not changed its basic definition, but the context around it has changed the interpretation.

Realized Volatility in Context

Realized volatility measures what happened, not what must happen next. Its value comes from disciplined comparison: across time, across assets, across measurement windows, and across related market indicators.

The strongest interpretation separates measurement from conclusion. Realized volatility can identify observed movement, but liquidity, credit, breadth, yields, DXY, implied volatility, and cross-asset behavior decide whether that movement supports a broader stress, calm, or regime reading.