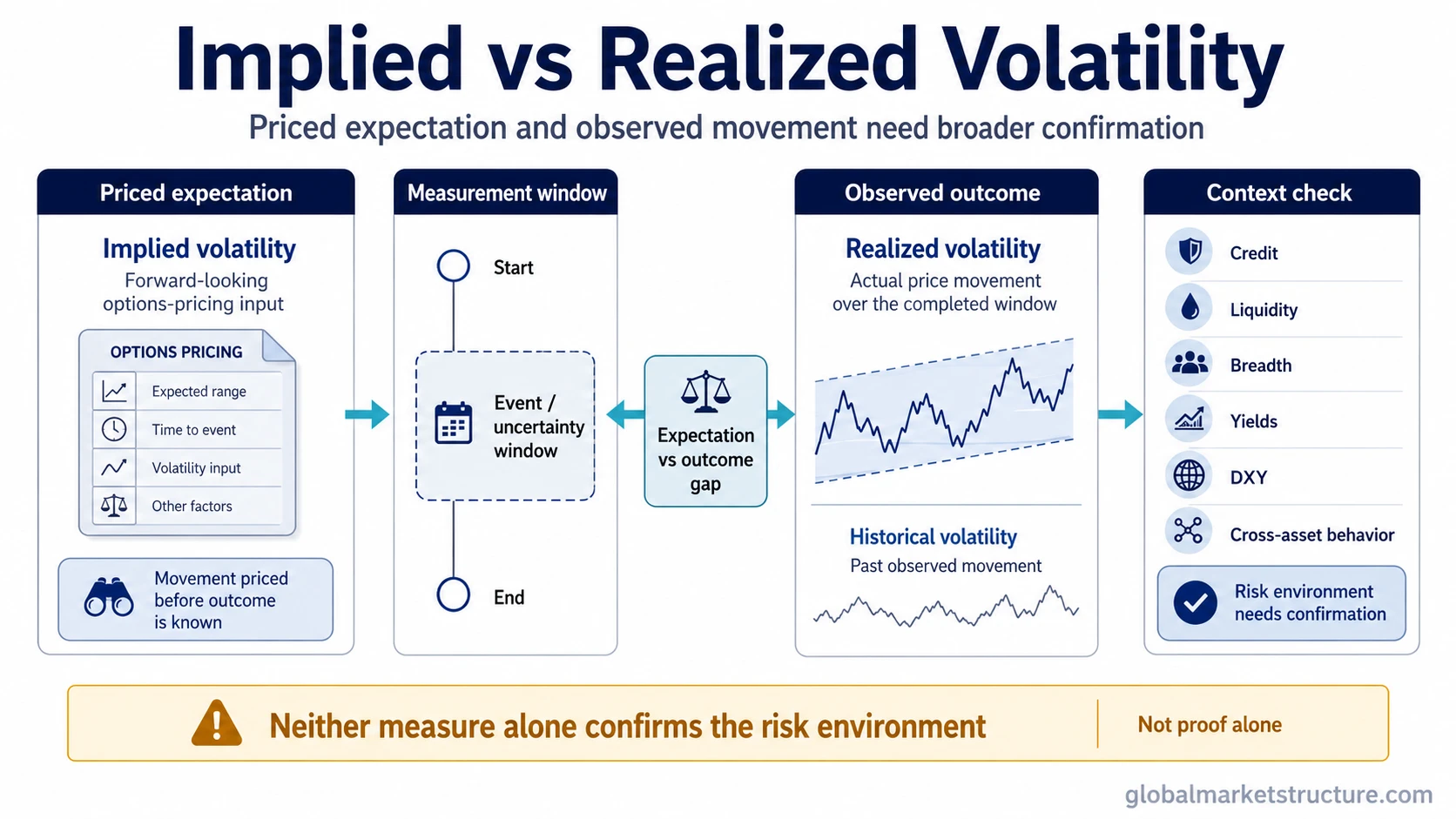

Implied vs realized volatility separates priced expectation from observed outcome. Implied volatility reflects future movement priced through options. Realized volatility measures how much the asset actually moved over a defined period. Historical volatility is often a close variant of realized volatility when it refers to past observed movement. Neither measure alone confirms the broader risk environment.

Key Points

- Implied volatility is forward-looking and derived from option prices.

- Realized volatility is calculated from actual price movement over a measured period.

- Historical volatility often overlaps with realized volatility when the focus is past observed movement.

- The useful distinction is expectation versus outcome, not better versus worse.

- The gap between the two can support interpretation, but it does not create a guaranteed edge.

- Volatility evidence becomes stronger when credit, liquidity, breadth, yields, DXY, and cross-asset behavior agree.

Implied vs realized volatility at a glance

| Criteria | Implied volatility | Realized volatility |

|---|---|---|

| Core question answered | How much movement is the options market pricing? | How much movement actually occurred? |

| Time orientation | Forward-looking expectation. | Observed movement over a completed or defined window. |

| Source | Option prices and the market’s pricing of future uncertainty. | Actual price changes measured over time. |

| What it reflects | Expected future volatility priced before the outcome is known. | The volatility that was actually realized during the measurement period. |

| Market-context use | Helps identify how much uncertainty is being priced in advance. | Helps compare the priced expectation with the movement that actually happened. |

| Main limitation | It is not a guaranteed forecast of future movement. | It does not automatically predict what comes next. |

| Common confusion | High implied volatility can be mistaken for a direct trading instruction. | Past realized movement can be mistaken for a complete forward-looking forecast. |

| Deeper concept | Implied volatility | Realized volatility |

What implied volatility measures

Implied volatility measures expected future movement as priced through options. It is not observed directly from past price movement. It is inferred from option prices, which can rise when traders demand more compensation for uncertainty or when the range of possible outcomes appears wider.

The important boundary is that implied volatility reflects pricing before the future path is known. It can be high before an event, during stress, or when uncertainty is expensive. That does not mean the asset must later move by the exact amount implied by options pricing.

In market-environment work, implied volatility is useful because it shows how uncertainty is being priced in advance. It becomes more informative when it is compared with actual movement and with other stress indicators rather than treated as a standalone conclusion.

What realized volatility measures

Realized volatility measures actual price movement over a defined window. When the period is already complete, it is backward-looking because it describes what happened rather than what the market expected beforehand.

Realized volatility can be measured across different windows, such as short event periods or longer historical periods. The chosen window matters because a short shock can look very different from a longer, calmer measurement period.

Historical volatility is often used as a close variant of realized volatility when the discussion refers to past observed movement. The terms are not always used with perfect consistency, so the safest reading is to check whether the speaker means actual past movement or expected future movement.

Why implied and realized volatility can diverge

Implied and realized volatility can diverge because they answer different questions. Implied volatility reflects the movement priced before the outcome is known. Realized volatility reflects the movement that actually occurred after prices had time to move.

The difference can appear around scheduled events, policy decisions, earnings windows, macro data releases, liquidity stress, or sudden repricing. Options may price a wide range of possible outcomes, but the actual move can end up smaller, larger, slower, or differently timed than expected.

That gap can support interpretation, but it should not be treated as automatic proof of mispricing. Without additional evidence, the comparison remains a way to separate expectation from outcome.

Same scenario, different meaning

Illustrative scenario: Before a major scheduled event, option prices may rise because the market is pricing a wider range of possible outcomes. That is the implied-volatility side of the situation.

After the event window passes, the actual price movement can be measured. That is the realized-volatility side. If the asset moves less than expected, realized volatility can come in below the movement that had been priced. If the move is larger or more disorderly, realized volatility can exceed the prior expectation.

The same scenario can therefore produce two different readings. Before the window, implied volatility describes priced uncertainty. After the window, realized volatility describes the observed outcome.

How the comparison supports risk-environment interpretation

The comparison can support volatility and stress analysis because it separates what markets feared from what actually happened. When implied volatility rises sharply, markets may be pricing uncertainty. When realized volatility rises sharply, actual price movement has already become more unstable.

A stronger risk-environment reading usually needs more than a volatility measure. Credit spreads, liquidity conditions, market breadth, yields, DXY behavior, and cross-asset participation can either support or weaken the interpretation.

For example, rising implied volatility alongside wider credit spreads and weaker breadth can carry a different message than rising implied volatility while credit remains calm and liquidity conditions are stable. The volatility reading becomes more useful when alternative explanations remain visible.

Important limitations

- Implied volatility is not a guaranteed forecast of future realized movement.

- Realized volatility is not a standalone predictor of the next market move.

- The comparison does not identify the best trade or the right options strategy.

- An implied-volatility index can add context, but it does not classify the full risk regime by itself.

- Broader confirmation is needed from credit, liquidity, breadth, yields, DXY, and cross-asset behavior.

Common mistakes when comparing implied and realized volatility

Mistake 1: Treating high implied volatility as a direct instruction. High implied volatility means uncertainty is being priced, not that a specific trade is automatically justified.

Mistake 2: Treating realized volatility as a complete forward forecast. Realized volatility describes measured movement over a window. Future conditions can change.

Mistake 3: Using historical volatility and realized volatility as if the wording is identical in every context. Historical volatility usually refers to past observed movement, but context still matters.

Mistake 4: Letting one volatility measure define the whole market regime. Volatility can support a risk reading, but a broader regime view needs confirmation across multiple markets.

When to use each concept

| Question | Most relevant concept | Safe interpretation |

|---|---|---|

| How much uncertainty is being priced before the outcome? | Implied volatility | Use it to understand priced expectation, not guaranteed movement. |

| How much did the asset actually move over the measurement window? | Realized volatility | Use it to measure observed outcome, not a complete forecast. |

| Did the market price more movement than actually occurred? | Both | Compare expectation with outcome, while avoiding unsupported edge claims. |

| Is volatility confirming broader market stress? | Both, plus confirmation | Check credit, liquidity, breadth, yields, DXY, and cross-asset behavior. |

| Is historical volatility the same as realized volatility? | Usually close when discussing past observed movement | Check the measurement window and the context of the wording. |

Bottom line

Implied volatility is priced expectation. Realized volatility is observed outcome. The comparison is useful because it separates what markets expected from what actually happened, but it does not remove uncertainty or confirm a full risk regime on its own.

In volatility and stress analysis, the strongest reading comes from comparing priced uncertainty, observed movement, and broader confirmation across credit, liquidity, breadth, yields, DXY, and cross-asset behavior.