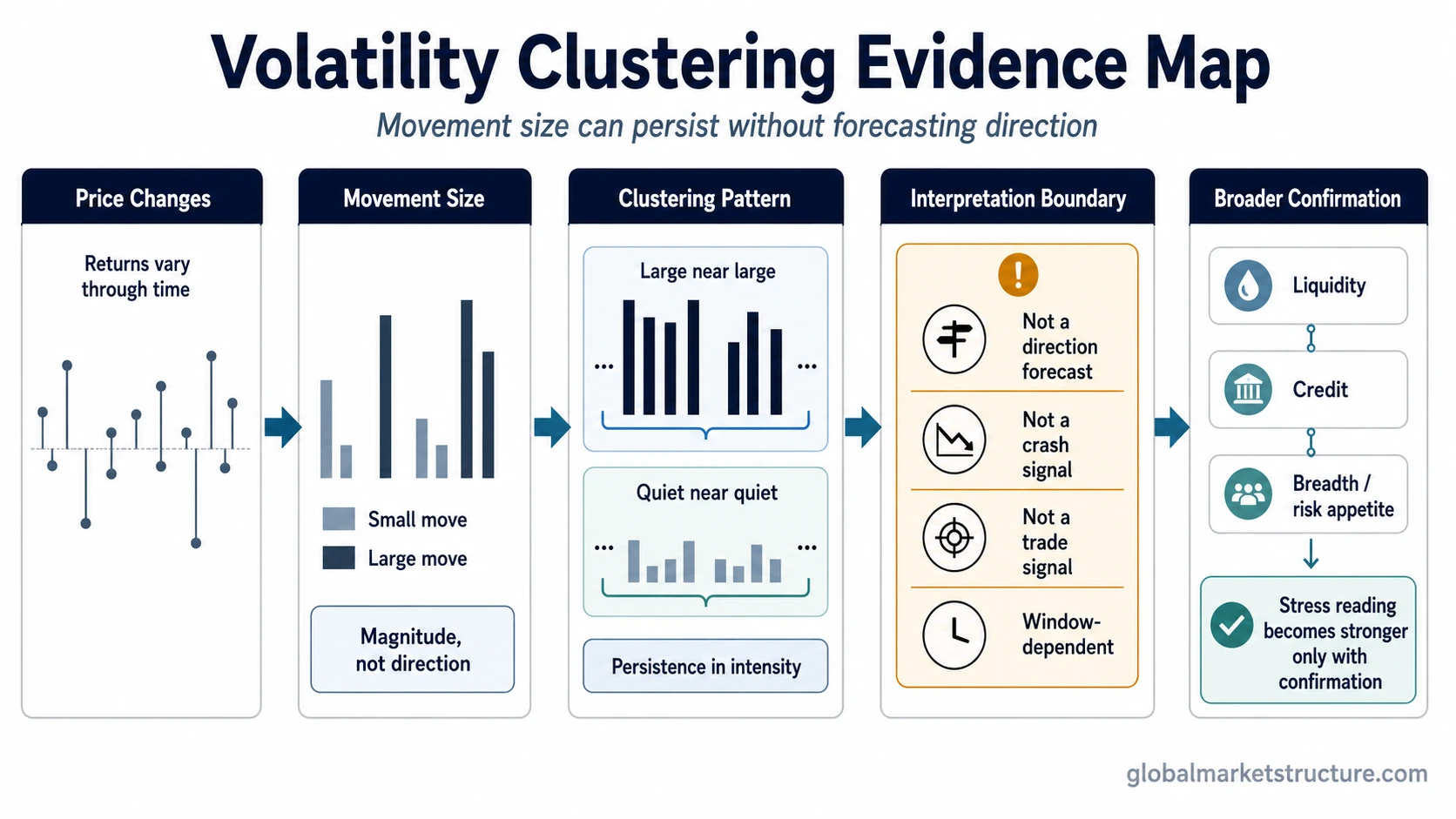

Volatility clustering is the tendency for large price moves to appear near other large moves and quiet periods to appear near other quiet periods. It describes persistence in the size of market movement, not a prediction about whether prices will rise or fall. The pattern can support risk-environment analysis, but it does not prove market stress without broader confirmation.

What volatility clustering is and is not

Volatility clustering is useful because it separates the intensity of movement from the direction of movement. A market can move sharply upward, sharply downward, or sideways with large intraperiod swings. The clustering concept focuses on whether similar movement intensity keeps appearing close together over time.

| What volatility clustering is | What it is not |

|---|---|

| Persistence in the size of market moves | A direction forecast |

| High-volatility periods appearing near other high-volatility periods | Proof of a crash |

| Low-volatility periods appearing near other quiet periods | A buy or sell signal |

| A useful clue for risk-environment interpretation | A complete market-stress reading |

| A pattern that can be measured over a defined window | A guarantee that volatility will continue |

How volatility clustering appears in market data

Volatility clustering appears when the size of price changes is not evenly scattered through time. Large changes tend to group near other large changes, while small changes tend to group near other small changes. The result is a market series that alternates between calmer patches and more active patches instead of moving with constant intensity.

In market data, the pattern is often studied through absolute returns, squared returns, or the autocorrelation of volatility-like measures. Statistical models such as ARCH and GARCH are commonly associated with this idea because they allow volatility to vary through time rather than assuming one constant level. A Global Market Structure page does not need to become a model-estimation tutorial to use the concept correctly.

Measurement boundary: The reading depends on the asset, return interval, and lookback window. A cluster on daily data may not carry the same meaning as a cluster on intraday or monthly data. The concept becomes more useful when the measurement window matches the question being asked.

Why volatility clustering matters for market-structure interpretation

Volatility clustering matters because persistent movement intensity can reveal that a market is no longer behaving as a sequence of isolated shocks. When large moves keep appearing near one another, participants may be reacting to changing uncertainty, thinner liquidity, faster repricing, or a shift in risk appetite.

The interpretation still needs confirmation. Clustered volatility can support a broader stress reading when it appears alongside other evidence, such as deteriorating liquidity, weaker breadth, wider credit spreads, unstable options pricing, or cross-asset risk-off behavior. Without those confirming layers, the same clustering pattern may simply describe a more active market rather than a stressed one.

Interpretation limit: Volatility clustering is one clue, not the whole risk-environment diagnosis. It describes persistence in movement size. It does not identify the cause of the movement, the direction of the next move, or whether stress is systemic.

A common false reading

The most common mistake is treating volatility clustering as if it automatically points to downside risk. It does not. A market can rally with clustered volatility if repricing is fast, participation is broad, or expectations are changing quickly. A market can also fall with clustered volatility if selling pressure keeps feeding on itself.

The direction question has to be read separately from the volatility question. Price trend, breadth, liquidity, credit, positioning, and cross-asset confirmation determine whether clustered movement is part of a constructive repricing, a disorderly selloff, or a mixed transition between regimes.

Volatility clustering versus nearby concepts

Volatility clustering sits near several related volatility and stress concepts, but it should not replace them. The clean distinction is that clustering describes serial behavior in movement intensity, while the nearby concepts describe broader states, pricing relationships, or stress conditions.

| Concept | Main meaning | How it differs from volatility clustering |

|---|---|---|

| Volatility | The size or variability of price movement | Volatility clustering focuses on whether high or low movement periods persist near themselves over time. |

| Volatility regime | A broader environment where volatility stays elevated, compressed, unstable, or transitioning | Clustering describes a pattern inside movement behavior; a regime describes the broader volatility state. |

| Volatility risk premium | The relationship between implied volatility compensation and realized volatility outcomes | Clustering concerns persistence in observed or measurable movement, not the pricing of volatility risk compensation. |

| Market stress | A broader pressure condition across liquidity, credit, breadth, options, and cross-asset behavior | Clustering can support a stress reading, but it is not stress proof by itself. |

How to interpret the concept safely

The safest use of volatility clustering is as a boundary-setting concept. It tells the analyst that movement intensity may be persistent, so a single calm or volatile observation should not be overread in isolation. The next question is whether other market-structure evidence agrees with the volatility reading.

Useful interpretation sequence: identify whether movement intensity is clustering, check whether the cluster is high or low volatility, separate direction from magnitude, then compare the reading with liquidity, breadth, credit, options, and cross-asset behavior.

When the surrounding evidence is mixed, volatility clustering should remain a descriptive observation. When the surrounding evidence also points toward pressure, it can become part of a stronger risk-environment reading. The distinction prevents the concept from becoming a signal, forecast, or standalone market-stress label.