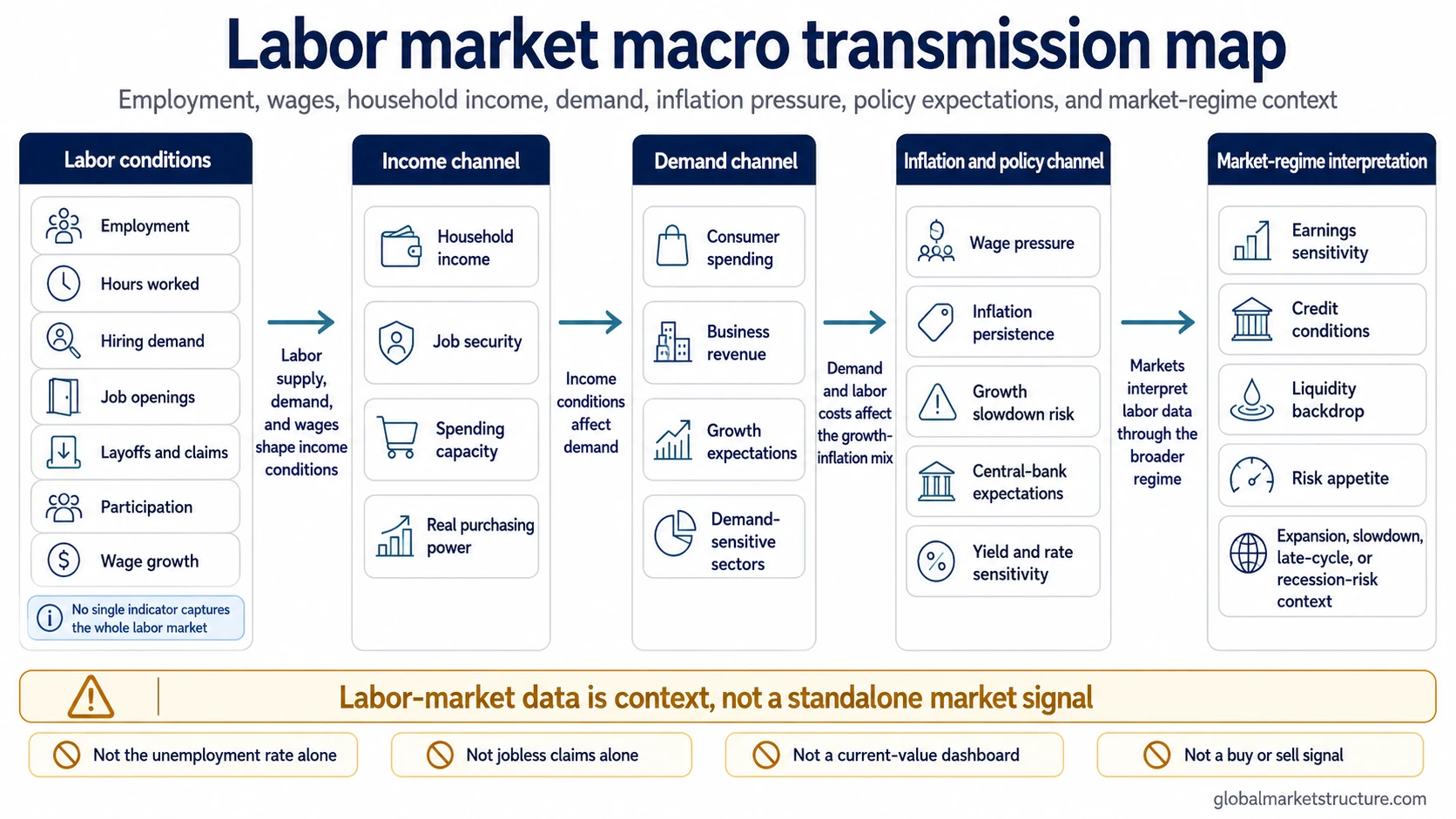

The labor market is the system where workers supply labor and employers demand labor through hiring, wages, job openings, layoffs, participation, and unemployment. In macro analysis, labor conditions shape household income, spending capacity, inflation pressure, policy expectations, corporate earnings sensitivity, and broader market-regime interpretation.

The labor market is broader than the unemployment rate. Unemployment measures one part of labor slack, while the full labor market also includes participation, wage growth, job creation, job openings, layoffs, hours worked, claims data, and survey-based expectations.

Labor-market data should not be treated as a standalone buy or sell signal. It works best as one part of a larger macro sequence connecting employment conditions to income, demand, inflation, central-bank reaction, earnings expectations, and risk appetite.

Key Points

- The labor market connects workers, employers, wages, hiring, layoffs, participation, unemployment, and hours worked.

- It is broader than the unemployment rate because labor conditions can improve or weaken across several indicators at once.

- Strong labor conditions can support household income and demand, while weak labor conditions can pressure spending and earnings expectations.

- Labor data can affect inflation expectations and policy expectations, especially when wage growth, employment, and demand move together.

- Labor-market interpretation is strongest when combined with inflation, policy, liquidity, credit, earnings, and market-regime context.

What is the labor market?

The labor market is the relationship between people who are available for work and employers who need workers. It includes the quantity of labor supplied, the demand for labor, the price of labor through wages, and the flow of people into and out of jobs.

A strong labor market can show up through easier job placement, low or falling unemployment, limited layoffs, resilient hours, and firmer wage growth. A weakening labor market may show up through slower hiring, rising unemployment, lower participation, weaker hours, more layoffs, or softer wage pressure.

No single indicator captures the whole system. A low unemployment rate can coexist with weak participation. Strong payroll growth can coexist with slowing hours. Rising wages can support spending, but they can also affect inflation pressure and policy expectations.

What the labor market includes

The labor market combines labor supply, labor demand, compensation, job flows, and labor slack. These components often move at different speeds, which is why labor-market interpretation requires more than one data point.

| Component | What it describes | Why it matters in macro analysis |

|---|---|---|

| Employment | How many people are working | Employment supports income, spending capacity, tax receipts, and business revenue. |

| Unemployment | How much available labor is not employed | Unemployment helps measure slack, income pressure, and potential weakness in demand. |

| Participation | How many people are working or actively looking for work | Participation affects how unemployment should be interpreted and whether labor supply is expanding or shrinking. |

| Wages | The price employers pay for labor | Wage growth can support spending, affect margins, and influence inflation and policy expectations. |

| Hiring and job openings | Employer demand for workers | Hiring demand can show whether firms are expanding, cautious, or reducing labor needs. |

| Layoffs and claims | Labor-market separation and job-loss pressure | Layoffs and first-time unemployment filings can provide timely signals of stress. |

| Hours worked | How much labor is being used before headcount changes | Falling hours can appear before broader job losses because firms may reduce hours before cutting staff. |

Labor market vs unemployment rate

The unemployment rate is one important labor-market indicator, but it is not the same as the labor market. It measures the share of the labor force that is unemployed and actively looking for work.

The broader labor market includes the unemployment rate plus job creation, wage growth, labor-force participation, hours worked, job openings, claims, layoffs, and employer demand. These indicators can send different messages during turning points.

| Concept | Scope | Common misreading |

|---|---|---|

| Labor market | Full system of employment, labor supply, labor demand, wages, participation, and job flows | Assuming one number summarizes the entire employment backdrop |

| Unemployment rate | One measure of labor slack among people in the labor force | Assuming low unemployment always means the entire labor market is healthy |

Why labor-market data matters for macro analysis

Labor-market data matters because employment and wages are central to household income. When more people work, hours are stable, and wages are supported, households generally have more capacity to spend. That spending can support revenue, economic growth, and demand-sensitive sectors.

Labor data also matters for inflation and policy. If wage growth remains firm while employment is strong, policymakers may worry that demand and labor costs are keeping inflation pressure elevated. If hiring weakens and unemployment rises, policymakers may become more concerned about growth, income pressure, and recession risk.

Markets often respond not only to whether labor data is strong or weak, but to what it changes about the path of growth, inflation, yields, central-bank expectations, earnings, credit risk, and liquidity conditions.

The labor-market transmission sequence

Labor conditions connect to markets through a sequence rather than a single direct signal.

| Step | Transmission path | Market-regime relevance |

|---|---|---|

| 1. Hiring and employment | Employers add or reduce workers and hours. | Changes the income base behind household demand. |

| 2. Wages and income | Labor compensation affects household cash flow. | Influences spending capacity and inflation pressure. |

| 3. Consumption and demand | Households adjust spending based on income security and purchasing power. | Shapes revenue, margins, and growth expectations. |

| 4. Inflation and policy | Strong demand and wage pressure can affect inflation and central-bank expectations. | Feeds into rates, yields, discount rates, and liquidity expectations. |

| 5. Market-regime interpretation | Labor data is weighed against inflation, credit, liquidity, earnings, and positioning. | Helps distinguish expansion, slowdown, late-cycle pressure, and recession-risk regimes. |

Labor supply and participation

The labor market cannot be understood without labor supply. The labor force participation rate helps show how many people are working or actively looking for work relative to the working-age population.

Participation matters because it changes the meaning of unemployment. A falling unemployment rate can look strong, but if participation is also falling, part of the improvement may reflect people leaving the labor force rather than stronger job creation.

When participation rises, the labor market may absorb more workers without the same wage pressure. When participation is constrained, employers may face tighter labor supply, which can support wages even if hiring growth slows.

Labor demand, hiring, and layoffs

Labor demand reflects how much employers want to hire, retain, or reduce workers. Hiring, job openings, hours worked, and layoff activity all help show whether firms are expanding or becoming cautious.

Hiring can slow before unemployment rises. Employers may first reduce job postings, slow replacement hiring, cut overtime, or reduce hours. If weakness deepens, layoffs and unemployment claims can rise later.

This timing matters because some labor indicators are lagging while others are more timely. A labor market can look stable in headline unemployment while other measures are already showing weaker demand for labor.

Wages, income, and inflation pressure

Wages are the price of labor. Wage growth can support household income and consumer spending, but it can also affect business costs, margins, inflation expectations, and central-bank policy expectations.

Wage growth does not have one fixed interpretation. When productivity is improving and demand is healthy, wage gains may support expansion without the same inflation pressure. When labor supply is tight and demand is strong, wage growth may reinforce inflation concerns.

For market-regime analysis, wage data is most useful when combined with employment growth, participation, inflation, productivity, margins, and policy expectations.

What labor-market data is not

Labor-market data is often misread because individual indicators are treated as complete signals. The labor market is not the unemployment rate alone, not a real-time market dashboard, and not a direct forecast for asset prices.

| Misreading | Better interpretation |

|---|---|

| Low unemployment means no macro risk | Unemployment can lag. Participation, claims, hours, hiring, credit, and earnings may show stress earlier. |

| Strong wage growth is always bullish | Wages can support consumption, but may also affect inflation, margins, and policy expectations. |

| Weak labor data is always good for markets because policy may ease | Policy expectations may improve, but earnings, credit, and demand risks can also rise. |

| One labor report defines the regime | Labor data should be interpreted across trend, revisions, composition, and macro context. |

How to use labor-market data without overclaiming it

Labor-market data is most useful when it is interpreted as part of a wider macro framework. Employment, wages, participation, unemployment, claims, hours, and job openings each answer different questions about labor supply, labor demand, income, and slack.

Current values, revisions, seasonal adjustment details, survey methodology, and official release definitions belong with official labor-statistics sources before any dated claim is made.

A safer interpretation starts with trend and composition. A single strong jobs number may mean something different if hours worked are falling, participation is changing, wage growth is slowing, or unemployment claims are rising.

Labor data becomes more useful when it is compared with inflation, credit spreads, yield-curve behavior, liquidity conditions, corporate earnings, sector leadership, and consumer-demand indicators.

Practical scenario

A common scenario is that unemployment remains low while job openings fall, hours worked soften, and initial unemployment claims begin to rise. The headline labor market may still look resilient, but the underlying flow of labor demand is weakening.

That does not automatically mean a recession or market decline is certain. The interpretation becomes stronger if softer labor demand appears alongside weaker income growth, slowing consumption, wider credit spreads, lower earnings guidance, and tighter liquidity conditions.

The practical distinction is between a labor-market slowdown and a full macro-regime shift. Labor data provides part of the evidence, but confirmation usually depends on whether demand, credit, liquidity, earnings, and policy expectations move in the same direction.

The labor market as a macro-driver endpoint

The labor market is one of the main bridges between economic activity and household demand. Employment supports income, income supports spending capacity, and spending capacity affects growth, inflation, business revenue, and earnings sensitivity.

The strongest labor-market interpretation separates the indicator from the conclusion. Employment, unemployment, participation, wages, claims, job openings, and hours worked each describe a different part of the system. The market implication depends on how those pieces interact with inflation, policy, liquidity, credit, and risk appetite.

The labor market is therefore best understood as a macro-driver endpoint. It helps interpret demand, inflation, policy expectations, earnings sensitivity, and market regimes, but it should not be reduced to one indicator or treated as a standalone market signal.

FAQ

What is the labor market in simple terms?

The labor market is the system where workers offer labor and employers demand labor. It includes jobs, wages, hiring, layoffs, unemployment, participation, and hours worked.

Is the labor market the same as the unemployment rate?

No. The unemployment rate is one labor-market indicator. The broader labor market also includes participation, wages, job openings, layoffs, claims, hiring, and hours worked.

Why does the labor market matter for the economy?

The labor market matters because employment and wages affect household income, spending capacity, inflation pressure, business revenue, policy expectations, and economic-cycle interpretation.

Why does the labor market matter for financial markets?

Labor conditions can affect growth expectations, inflation expectations, central-bank policy expectations, earnings sensitivity, yields, credit conditions, and risk appetite. They should be interpreted with broader macro and market context.

Can labor-market data predict market direction?

Labor-market data should not be treated as a standalone market-direction signal. It is more useful as part of a broader framework that also includes inflation, policy, liquidity, credit, earnings, positioning, and risk conditions.