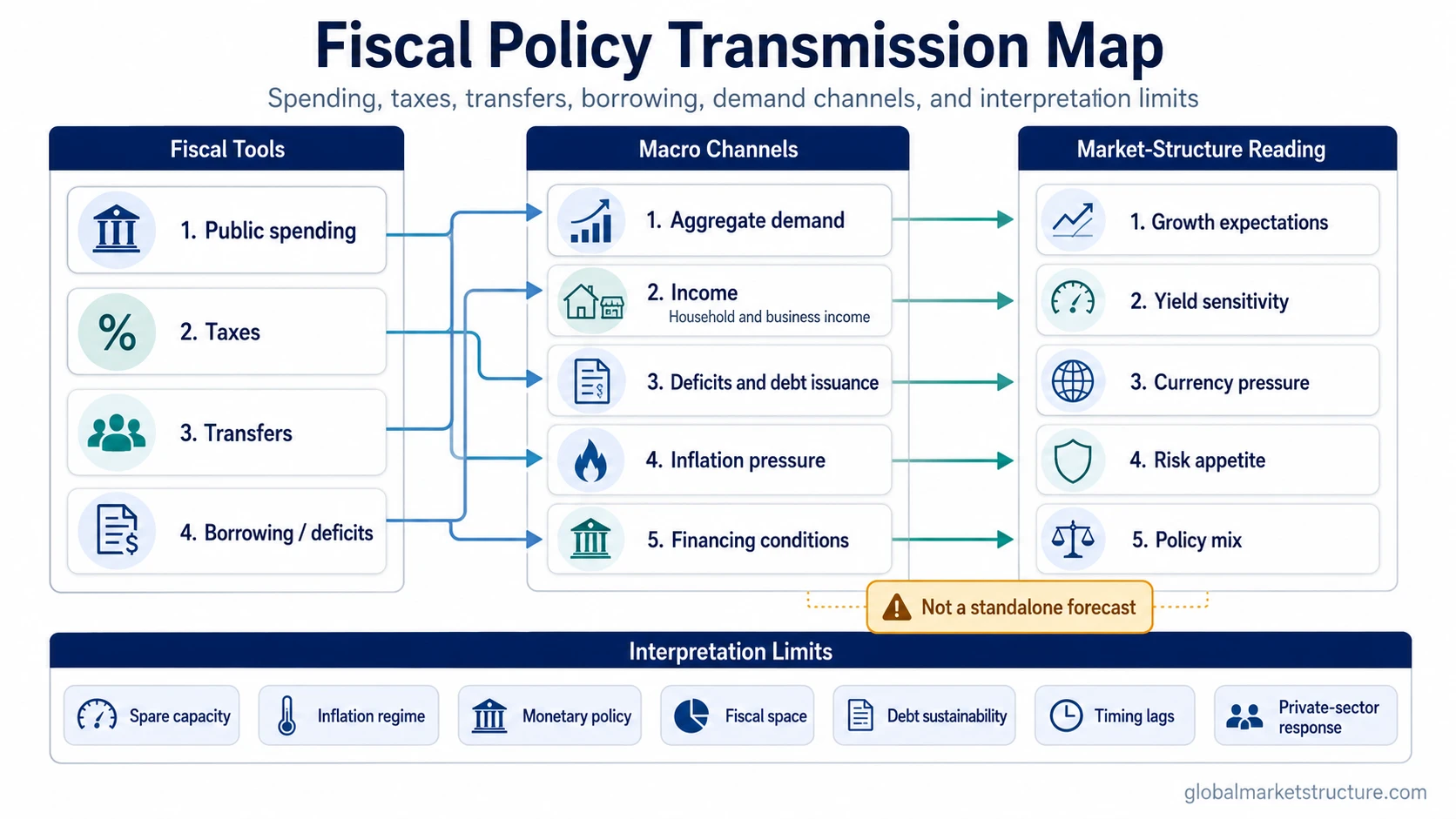

Fiscal policy is the government budget-policy channel that uses public spending, taxation, transfers and borrowing to affect aggregate demand, income, deficits, inflation pressure and financing conditions. For market interpretation, it helps explain how government decisions can support or restrain demand, but it is not a standalone forecast for recession, durable inflation, yields, equities, FX or risk assets.

Definition: fiscal policy refers to government decisions that change spending, taxes, transfers, borrowing and the overall budget stance. The same policy action can support growth, increase financing needs, cool demand or change inflation pressure depending on spare capacity, monetary policy, private-sector behavior and market financing conditions.

Key Points

- Fiscal policy uses budget tools, not central-bank tools.

- Its main channels run through public spending, taxation, transfers, borrowing and deficits.

- Expansionary policy can support demand, while contractionary policy can restrain demand.

- Market interpretation depends on capacity, inflation conditions, fiscal space, debt sustainability and financing conditions.

- Fiscal policy can shape the macro environment, but it does not mechanically predict asset direction.

What Fiscal Policy Includes

Fiscal policy includes the main budget choices that alter the flow of income between the public sector and the private sector. The most common tools are spending, taxation, transfers and borrowing.

- Government spending: purchases of goods, services, infrastructure, defense, healthcare, education and other public programs.

- Taxation: changes in income taxes, corporate taxes, consumption taxes, payroll taxes or other revenue measures.

- Transfers: payments or benefits that move income to households, firms or other sectors without a direct purchase of output.

- Borrowing and deficits: financing choices that affect the supply of government debt and the future budget path.

- Fiscal stance: the overall loose, tight or neutral position created by the combination of spending, revenue and borrowing decisions.

The fiscal stance matters because the combined budget position can differ from any single policy measure. A tax cut paired with spending restraint may not have the same demand effect as a tax cut paired with larger public spending.

How Fiscal Policy Moves Through the Economy

Fiscal policy reaches markets through income, demand, deficits, inflation pressure and financing conditions. The channel can also interact with the monetary transmission mechanism when central-bank reaction functions, rates or broader financial conditions change.

| Fiscal action | Direct macro channel | Market-structure interpretation | Main limitation |

|---|---|---|---|

| Higher public spending | Raises direct demand for goods, services or investment activity | Can support nominal growth expectations and sector-level demand exposure | The effect depends on spare capacity, import leakage, execution speed and financing conditions |

| Tax cuts | Increase disposable income or after-tax cash flow | Can support consumption, business margins or private investment appetite | Households and firms may save the benefit, reduce debt or face offsetting inflation pressure |

| Transfers | Move income directly to households, firms or specific sectors | Can stabilize income, demand and credit quality during weak private demand | Impact depends on targeting, persistence and whether recipients spend or save the transfer |

| Tax increases or spending restraint | Reduce disposable income, public demand or fiscal support | Can cool demand expectations, inflation pressure or deficit concerns | Private demand, external demand or monetary easing can offset part of the drag |

| Higher borrowing needs | Increase government financing requirements and debt issuance | May influence yield pricing, currency sensitivity, term-premium concerns and risk appetite | Market response depends on savings, central-bank policy, credibility and debt sustainability |

Expansionary, Contractionary and Neutral Fiscal Policy

Fiscal policy is often described by its stance. The stance summarizes whether budget policy is adding support, removing support or leaving the demand impulse broadly unchanged.

- Expansionary fiscal policy: higher spending, lower taxes or larger transfers that support aggregate demand.

- Contractionary fiscal policy: lower spending, higher taxes or reduced transfers that restrain aggregate demand.

- Neutral fiscal policy: a budget stance that does not materially add to or subtract from demand.

The stance is not always obvious from headline spending or tax changes. A government may increase spending while also raising taxes, or cut taxes while reducing other forms of support. The net demand effect depends on the full budget mix.

Automatic Stabilizers and Discretionary Fiscal Policy

Fiscal policy can work automatically or through deliberate policy changes. Automatic stabilizers are budget features that move with the economy without requiring a new policy decision.

- Automatic stabilizers: unemployment benefits, progressive tax collections and other budget items that cushion income when activity slows or withdraw support when activity strengthens.

- Discretionary fiscal policy: deliberate changes such as new spending programs, tax changes, stimulus packages, subsidies or consolidation plans.

Automatic stabilizers usually adjust with the cycle, while discretionary measures depend on political decisions, administrative timing and implementation speed. That timing difference matters for market interpretation because a fiscal announcement may not equal immediate demand impact.

Fiscal Policy vs Monetary Policy

Fiscal policy and monetary policy are different policy channels. Fiscal policy comes from government budget decisions. Monetary policy comes from central-bank decisions around interest rates, balance-sheet policy, liquidity tools and financial-system operations.

| Policy channel | Main authority | Main tools | Primary transmission path |

|---|---|---|---|

| Fiscal policy | Government budget authority | Spending, taxes, transfers, borrowing | Income, demand, deficits and public financing needs |

| Monetary policy | Central bank | Policy rates, balance-sheet tools, liquidity operations | Interest rates, credit, liquidity and financial conditions |

The two channels can reinforce or offset each other. Fiscal stimulus paired with tight monetary policy may support demand while also raising financing-cost sensitivity. Fiscal consolidation paired with monetary easing may restrain budget support while lower rates cushion the drag.

Fiscal Policy, Fiscal Stance and Fiscal Impulse

Fiscal policy is the broad set of government budget tools. Fiscal stance describes the overall budget position at a point in time. Fiscal impulse focuses on the change in that stance and the likely demand effect of the change.

| Term | Meaning | Why it matters |

|---|---|---|

| Fiscal policy | The government use of spending, taxes, transfers and borrowing | Defines the policy tool set |

| Fiscal stance | The overall loose, tight or neutral budget position | Shows whether policy is broadly supportive or restrictive |

| Fiscal impulse | The change in fiscal stance relative to a prior period | Helps estimate whether the budget is adding or removing demand pressure |

A large deficit is not always a new stimulus impulse. If the deficit is already expected and no longer widening, the incremental effect on demand may be smaller than the headline deficit suggests.

Why Fiscal Policy Matters for Market Structure

Fiscal policy matters for market structure because it can change the balance between demand support, inflation pressure, financing needs and policy reaction. Those channels can affect how investors interpret growth expectations, yields, currency behavior, credit conditions and risk appetite.

Expansionary fiscal policy can support income and demand when private activity is weak. It can also increase borrowing needs or add inflation pressure if the economy is already near capacity. Contractionary policy can reduce deficit concerns or cool inflation pressure, but it can also weaken income growth and private demand.

The useful market question is not whether fiscal policy is good or bad. The useful question is which channel dominates under the current regime: demand support, inflation pressure, fiscal credibility, debt supply, central-bank response or private-sector offset.

When Fiscal Policy Readings Become Misleading

Fiscal policy should not be read as a standalone market signal. The same fiscal action can create different outcomes depending on economic slack, inflation conditions, monetary policy, debt sustainability, fiscal credibility, market expectations and external demand.

- Spare capacity changes the effect: stimulus may lift output more when unused labor and capacity exist, but may create more price pressure when capacity is tight.

- Financing conditions matter: higher deficits can be easier to absorb when savings are strong and yields are stable, but harder to absorb when rates and term premiums rise.

- Monetary reaction matters: central banks may offset fiscal demand support if inflation risk is high.

- Timing lags matter: fiscal announcements, approvals, spending flows and macro effects can occur on different timelines.

- Private-sector behavior matters: households and firms may save, deleverage or delay investment instead of spending immediately.

Practical Scenario: Demand Support With Yield Repricing

A government increases transfers and public investment while private demand is weak. The first effect may be stronger household income, improved sales expectations and better near-term demand. Bond yields can still rise if investors also reprice borrowing needs, future debt supply or inflation risk.

The market read is mixed rather than one-directional. Fiscal support can improve the demand side while tighter financing conditions create a separate restraint. A stronger interpretation requires confirmation from yields, inflation expectations, credit spreads, currency behavior and broader liquidity conditions.

Related Policy Concepts

Fiscal policy is one policy-transmission channel. Monetary policy covers central-bank tools rather than budget tools.

The direct distinction between the two policy levers is fiscal policy vs monetary policy.

Policy transmission through interest rates, credit, liquidity and financial conditions belongs to the monetary transmission mechanism.

FAQ

What is fiscal policy in simple terms?

Fiscal policy is the way a government uses spending, taxes, transfers and borrowing to influence demand, income, deficits, inflation pressure and financing conditions.

What are the main tools of fiscal policy?

The main tools are public spending, taxation, transfer payments, borrowing and the overall budget stance created by those decisions.

How is fiscal policy different from monetary policy?

Fiscal policy uses government budget tools. Monetary policy uses central-bank tools such as interest rates, balance-sheet policy and financial-system operations.

Does expansionary fiscal policy always push markets higher?

No. Expansionary fiscal policy can support demand, but market response also depends on inflation pressure, borrowing needs, central-bank policy, yields, currency conditions and risk appetite.

What is the difference between fiscal policy and fiscal impulse?

Fiscal policy is the broad budget tool set and stance. Fiscal impulse focuses on the change in that stance and the likely effect of the change on demand.