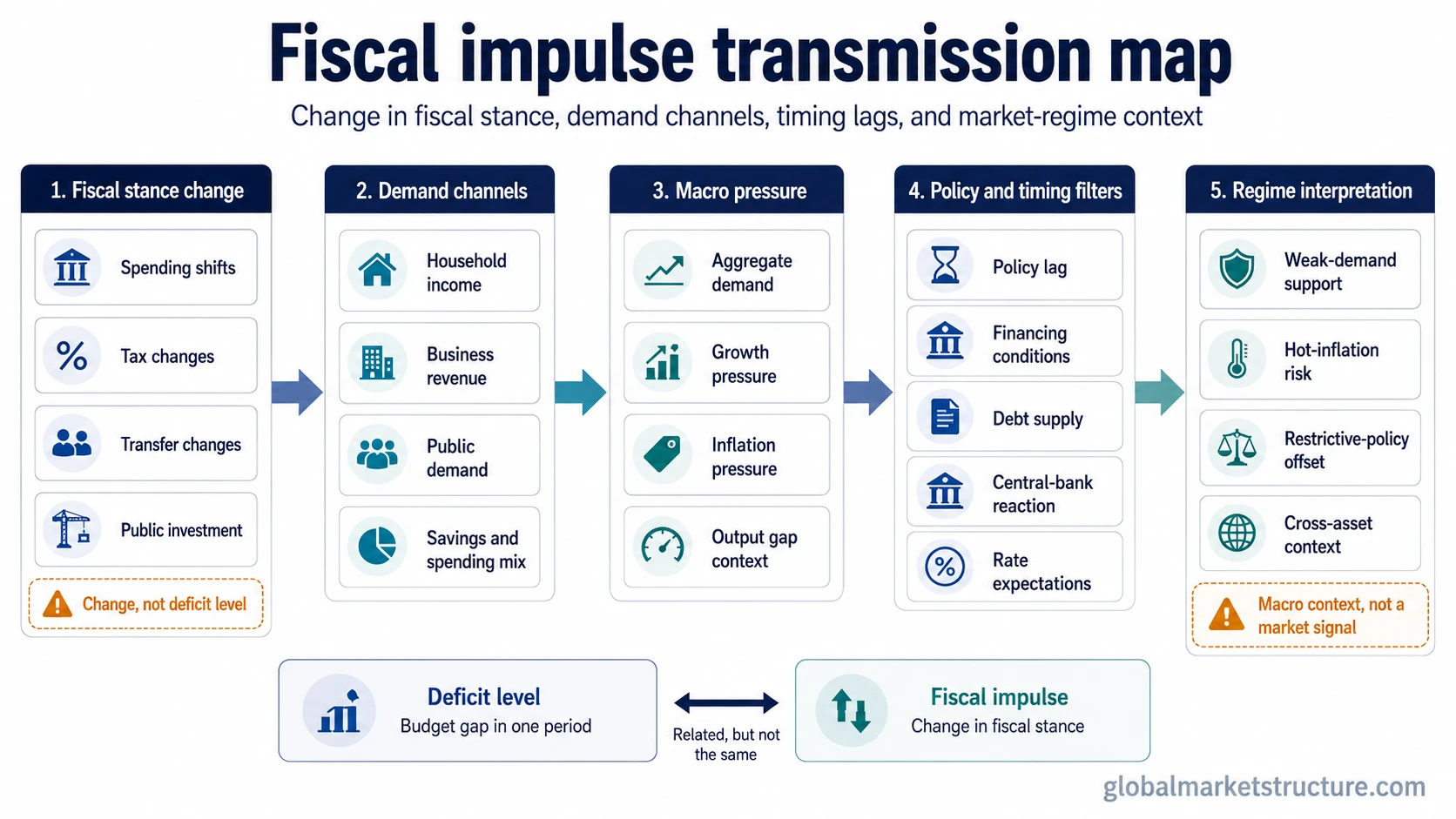

Fiscal impulse measures whether fiscal policy is becoming more expansionary or restrictive by focusing on the change in fiscal stance, not the deficit level alone. It tracks how changes in spending, taxes, and transfers can alter aggregate demand, growth pressure, inflation pressure, and policy expectations. For market interpretation, fiscal impulse is context, not a standalone signal, because its effect depends on timing, financing, monetary policy, and the broader regime.

Fiscal impulse is the change in the budget’s effect on the economy. A larger deficit can sometimes reflect economic weakness rather than new fiscal stimulus, while a smaller deficit can sometimes reflect stronger tax receipts rather than deliberate fiscal tightening. The useful question is not only whether the government is in deficit, but whether fiscal policy is becoming more supportive or more restrictive than before.

What fiscal impulse means

Fiscal impulse is used to describe the direction and change in fiscal policy pressure. A positive fiscal impulse usually means policy is becoming more expansionary. A negative fiscal impulse usually means policy is becoming more restrictive. The concept is about the change in stance, not simply the level of government borrowing.

The distinction matters because fiscal policy can affect the private economy through several channels. Higher public spending can add direct demand. Tax cuts can raise disposable income. Transfers can support household cash flow. Tax increases or spending restraint can work in the opposite direction.

Fiscal impulse therefore sits inside policy transmission. It helps connect budget decisions to aggregate demand, growth pressure, inflation pressure, and expectations for rates. It does not, by itself, say what markets should do next.

Fiscal impulse vs nearby concepts

| Concept | What it measures | Common mistake |

|---|---|---|

| Fiscal impulse | The change in fiscal stance or budget impact from one period to another. | Treating it as the same thing as the deficit level. |

| Fiscal deficit | The gap between government spending and government revenue over a period. | Assuming a larger deficit always means a more expansionary new impulse. |

| Fiscal policy | The broader toolkit of spending, taxation, transfers, and borrowing decisions. | Using the broad policy category when the question is about the change in stance. |

| Fiscal stance | The overall position of fiscal policy, often described as expansionary, neutral, or restrictive. | Confusing the stance itself with the change in that stance. |

| Fiscal multiplier | The estimated output response to a fiscal policy change. | Using multiplier size as if it were the same as the initial policy impulse. |

| Fiscal impact / fiscal effect | The estimated contribution of fiscal policy to growth or demand in a specific framework. | Assuming every framework uses the same formula, adjustment, or counterfactual. |

How fiscal impulse moves through the economy

Fiscal impulse starts with a policy change, but the economic effect depends on the channel. A spending increase, tax cut, transfer expansion, tax increase, or spending restraint can move through income, public demand, business revenue, inflation pressure, and rate expectations in different ways.

- Fiscal policy changes: spending, taxes, transfers, or public investment shift relative to the prior stance.

- Income and demand channels adjust: households, firms, or public-sector demand receive more or less support.

- Aggregate demand changes: the impulse can add to or subtract from spending pressure in the economy.

- Growth and inflation pressure respond: the same fiscal impulse can look different depending on slack, capacity, and price pressure.

- Policy expectations adjust: markets may reassess rates, central-bank reaction, funding needs, and debt supply.

- Market-regime interpretation changes: the fiscal impulse becomes one input inside a broader macro regime, not a direct market forecast.

The same fiscal impulse can be interpreted differently across regimes. Expansionary fiscal support during weak demand can be read differently from expansionary support when inflation is already high and monetary policy is restrictive. Policy lag matters here because spending, tax, and transfer decisions can reach households, firms, and public demand with delays.

How fiscal impulse is measured

Fiscal impulse is often linked to changes in the structural or cyclically adjusted budget balance. That matters because the actual deficit can change for reasons that have little to do with new policy decisions. A recession can widen the deficit through lower tax revenue and higher automatic stabilizers, even if the government has not chosen a new discretionary stimulus package.

Measurement frameworks try to separate policy-driven changes from changes caused by the business cycle. Some approaches focus on the change in the cyclically adjusted balance. Others use counterfactual estimates or direct fiscal-effect models that translate spending and tax changes into growth or demand contributions.

Measurement boundary: fiscal impulse does not have one universal formula that applies cleanly across every country, institution, or period. The estimate can change depending on the adjustment method, baseline, fiscal components included, timing assumptions, and whether the framework measures the policy impulse itself or the estimated economic effect.

Why fiscal impulse is not the same as the deficit

The fiscal deficit is a level. Fiscal impulse is a change. A country can run a large deficit without a new positive fiscal impulse if the deficit is not becoming more expansionary. A country can also show a shrinking deficit while fiscal policy is not necessarily tightening, especially if stronger growth raises tax receipts automatically.

This is why fiscal impulse is usually more useful for macro interpretation than a deficit number alone. The deficit can show the budget balance, but fiscal impulse asks whether the budget is adding more or less support to the economy than before.

A simple way to separate them is to ask two questions. The deficit question is: how large is the budget gap? The fiscal impulse question is: did the fiscal stance become more expansionary or more restrictive compared with the prior period?

Why fiscal impulse is not a market signal

A positive fiscal impulse does not automatically mean risk assets should rise. A negative fiscal impulse does not automatically mean risk assets should fall. Fiscal policy affects the macro backdrop, but market interpretation also depends on inflation, rates, financing conditions, central-bank reaction, output gap, risk appetite, valuations, and timing lags.

Expansionary fiscal policy can support demand, but it can also increase inflation pressure or raise concerns about debt issuance and financing conditions. Restrictive fiscal policy can reduce demand, but it can also ease inflation pressure or change expectations for monetary policy. The market effect depends on the regime around the impulse.

Common false reading: fiscal impulse is not a buy or sell trigger. It is a macro context variable. Its value comes from showing how fiscal policy pressure is changing, then comparing that shift with inflation, rates, liquidity, credit conditions, and market-cycle context.

Practical scenario

Tax receipts can rise when the economy is already strong. In that situation, the deficit may shrink, but the smaller deficit does not automatically prove that policymakers have tightened fiscal policy. The change may partly reflect the cycle rather than a discretionary decision.

A different scenario is that spending, tax, or transfer decisions make the structural stance more expansionary. In that case, fiscal impulse can become positive even if the headline deficit does not tell the full story. The market interpretation still depends on whether the economy has spare capacity, whether inflation is already high, how the spending is financed, and how monetary policy responds.

Related policy-transmission concepts

Fiscal impulse becomes easier to interpret when it is treated as one part of a policy mix rather than as a direct market signal. The monetary transmission mechanism matters because interest rates, credit conditions, liquidity, and inflation expectations can amplify or offset the fiscal impulse.

The safest macro reading treats fiscal impulse as one part of a policy mix. It helps classify whether fiscal policy is adding or removing demand pressure, but the broader regime determines how that impulse is absorbed by households, firms, central banks, bond markets, and risk assets.