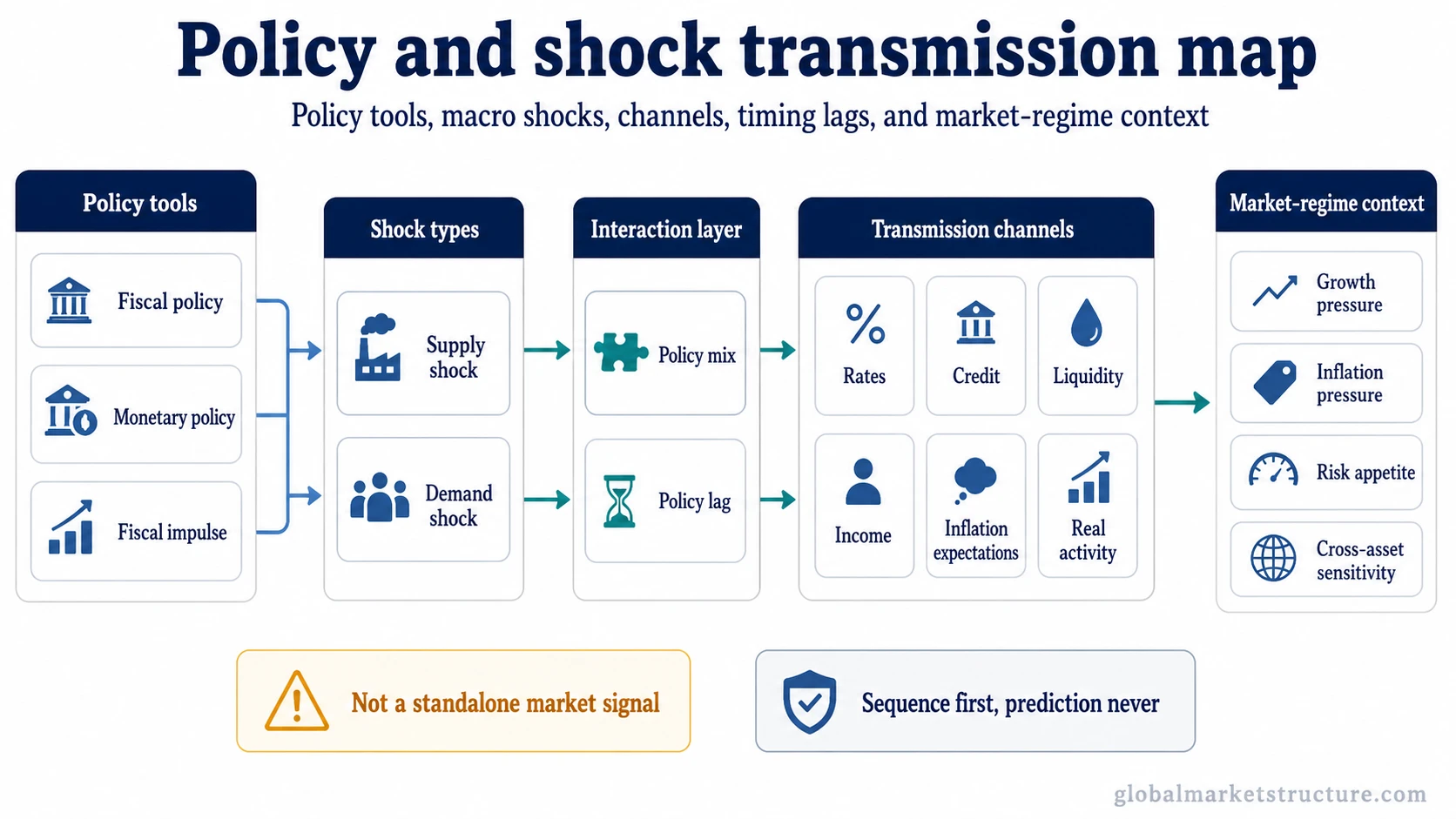

Policy and shock transmission organizes how policy tools and macro disturbances can move through growth, inflation, income, credit, liquidity, expectations, and market-regime conditions. The key distinction is whether the question is about a policy tool, a shock type, a policy combination, a timing lag, or the channel that carries policy into the economy and markets.

Policy tools, shocks, and transmission channels

Policy tools are deliberate settings such as government spending, taxation, interest rates, central-bank balance sheets, and guidance. Shocks are disturbances that can begin from supply, demand, credit, energy, income, or confidence conditions. Transmission is the path through which those forces affect borrowing costs, real activity, inflation pressure, liquidity, expectations, and market-regime interpretation.

The same macro headline can point to different concepts. A fiscal package is not the same as a demand shock. A central-bank rate change is not the same as a supply shock. A delayed response in employment, inflation, credit, or asset prices belongs closer to policy lag or transmission mechanics than to the policy decision alone.

Which concept should you start with?

| Question or signal | Start with | Why it fits |

|---|---|---|

| Government spending, taxation, deficits, or public-sector demand | fiscal policy | Fiscal policy describes how government budget choices affect demand, income, deficits, and macro conditions. |

| The size, direction, or demand effect of a fiscal change | fiscal impulse | Fiscal impulse focuses on whether public-sector policy is adding to or subtracting from demand pressure. |

| Rates, balance sheets, central-bank guidance, or financial conditions | monetary policy | Monetary policy covers central-bank settings that influence borrowing costs, liquidity, expectations, and financial conditions. |

| The path from policy action to rates, credit, income, inflation, and asset sensitivity | monetary transmission mechanism | Monetary transmission mechanism focuses on how policy moves through economic and financial channels. |

| Inputs, energy, logistics, production capacity, or goods availability | supply shock | A supply shock begins on the production, input, capacity, or availability side of the economy. |

| Spending, income, credit appetite, confidence, or private-sector demand | demand shock | A demand shock begins with changes in spending willingness, income flow, credit use, or demand conditions. |

| Fiscal and monetary settings pushing together or against each other | policy mix | Policy mix compares how fiscal and monetary settings interact instead of treating either tool in isolation. |

| Delayed effects, long transmission windows, or markets pricing ahead of realized data | policy lag | Policy lag explains why policy effects may appear with delays across growth, inflation, credit, labor, and markets. |

Core policy and shock concepts

Fiscal policy: Government spending, taxation, transfers, and deficits shape the public-sector demand channel.

Monetary policy: Central-bank rates, balance-sheet settings, guidance, and financial conditions influence borrowing costs, liquidity, expectations, and credit conditions.

Supply shock: Supply shock analysis starts with inputs, energy, production capacity, logistics, or availability constraints.

Demand shock: Demand shock analysis starts with spending, income, credit appetite, confidence, or private-sector demand conditions.

Policy mix: Policy mix compares fiscal and monetary settings when they reinforce, offset, or complicate each other.

Policy lag: Policy lag explains why policy effects can appear on different timelines across markets, credit, labor, inflation, and growth.

Fiscal impulse: Fiscal impulse focuses on the change in fiscal support or restraint, not only the level of spending or deficits.

Monetary transmission mechanism: Monetary transmission mechanism follows the channels from central-bank policy into rates, credit, income, inflation expectations, asset sensitivity, and real activity.

Common comparisons

Supply shock vs demand shock: Supply shocks begin with production, input, capacity, or availability constraints. Demand shocks begin with spending, income, credit appetite, or private-demand conditions. The distinction matters because inflation, growth, and policy interpretation can change depending on which side of the economy moved first.

Fiscal policy vs monetary policy: Fiscal policy works through government budgets, taxes, spending, transfers, and deficits. Monetary policy works through central-bank settings, rates, balance sheets, guidance, and financial conditions. They can reinforce each other, offset each other, or create mixed macro signals.

What policy and shock transmission does not tell you by itself

Policy and shock transmission is not a current-value dashboard. It does not prove that one policy action mechanically creates one market outcome. It also does not turn fiscal policy, monetary policy, supply shocks, demand shocks, and transmission channels into interchangeable signals.

Market interpretation becomes more useful when the source of pressure, the transmission channel, the timing lag, and the surrounding regime are separated. A rate move can affect credit conditions before it appears in labor data. A supply shock can lift inflation while weakening real demand. A fiscal impulse can support income while tighter monetary conditions may still pressure credit conditions, liquidity, or risk appetite.

How the concepts work together

A practical macro sequence often begins with one of three questions. Is the change coming from policy settings, from a supply-side disturbance, or from demand conditions? After that, the interpretation depends on the channel: rates, credit, liquidity, income, margins, inflation expectations, or market-risk appetite.

For example, a rise in energy costs usually starts closer to supply shock analysis, but the sequence can later involve demand conditions, monetary policy, or fiscal impulse depending on how income, prices, and policy responses change.

The useful distinction is sequence, not prediction. The first concept identifies the source of pressure. The next concept follows the channel. The final interpretation depends on whether the broader environment is shaped more by growth, inflation, liquidity, credit, income, or risk-regime pressure.