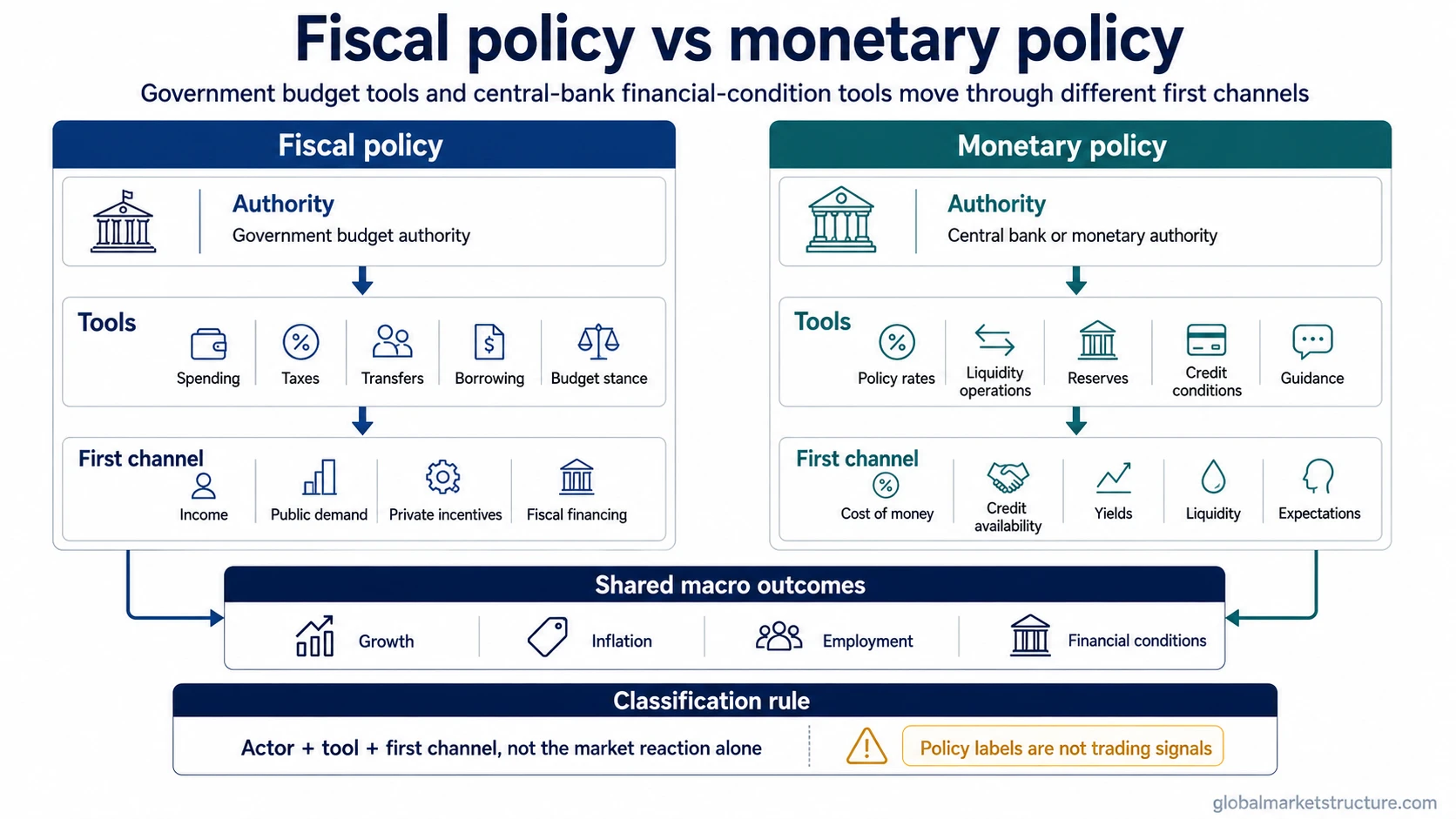

Fiscal policy vs monetary policy separates government budget action from central-bank financial-condition action. Fiscal policy works through spending, taxes, transfers, borrowing, and fiscal stance. Monetary policy works through rates, liquidity operations, reserves, credit conditions, and expectations. Both can affect growth, inflation, employment, and markets, but the policy label alone does not predict market direction.

Core distinction: fiscal policy starts with the government budget; monetary policy starts with the central bank’s control over financial conditions.

Key Points

- Fiscal policy is controlled by the government through spending, taxation, transfers, and budget stance.

- Monetary policy is controlled by the central bank through rates, liquidity, reserves, credit conditions, and expectations.

- The two can target similar macro outcomes, including growth, inflation, employment, and financial stability.

- The difference is not the goal alone. The difference is the authority, tool, and first transmission channel.

- Markets interpret both through starting conditions, inflation pressure, bond yields, liquidity, credit conditions, and the expected policy mix.

What fiscal policy and monetary policy mean

Fiscal policy refers to government decisions about spending, taxation, transfers, borrowing, and the overall budget stance. Its first impulse usually enters through public demand, household income, business incentives, sector allocation, or the government financing channel.

Monetary policy refers to central-bank decisions that influence interest rates, liquidity conditions, reserves, credit conditions, and expectations about future financial conditions. Its first impulse usually enters through the cost of money, credit availability, asset discount rates, bank funding conditions, and market expectations about future policy.

Definition: fiscal policy is classified by the budget tool being changed. Monetary policy is classified by the central-bank financial-condition tool being changed.

Fiscal policy vs monetary policy: criteria table

| Criteria | Fiscal policy | Monetary policy |

|---|---|---|

| Decision authority | Government budget authority, such as the legislature, treasury, finance ministry, or administration depending on the country. | Central bank or monetary authority. |

| Main tools | Government spending, taxation, transfers, subsidies, borrowing, and budget stance. | Policy rates, reserve settings, liquidity operations, central-bank asset purchases where applicable, and guidance that affects financial conditions. |

| First transmission channel | Income, demand, public-sector spending, private-sector incentives, and fiscal financing. | Interest rates, credit conditions, liquidity, bank reserves, yields, exchange-rate pressure, and expectations. |

| Growth path | Can support or restrain demand through government spending, tax changes, transfers, and incentives. | Can support or restrain demand by changing financing costs, credit creation, and risk-taking conditions. |

| Inflation path | Can affect inflation through demand pressure, income support, supply incentives, taxes, subsidies, and fiscal credibility. | Can affect inflation through borrowing costs, demand conditions, inflation expectations, currency pressure, and financial conditions. |

| Typical lag | Depends on political approval, program design, implementation speed, and how quickly households or firms respond. | Depends on central-bank decisions, market pricing, banking transmission, credit demand, and economic sensitivity to rates and liquidity. |

| Market-regime interpretation | Markets may focus on demand support, deficits, issuance, taxes, inflation pressure, growth mix, and central-bank reaction risk. | Markets may focus on yields, discount rates, liquidity, credit spreads, currency effects, and reaction-function expectations. |

| Main limitation | The same fiscal action can have different effects depending on timing, financing, inflation pressure, and private-sector response. | The same monetary action can have different effects depending on credit stress, inflation expectations, banking conditions, and growth risk. |

| Related concept route | Use fiscal impulse when the key issue is the change in fiscal stance over time. | Use central-bank liquidity when the key issue is the liquidity channel rather than the whole monetary-policy framework. |

Why the same macro goal can use different tools

Fiscal and monetary policy can both aim at growth, inflation, employment, or financial stability. The overlap in goals is why the two are often confused. The cleaner classification is not “which goal is being pursued,” but “which authority changed which tool.”

A government tax rebate and a central-bank rate cut can both be used when growth is weakening. They are still different policy types because one changes the budget channel and the other changes financial conditions.

Classification rule: identify the actor first, the tool second, and the first transmission channel third. The macro goal alone is not enough to classify the policy.

Same scenario, different policy label

Weakening-economy scenario: if the government sends households a tax rebate or increases infrastructure spending, the action is fiscal policy because the tool is budget-based. If the central bank cuts the policy rate or adds liquidity through its operations, the action is monetary policy because the tool changes financial conditions. If both happen at the same time, the setting is a policy mix rather than one label replacing the other.

The distinction matters because markets may react to the same growth problem through different channels. Fiscal support may raise attention on deficits, issuance, sector demand, and inflation pressure. Monetary easing may raise attention on yields, discount rates, bank credit, liquidity, and currency effects. Neither reaction is automatic.

Common confusion and boundary cases

| Confusion | Cleaner classification | Why it matters |

|---|---|---|

| Tax cuts are monetary policy because they stimulate demand. | Tax cuts are fiscal policy because the government changes the tax channel. | The economic effect may overlap with monetary easing, but the authority and tool are different. |

| Rate cuts are fiscal policy because they support the economy. | Rate cuts are monetary policy because the central bank changes the cost of money. | The goal may be growth support, but the transmission starts through financial conditions. |

| Government borrowing is monetary policy. | Government borrowing belongs to fiscal stance and financing context. It becomes part of the monetary-policy discussion only when the central bank changes financial conditions through its own tools. | Debt issuance, deficit financing, and central-bank liquidity operations should not be collapsed into one label. |

| Fiscal impulse is the same as fiscal policy. | Fiscal impulse focuses on the change in fiscal stance or budget impact over time. It is narrower than the full fiscal-policy category. | A deficit level alone does not classify the direction or size of the fiscal impulse. |

| Central-bank liquidity is the same as all monetary policy. | Central-bank liquidity is one channel within or near monetary-policy implementation, not the full policy framework. | Liquidity operations, rates, guidance, and credit conditions can matter in different ways. |

| Policy mix means fiscal policy and monetary policy are identical. | Policy mix describes the combined fiscal and monetary setting. | Combined settings can reinforce or offset each other without erasing the distinction between the two policy types. |

How markets interpret the difference

Market interpretation depends on the policy channel, the starting macro regime, and the expected reaction from other policymakers. A fiscal expansion during weak demand can be interpreted differently from the same fiscal expansion during already-high inflation. A monetary easing step during a normal slowdown can be interpreted differently from easing during credit stress.

For market-regime analysis, the useful sequence is: authority, tool, first channel, inflation pressure, growth pressure, yields, liquidity, credit, currency context, and expected reaction from the other side of the policy mix.

Market limitation: fiscal stimulus is not automatically positive for risk assets, and monetary easing does not always mean asset prices rise. The outcome depends on inflation, yields, credit stress, earnings risk, financing conditions, and whether markets read the policy as support, stress response, or credibility risk.

When policy mix matters

Policy mix matters when fiscal and monetary settings point in the same or opposite direction. A government can expand fiscal support while the central bank tightens monetary conditions to fight inflation. A government can reduce fiscal support while the central bank eases to protect credit conditions. The combined setting can matter more than either label in isolation.

Use policy mix when the main question is how fiscal and monetary settings interact. Use the fiscal-versus-monetary distinction when the main question is how to classify a specific tool or headline.

Key limitations

- One is not always faster: fiscal approval, fiscal implementation, monetary transmission, banking conditions, and market expectations can all change timing.

- One is not always stronger: strength depends on inflation regime, credit conditions, household balance sheets, business confidence, and financing constraints.

- Same goal does not mean same tool: both can target growth or inflation, but the classification depends on authority and instrument.

- Same market reaction does not prove same cause: yields, equities, currencies, and credit can move for different reasons under fiscal and monetary shocks.

- Policy labels are not signals: “fiscal” and “monetary” describe policy channels, not buy, sell, bullish, or bearish conclusions.

How to classify a policy headline

A policy headline is easier to classify when the first question is about the tool, not the expected market reaction.

| Question | Fiscal answer | Monetary answer |

|---|---|---|

| Who changed the policy lever? | Government budget authority. | Central bank or monetary authority. |

| What changed first? | Spending, taxes, transfers, borrowing, or fiscal stance. | Rates, liquidity, reserves, credit conditions, or guidance. |

| Where does the impulse enter? | Demand, income, fiscal financing, or public-sector allocation. | Cost of money, credit availability, liquidity, yields, or expectations. |

| What could change the market reading? | Inflation pressure, deficit financing, bond issuance, tax effects, and central-bank response. | Credit stress, inflation expectations, currency pressure, bank transmission, and growth risk. |

| When is it policy mix? | When fiscal and monetary settings are being interpreted together rather than as isolated policy actions. | |