An earnings recession is a sustained decline in aggregate corporate earnings, commonly discussed as two or more quarters of year-over-year earnings or EPS contraction across a broad index, market segment, or corporate sector.

It is an earnings-cycle condition, not a direct label for the whole economy. It can appear without a confirmed economic recession because the contraction is measured through corporate profits, not through the full set of output, income, employment, and production indicators.

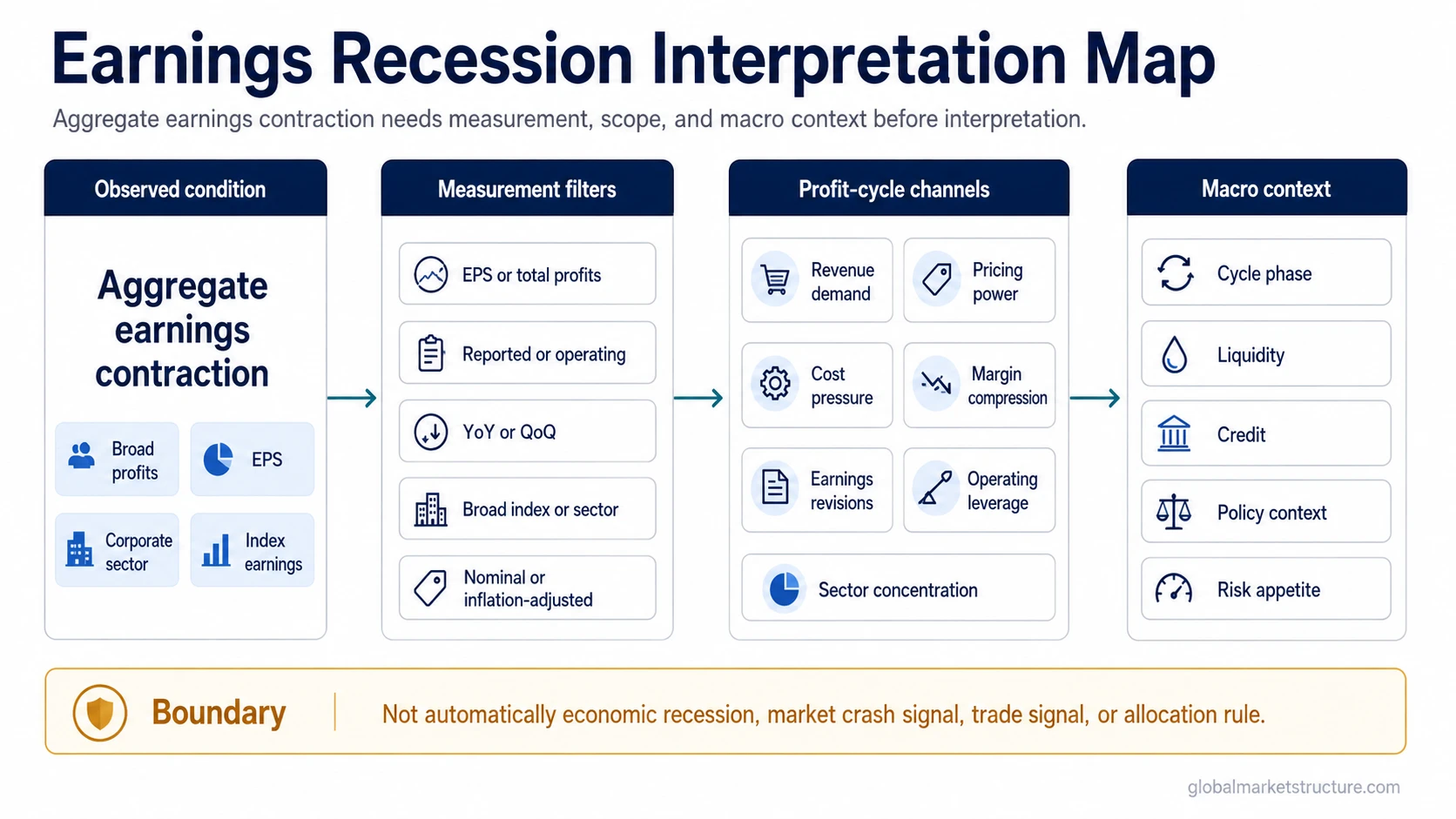

Definition: Earnings recession means broad corporate earnings are contracting for a sustained period. The exact measurement depends on the earnings basis, comparison period, and scope being analyzed.

Key Points

- An earnings recession refers to sustained aggregate earnings decline, not a single company missing estimates.

- It is commonly framed through multi-quarter year-over-year EPS or profit contraction, but the measurement basis matters.

- It is not automatically the same as an economic recession.

- Interpretation depends on margins, revisions, sector concentration, operating leverage, liquidity, credit, and cycle context.

- It should not be treated as a market forecast, crash signal, or allocation rule by itself.

What Is an Earnings Recession?

An earnings recession describes a period when aggregate profits or earnings per share decline across a broad earnings base. The base may be a major equity index, a national corporate sector, or a large group of companies being tracked together.

The word recession can be misleading because it borrows language from economic cycles. In this context, the contraction is in earnings, not necessarily in GDP, employment, industrial activity, or household income.

The concept is useful because earnings link company-level results to broader market interpretation. When aggregate earnings fall, the pressure may come from weaker demand, lower pricing power, rising costs, margin compression, negative revisions, or a mix of those forces.

Earnings Recession vs Economic Recession

An earnings recession and an economic recession can overlap, but they are not the same condition.

Earnings recession: focuses on aggregate corporate profits, EPS, margins, and revisions.

Economic recession: focuses on broad economic activity, such as output, income, employment, consumption, production, and related macro data.

The difference matters because corporate earnings can weaken before, during, or after broader economic activity slows. Earnings can also contract for reasons that do not require a full economic recession, such as margin pressure, sector-specific weakness, inventory adjustment, currency effects, tax effects, or prior-year comparison distortions.

A weak earnings cycle can still influence market interpretation, but it does not prove that the economy is already in recession. The safer reading is narrower: aggregate profits are under pressure, and the cause of that pressure needs to be identified.

Earnings Recession vs Earnings Season

Earnings season is the recurring reporting period when companies publish results. An earnings recession is a broader condition that may become visible across multiple reporting periods.

The distinction is simple: earnings season is a calendar and reporting flow, while earnings recession is a sustained aggregate earnings contraction. A single weak reporting season may contribute to the evidence, but it does not automatically establish a sustained earnings recession.

How an Earnings Recession Is Measured

There is no single measurement format that works in every context. The most common shorthand is a multi-quarter decline in year-over-year earnings or EPS, but the conclusion can change depending on the earnings basis and comparison scope.

| Measurement question | Why it matters | Interpretation risk |

|---|---|---|

| Year-over-year or quarter-over-quarter? | Year-over-year comparison can reduce seasonality, while quarter-over-quarter movement may capture faster turning points. | A short-term drop can look severe without showing a sustained earnings contraction. |

| EPS or total profits? | EPS reflects profit per share, while total profits measure the aggregate profit pool. | Buybacks, share issuance, or index composition changes can affect EPS interpretation. |

| Reported or operating earnings? | Reported earnings include more accounting items, while operating earnings may remove selected one-time effects. | Different earnings bases can produce different recession signals. |

| Broad index or one sector? | A broad index gives a wider earnings-cycle view, while a sector can show concentrated pressure. | Sector weakness can be mistaken for market-wide earnings contraction. |

| Nominal or inflation-adjusted profits? | Nominal earnings can rise even when real profit power is weaker. | Inflation can blur whether companies are improving real earnings capacity. |

Because the measurement basis matters, earnings recession language should be read with its scope attached. A clear statement should identify what earnings series is being measured, which comparison period is used, and whether the decline is broad or concentrated.

What Can Cause an Earnings Recession?

An earnings recession usually reflects pressure somewhere inside the profit cycle. The same earnings decline can have different meanings depending on whether the main driver is demand, margins, costs, financing conditions, sector concentration, or accounting effects.

| Channel | How it can pressure earnings | What to watch conceptually |

|---|---|---|

| Revenue demand | Slower sales growth reduces the top-line base that profits are built on. | Whether weakness is broad or concentrated in a few cyclical areas. |

| Pricing power | Companies may struggle to pass higher costs to customers. | Whether margins fall even when revenue remains stable. |

| Cost pressure | Input, labor, interest, or supply-chain costs can reduce profitability. | Whether costs are temporary, structural, or tied to financing conditions. |

| Margins | Margins compress when expenses rise faster than revenue or pricing power weakens. | Whether profit weakness is mainly a margin problem or a demand problem. |

| Revisions | Analysts may reduce expected earnings as company guidance and macro data weaken. | Whether estimates are still falling or beginning to stabilize. |

| Operating leverage | High fixed-cost businesses can see profits fall faster than revenue when sales slow. | How operating leverage amplifies profit sensitivity. |

| Sector concentration | A few large sectors can dominate the earnings picture for a broad index. | Whether headline earnings weakness reflects the whole market or a concentrated group. |

| Liquidity and credit context | Tighter financing conditions can affect demand, refinancing, investment, and risk appetite. | Whether earnings pressure appears alongside tighter credit, weaker liquidity, or changing policy expectations. |

The important point is not just that earnings are falling. The more useful question is why they are falling and whether the pressure is broad, narrow, temporary, or connected to a deeper macro cycle.

What an Earnings Recession Can and Cannot Tell You

An earnings recession can show that profit conditions have weakened. It can also help identify whether market attention is shifting toward margins, revisions, cost pressure, and cycle sensitivity.

Limitation: An earnings recession is not a standalone market signal. It does not prove an economic recession, predict a market crash, define a market bottom, or determine asset allocation.

Market prices may move before earnings data fully reflect the pressure. Prices may also recover before reported earnings improve if investors believe the worst earnings revisions are already priced. That timing gap is one reason earnings recession analysis must separate observed earnings data from market interpretation.

The signal becomes more meaningful when it is placed beside other conditions, such as margin trends, revision breadth, credit spreads, liquidity conditions, policy expectations, and market breadth. Even then, the interpretation remains conditional rather than automatic.

A Practical Scenario

A broad index reports falling aggregate EPS for several quarters, while GDP remains positive and employment has not clearly contracted. Depending on the earnings basis and comparison period, that can still be described as an earnings recession. It would not automatically mean the economy is in recession.

The same scenario can have different interpretations. If the decline comes mainly from one sector, the signal may be narrower. If profit margins are compressing across many industries and revisions are still falling, the earnings-cycle pressure may be broader. If liquidity and credit conditions are also tightening, the earnings decline may carry more macro significance.

Common False Readings

The most common mistake is treating the phrase earnings recession as if it automatically carries the same meaning as economic recession. It does not.

| False reading | Cleaner interpretation |

|---|---|

| A single company misses earnings, so there is an earnings recession. | An earnings recession requires broad aggregate earnings weakness, not one company result. |

| Two weak quarters always mean the same thing. | The measurement basis, comparison period, and scope must be checked. |

| Earnings recession means economic recession. | Economic activity and corporate earnings are related, but they are not identical measures. |

| Earnings recession is a market crash signal. | It is an earnings-cycle condition. Market interpretation depends on pricing, expectations, liquidity, credit, and breadth. |

| All earnings weakness is equally macro-relevant. | Concentrated sector weakness can mean something different from broad margin compression. |

Related Concepts

Operating leverage helps explain why profits can fall faster than revenue when fixed costs are high or demand softens. Earnings season helps explain when company results are reported and how the reporting cycle reveals changes in expectations.

Together, these concepts separate the mechanics of profit sensitivity from the calendar flow of reported results. Earnings recession sits between them as the broader condition where aggregate earnings decline becomes sustained enough to shape earnings-cycle interpretation.

FAQ

What does earnings recession mean?

Earnings recession means aggregate corporate earnings are declining for a sustained period. It is commonly discussed as two or more quarters of year-over-year earnings or EPS contraction, but the exact definition depends on the earnings basis and scope being measured.

Is an earnings recession the same as an economic recession?

No. An earnings recession focuses on corporate profits, while an economic recession focuses on broad economic activity. The two can overlap, but one does not automatically prove the other.

Can one company have an earnings recession?

A single company can experience an earnings decline, but the term earnings recession is usually used for aggregate earnings across a broad index, market segment, or corporate sector.

Is an earnings recession a stock market signal?

No. It can be relevant for market interpretation, but it is not a standalone forecast, trade signal, or allocation rule. Its meaning depends on margins, revisions, valuation, liquidity, credit, cycle context, and what markets may have already priced.

Why does the measurement basis matter?

The conclusion can change depending on whether the analysis uses EPS or total profits, reported or operating earnings, year-over-year or quarter-over-quarter comparisons, and broad-index or sector-level scope.