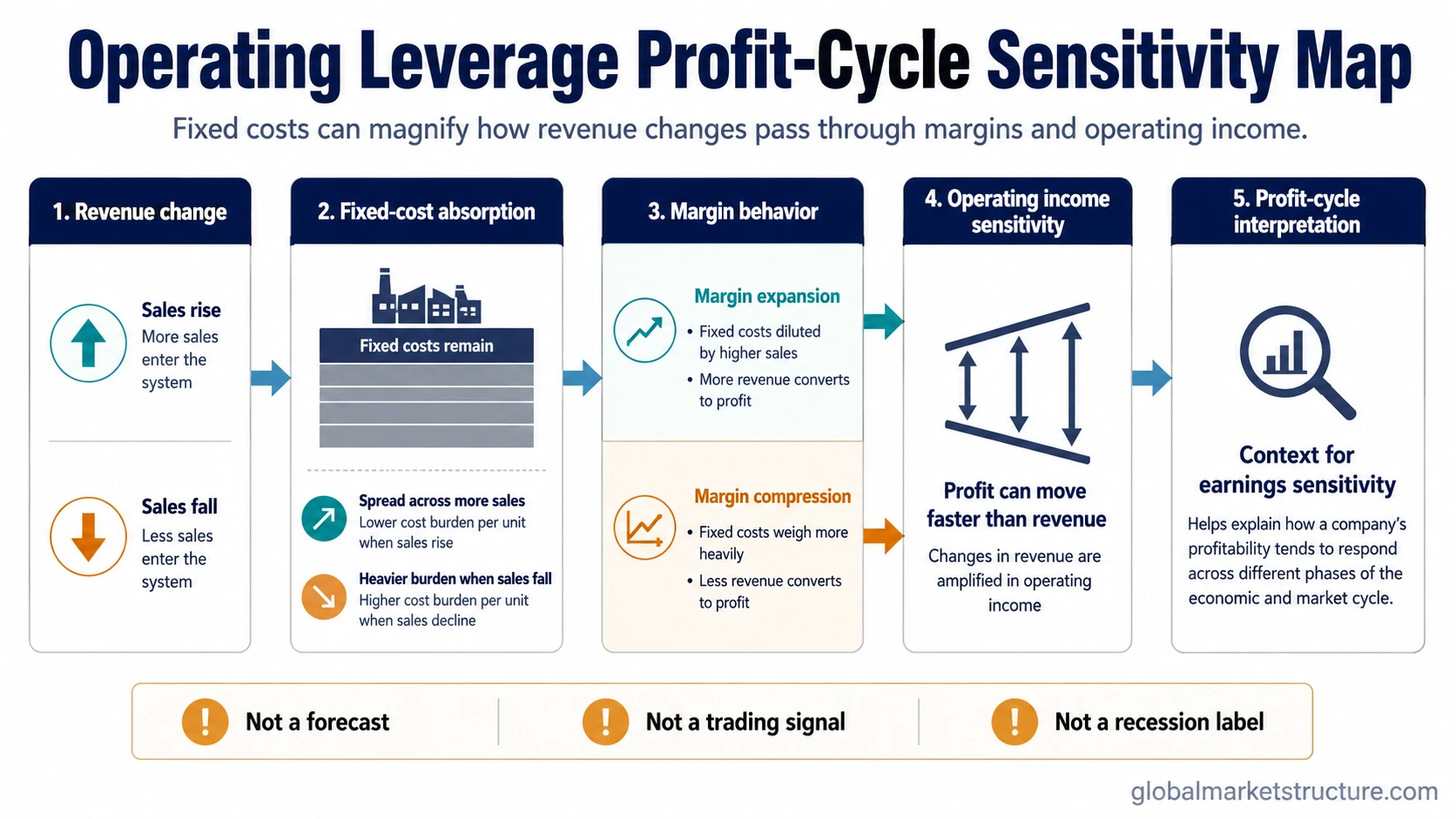

Operating leverage means that operating income is sensitive to revenue changes because part of the cost base is fixed. When revenue rises, fixed costs can be spread across more sales and margins can expand. When revenue falls, the same fixed costs can pressure margins and earnings. It is a profit-cycle sensitivity concept, not a forecast, signal, or recession label.

Operating leverage in simple terms: the higher the fixed-cost share of a business model, the more operating profit can move when revenue changes. The lower the fixed-cost share, the more costs tend to move with sales, which can make operating profit less exposed to each revenue change.

Operating leverage helps explain why the same revenue slowdown can create different earnings effects across business models, industries, and profit-cycle phases.

How operating leverage works

Operating leverage begins with the split between fixed costs and variable costs. Fixed costs do not adjust quickly with sales volume. Variable costs tend to rise or fall more directly with production, service delivery, or sales activity.

| Cost or profit layer | What changes | Why it matters |

|---|---|---|

| Revenue | Sales rise or fall | Revenue is the starting point for the operating leverage effect. |

| Fixed-cost absorption | Fixed costs are spread across more or fewer sales | More sales can dilute fixed costs per unit, while fewer sales can make the fixed-cost burden heavier. |

| Margin behavior | Operating margin expands or compresses | Margins can move faster than revenue when fixed costs are meaningful. |

| Operating income | Profit changes more than sales | Operating income can rise or fall by a larger percentage than revenue. |

| Profit-cycle interpretation | Earnings sensitivity becomes easier to classify | Cost structure helps explain why operating profit sensitivity can change across different revenue and margin conditions. |

Revenue change affects fixed-cost absorption, fixed-cost absorption affects margin expansion or compression, and margin movement changes operating income sensitivity.

Fixed costs, variable costs, and operating income sensitivity

A business with high fixed costs must cover those costs before revenue growth becomes strongly visible in operating income. Once those fixed costs are covered, additional revenue can carry more profit through to operating income because the cost base does not rise at the same pace.

The same mechanism works in reverse. If revenue weakens while fixed costs remain in place, operating income can fall faster than revenue. That is where operating leverage connects to margin compression: weaker sales can meet a cost base that cannot adjust quickly enough.

Practical scenario: a company with heavy fixed infrastructure may look efficient while demand is rising because each extra unit of revenue helps absorb the fixed base. If demand slows, that same fixed base can turn into earnings pressure because rent, depreciation, platform costs, or salaried labor may not decline at the same speed as revenue.

High operating leverage vs low operating leverage

High operating leverage is not automatically good or bad. It describes sensitivity. The same structure that can amplify profit growth during a revenue expansion can also amplify earnings weakness during a revenue decline.

| Type | Cost structure | When revenue rises | When revenue falls |

|---|---|---|---|

| High operating leverage | Higher fixed-cost share | Operating income can rise faster than revenue after fixed costs are absorbed. | Operating income can fall faster than revenue if fixed costs remain in place. |

| Low operating leverage | Higher variable-cost share | Operating income may rise more steadily because costs also move with sales. | Operating income may be less exposed to fixed-cost pressure, but margin expansion can also be more limited. |

The false reading is to treat high operating leverage as a bullish label or a bearish warning by itself. It becomes meaningful only after revenue direction, pricing power, cost flexibility, margin trend, and profit-cycle context are considered together.

Degree of operating leverage

The degree of operating leverage, often shortened to DOL, is a way to estimate how exposed operating income is to a change in revenue. A common expression is:

Degree of operating leverage = percentage change in operating income ÷ percentage change in revenue

If operating income changes much more than revenue, operating leverage is higher. If operating income changes closer to the revenue change, operating leverage is lower.

The formula is useful as a support tool, but it should not replace business interpretation. DOL can vary across time, across revenue levels, and across cost structures. It can also be hard to estimate precisely from public statements when fixed and variable costs are not disclosed in a clean split.

Break-even, contribution margin, and fixed-cost absorption

Operating leverage is closely tied to break-even economics. Before a business covers its fixed costs, revenue growth may not translate into strong operating income. After break-even is reached, each additional unit of revenue can have a larger profit effect if the contribution margin is strong.

Contribution margin matters because it shows how much revenue remains after variable costs. A business with high fixed costs and a healthy contribution margin can experience strong operating income growth after the fixed base is covered. A business with weak contribution margin may not get the same benefit even if fixed costs are meaningful.

Interpretation limit: operating leverage is not visible from fixed costs alone. Pricing, variable costs, demand stability, cost flexibility, and accounting classification can all change the profit effect.

Why operating leverage matters in the profit cycle

Operating leverage matters for profit-cycle interpretation because earnings often move through phases of acceleration, slowdown, pressure, and recovery. Cost structure can help explain why operating income responds more sharply in some phases than in others.

During a revenue upswing, high operating leverage can strengthen profit response when fixed costs are already covered. During a revenue slowdown, it can expose downside amplification because fixed costs remain while sales weaken. At the aggregate level, that sensitivity can matter when analysts, investors, or macro observers are trying to understand whether earnings pressure is broadening.

That connection does not make operating leverage an earnings recession signal. It is one channel through which revenue weakness can become operating income weakness. Aggregate earnings contraction still requires broader evidence across companies, sectors, margins, revisions, and reported results.

Operating leverage vs financial leverage

Operating leverage and financial leverage both describe amplification, but they come from different places.

| Concept | Main driver | What gets amplified | Main confusion to avoid |

|---|---|---|---|

| Operating leverage | Fixed operating costs | Operating income sensitivity to revenue changes | It is about the cost structure of operations, not debt. |

| Financial leverage | Debt and capital structure | Equity return or earnings sensitivity after financing costs | It is about financing structure, not fixed operating costs. |

A business can have high operating leverage without high financial leverage, and a highly indebted business can have modest operating leverage. The distinction matters because operational sensitivity and balance-sheet sensitivity create different risks.

Operating leverage vs profit margins

Profit margins describe profitability at a point in time or over a period. Operating leverage describes how responsive operating income can be when revenue changes. The two are related, but they are not the same concept.

A company can have strong margins and still have low operating leverage if its costs move closely with sales. Another company can have lower current margins but high operating leverage if revenue growth would spread fixed costs across a larger base. The useful distinction is level versus response: margins show where profitability is, while operating leverage helps explain how profitability may react to revenue change.

Can operating leverage be calculated from public financial statements?

Operating leverage can often be estimated, but it is rarely visible with perfect precision from standard public reporting. Financial statements usually separate broad expense categories, not every fixed and variable cost needed for a clean operating leverage model.

Analysts may estimate operating leverage by comparing revenue changes with changes in operating income over time, or by using contribution-margin and break-even assumptions when enough detail is available. Those estimates should stay conditional because accounting classifications, business mix, pricing, restructuring, and one-time items can distort the signal.

Common mistakes when interpreting operating leverage

Mistake 1: treating high operating leverage as automatically bullish. High sensitivity can help when revenue rises, but it can hurt when revenue falls.

Mistake 2: treating operating leverage as a recession signal. It can explain earnings sensitivity, but it does not label the economy or the market cycle by itself.

Mistake 3: treating the DOL formula as full certainty. A formula can summarize past or assumed sensitivity, but real cost behavior can change.

Mistake 4: confusing operating leverage with financial leverage. Operating leverage comes from fixed operating costs. Financial leverage comes from debt and capital structure.

Mistake 5: ignoring revenue quality and pricing power. Fixed-cost absorption matters most when revenue is durable enough and pricing does not deteriorate at the same time.

How operating leverage fits into earnings interpretation

Operating leverage is most useful when it is placed between revenue trends and earnings outcomes. It helps explain why a small change in sales can produce a larger change in operating income, especially when fixed costs are difficult to adjust.

The interpretation becomes stronger when operating leverage is considered alongside margin trend, revenue growth quality, cost flexibility, pricing power, and earnings revisions. It becomes weaker when the analysis relies only on a single formula, a single period, or a broad assumption about fixed costs.

Core limitation: operating leverage is a sensitivity channel. It does not predict stock returns, provide a trading signal, or prove that aggregate earnings are entering contraction. It helps classify how revenue changes may pass through to operating income under a given cost structure.

FAQ

What is operating leverage?

Operating leverage is the sensitivity of operating income to revenue changes caused by fixed operating costs. Higher fixed costs can make operating income rise faster than revenue during growth and fall faster than revenue during weakness.

Is high operating leverage good or bad?

High operating leverage is conditional. It can be beneficial when revenue grows and fixed costs are absorbed, but it can become a weakness when revenue falls and fixed costs remain in place.

What is the degree of operating leverage?

The degree of operating leverage estimates how much operating income changes relative to revenue. A common formula is percentage change in operating income divided by percentage change in revenue.

How is operating leverage different from financial leverage?

Operating leverage comes from fixed operating costs. Financial leverage comes from debt and capital structure. Both can amplify outcomes, but they measure different sources of sensitivity.

Does operating leverage predict stock returns?

No. Operating leverage can help explain profit sensitivity, but it does not predict stock returns or create a trading signal by itself.