DXY, or the U.S. Dollar Index, is a benchmark that measures the U.S. dollar against a fixed basket of major currencies. It rises when the dollar strengthens against that basket and falls when the dollar weakens. The key boundary is narrow but important: DXY is a currency-basket index, not a complete measure of global dollar liquidity, broad trade-weighted dollar strength, or market direction.

Definition: The Dollar Index is a currency-basket benchmark for the U.S. dollar. It compares the dollar with a specific group of foreign currencies rather than measuring every dollar market, every funding channel, or every global trade relationship.

Key Points

- DXY measures the U.S. dollar against a fixed basket of major currencies.

- The euro has the largest influence, so DXY is not a complete global dollar measure.

- DXY can help frame dollar pressure across FX, commodities, rates, and risk conditions.

- DXY needs confirmation from broader dollar, liquidity, rates, credit, and cross-asset evidence.

What the Dollar Index Measures

The Dollar Index measures how the U.S. dollar moves against a defined basket of currencies. A higher DXY reading means the dollar has strengthened against that basket. A lower DXY reading means the dollar has weakened against that basket.

The index gives markets a common reference point for dollar pressure. Its weakness is also its clarity: it answers a narrower benchmark question, not every question about global dollar conditions.

Boundary: DXY is useful for reading dollar movement against its fixed basket. The cause and market meaning of that movement come from surrounding evidence such as rates, liquidity, credit, commodities, and risk appetite.

What Currencies Are in the DXY Basket?

The DXY basket is concentrated in a small group of major currencies. The euro carries the largest weight, which makes the index especially sensitive to EUR/USD movement compared with broader trade-weighted dollar measures.

| Currency | Common DXY weight | Interpretation note |

|---|---|---|

| Euro | 57.6% | Largest influence, so euro movement can dominate the index. |

| Japanese yen | 13.6% | Important developed-market FX component. |

| British pound | 11.9% | Adds another major European currency relationship. |

| Canadian dollar | 9.1% | Connects the basket to a commodity-linked developed-market currency. |

| Swedish krona | 4.2% | Smaller European component. |

| Swiss franc | 3.6% | Smaller safe-haven and European component. |

The basket composition matters because a DXY move can look broad even when one or two large components explain much of the change. A dollar move against emerging-market currencies, commodity-linked currencies outside the basket, or dollar funding channels may not appear cleanly in DXY.

How DXY Is Read in Market-Structure Context

DXY is often used as a reference point for dollar pressure. When DXY rises, dollar strength against its basket can affect FX translation, commodity pricing, and financial conditions for some non-dollar borrowers. When DXY falls, the pressure can ease, but the interpretation still depends on why the dollar is moving.

The driver matters. A rising DXY linked to higher real yields can mean something different from a rising DXY linked to stress demand for dollars. A falling DXY during improving global growth can mean something different from a falling DXY driven by U.S.-specific policy repricing.

Useful cross-checks: DXY becomes more informative when it is checked against rates, credit spreads, commodity behavior, funding conditions, broader dollar indexes, and risk appetite.

What DXY Does Not Measure

DXY answers a specific basket question. It does not replace broader evidence about dollar liquidity, capital flows, funding stress, commodity supply-demand conditions, or the full dollar regime.

| Common overread | Why it is incomplete | Better interpretation |

|---|---|---|

| DXY equals the whole dollar | The index tracks a fixed basket, not every currency pair or funding market. | Use DXY as one dollar benchmark. |

| DXY equals dollar liquidity | Liquidity also depends on funding markets, balance sheets, collateral, credit, and policy channels. | Compare DXY with broader liquidity and funding evidence. |

| DXY proves capital flows | Exchange-rate movement is not the same as a complete capital-flow map. | Treat DXY as price evidence, not full flow evidence. |

| DXY forecasts commodities | Commodity prices can be driven by supply shocks, demand changes, inventories, policy, and positioning. | Use DXY as one pressure input, not a commodity forecast. |

The broader dollar cycle includes phase, persistence, policy context, global growth, liquidity, and cross-asset confirmation. DXY can contribute to that reading, but it cannot replace the broader framework.

DXY vs Broader Dollar Measures

Different dollar measures answer different questions. DXY is a widely followed market benchmark, while Federal Reserve broad, AFE, and EME dollar index families answer broader trade-weighted dollar questions.

| Measure | Main question | What it can clarify | Main limitation |

|---|---|---|---|

| DXY / U.S. Dollar Index | How is the dollar moving against its fixed basket? | Benchmark dollar pressure against major currencies. | Euro-heavy and not a complete dollar-system measure. |

| Federal Reserve dollar index families | How is the dollar moving against broader trade-weighted currency groups? | Broader dollar strength across larger currency sets. | Less likely to match the live DXY quote shown on market dashboards. |

| Dollar liquidity evidence | How easy or difficult is dollar funding? | Funding stress, balance-sheet pressure, collateral strain, and liquidity conditions. | Requires funding and market-depth evidence beyond a currency index. |

| Dollar cycle | Is the dollar in a broader strengthening or weakening phase? | Persistence, regime context, and cross-asset confirmation. | Requires more evidence than DXY direction alone. |

How DXY Connects to Commodities and FX Translation

Many globally traded commodities are quoted in dollars, so a stronger dollar can change pricing pressure for non-dollar buyers. That relationship is conditional. Supply shocks, inventories, demand, policy restrictions, and positioning can dominate the dollar effect.

The relationship between dollar and commodity prices is clearer when DXY is treated as one part of the pricing environment rather than the whole explanation.

Currency movement can also affect imported-price translation. A DXY move gives a broad dollar reference, while fx pass-through explains how exchange-rate changes may move into import prices, local inflation pressure, margins, and policy sensitivity.

Precious metals add another layer. The gold-dollar relationship can be shaped by the dollar, real yields, risk demand, central-bank behavior, and market stress, so DXY should not be treated as the only driver.

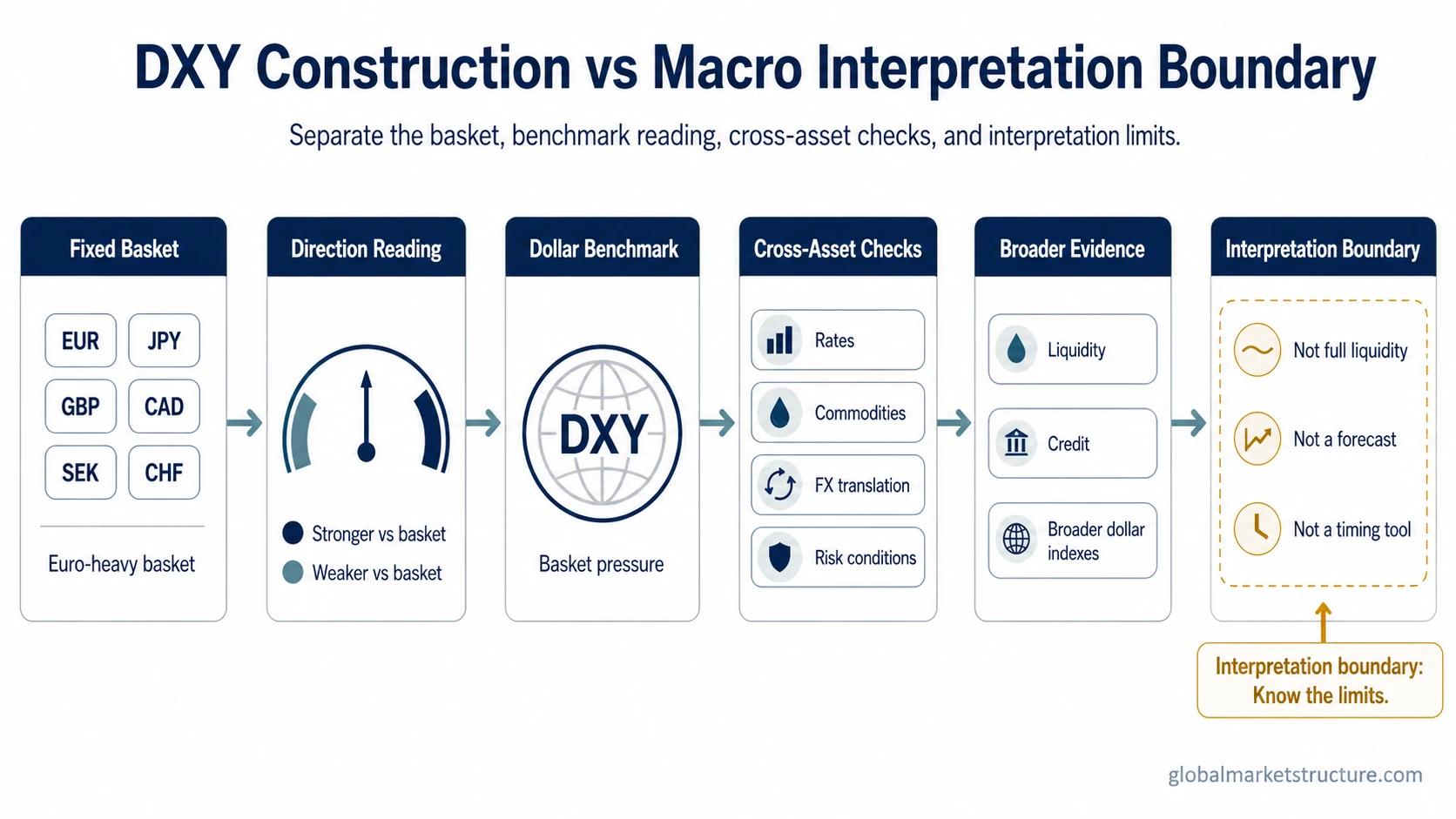

DXY Construction vs Macro Interpretation Boundary

The cleanest use of DXY separates construction from interpretation. Construction tells what the index measures. Interpretation asks what the move may mean across markets.

| Layer | Question | Useful evidence | Boundary |

|---|---|---|---|

| Index construction | Which currencies drive the index? | Basket composition, weights, and direction logic. | Explains the index, not the whole dollar system. |

| Dollar benchmark | Is the dollar strengthening or weakening against the basket? | DXY direction and persistence. | Does not prove the cause of the move. |

| Cross-asset pressure | Are commodities, FX translation, rates, or risk assets responding? | Commodity behavior, yields, credit, FX pairs, and risk appetite. | Requires confirmation outside DXY. |

| Macro regime interpretation | Does the move fit a broader dollar environment? | Liquidity, policy, rates, credit, global growth, and positioning. | DXY is an input, not a complete regime model. |

Example of a Basic DXY Reading

DXY strengthens while several dollar-priced commodities weaken and non-dollar currencies lose ground. The first read is that dollar pressure may be affecting cross-asset pricing. That reading remains incomplete if the commodity move is driven by a supply shock, if rates are rising because growth expectations improved, or if broader dollar funding evidence does not confirm tighter liquidity.

If broader dollar indexes or funding indicators do not confirm the move, the reading should stay narrower and DXY-specific. Stronger interpretation requires alignment across rates, credit conditions, commodity-specific evidence, liquidity measures, and risk appetite.

FAQ

Is DXY the same as the U.S. dollar?

No. DXY is a benchmark for the dollar against a fixed currency basket. The U.S. dollar is broader than one index and includes many currency pairs, funding markets, payment channels, and liquidity conditions.

Why does the euro matter so much in DXY?

The euro has the largest basket weight, so euro-dollar movement can have an outsized effect on the index. That concentration is one reason DXY should not be treated as a complete global dollar measure.

Does a rising DXY always hurt commodities?

No. A rising DXY can create pressure around dollar-priced commodities, but commodity prices can also be driven by supply shocks, demand conditions, inventories, policy changes, and positioning.

Is DXY the same as a Federal Reserve broad dollar index?

No. DXY is a fixed currency-basket market benchmark. Federal Reserve broad, AFE, and EME dollar index families are broader trade-weighted measures and answer different dollar-strength questions.