The gold dollar relationship is often inverse because gold is priced in U.S. dollars and dollar strength changes global purchasing power. The relationship is conditional, not mechanical. Real yields, defensive demand, inflation expectations, policy expectations, and reserve behavior can weaken or reverse the usual pattern.

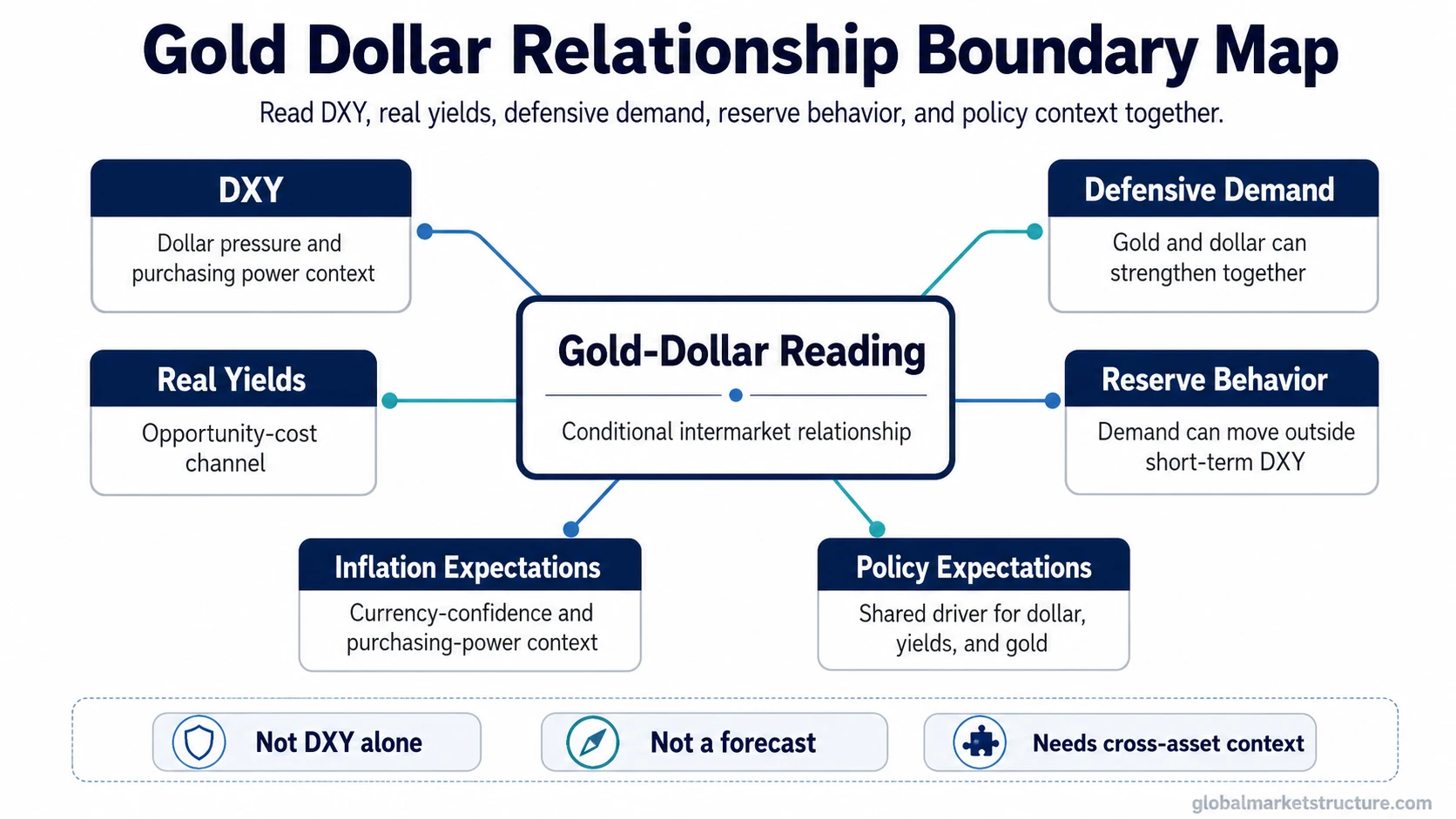

Definition: The gold dollar relationship describes how gold and the U.S. dollar interact inside a broader intermarket framework. It connects a dollar-priced precious metal with the dollar benchmark, real interest rates, inflation expectations, defensive demand, and reserve behavior.

The common reading is straightforward: when the dollar strengthens, gold can face pressure because it becomes more expensive in other currencies and because dollar strength often appears alongside tighter monetary or liquidity conditions. That reading becomes incomplete when another macro force dominates the dollar effect.

Key Points

- Gold and the dollar often move in opposite directions, but the relationship is a tendency rather than a fixed rule.

- DXY is useful for reading dollar pressure, but it is not a complete model for gold behavior.

- Real yields can change the interpretation because gold has no coupon and reacts to opportunity-cost pressure.

- Defensive demand, inflation expectations, policy expectations, and reserve behavior can override a simple dollar reading.

Why Gold and the Dollar Often Move in Opposite Directions

Gold is quoted globally in U.S. dollars. When the dollar strengthens, buyers using other currencies need more local currency to acquire the same ounce of gold. That pricing channel can reduce demand at the margin and can make gold appear inversely related to the dollar.

The DXY Index helps track dollar strength against a fixed currency basket. It can clarify whether a gold move is happening with or against broad dollar pressure, but it does not capture every force affecting gold.

The inverse relationship is most useful when dollar strength appears together with higher real yields, firmer policy expectations, and reduced defensive demand. In that environment, gold can face pressure from both the currency channel and the opportunity-cost channel.

What Changes the Gold Dollar Relationship

The relationship changes when gold is being driven by more than the dollar quotation effect. The main question is whether the dollar move is aligned with real yields, risk demand, policy expectations, inflation expectations, and reserve behavior.

| Driver | How it affects the reading | Main limitation |

|---|---|---|

| Real yields | Higher real yields can raise the opportunity cost of holding gold, while falling real yields can support gold even when the dollar is firm. | Nominal yields alone can mislead if inflation expectations are moving at the same time. |

| Defensive demand | Gold and the dollar can both attract demand during stress because both may be treated as defensive assets in different ways. | Parallel strength does not identify one cause by itself. |

| Inflation expectations | Gold can respond to currency-confidence and purchasing-power concerns when inflation expectations shift. | Inflation pressure does not automatically dominate real-yield pressure. |

| Policy expectations | Expected changes in monetary policy can influence the dollar, real yields, and gold at the same time. | The same policy expectation can affect gold through more than one channel. |

| Reserve behavior | Reserve-related demand can affect gold independently of short-term dollar movement. | Concrete claims about purchase levels need current, reliable source support before publication. |

Gold Dollar Conditions, Implications and Limits

A stronger reading separates the dollar move from the macro condition around it. The same DXY move can mean different things depending on real yields, stress demand, inflation expectations, and reserve behavior.

| Condition | Possible implication | Interpretation limit |

|---|---|---|

| Dollar rises and real yields rise | Gold may face both currency pressure and opportunity-cost pressure. | The reading is weaker if defensive or reserve-related demand is rising at the same time. |

| Dollar rises and stress demand rises | Gold and the dollar may both strengthen as defensive demand increases. | Parallel movement does not prove a single stress regime without confirmation from other markets. |

| Dollar falls and real yields fall | Gold may receive support from both easier dollar pressure and lower opportunity cost. | The move can still fade if inflation expectations, liquidity, or risk appetite shift in the opposite direction. |

| Dollar is flat while inflation expectations shift | Gold can move even without a strong DXY move because the measuring unit is only one part of the setup. | A flat dollar does not mean the gold backdrop is unchanged. |

| DXY conflicts with gold behavior | Another macro driver may be dominating the simple dollar-pressure model. | The conflict needs cross-asset confirmation before the relationship receives a strong interpretation. |

Common False Reading: DXY Alone

Common mistake: A stronger DXY reading does not mean gold must fall. DXY measures dollar strength against a currency basket, while gold also responds to real yields, defensive demand, inflation expectations, policy expectations, and reserve behavior.

Example: DXY strengthens while gold does not fall. A simple dollar-pressure model would expect gold weakness, but the reading changes if real yields are falling, stress demand is rising, or reserve-related demand is absorbing supply. The diagnostic step is to compare the dollar move with the surrounding macro conditions instead of treating the dollar benchmark as the whole explanation.

The Dollar Cycle adds broader regime context because a short dollar move can mean something different from a multi-phase dollar tightening or weakening environment.

How to Interpret the Gold Dollar Relationship Without Overreading It

The gold dollar relationship works best as one intermarket input. It can help classify whether gold is moving with dollar pressure, against dollar pressure, or outside the simple dollar framework.

Limitation: Gold is not only a dollar trade. A gold move may reflect metal demand, currency confidence, real-yield pressure, inflation expectations, policy expectations, stress demand, or reserve behavior. A stronger reading comes from separating those drivers rather than forcing every gold move into a single dollar explanation.

Gold also sits inside the broader category of real assets, where inflation expectations, currency confidence, commodity behavior, and regime shifts can all affect interpretation.

Related Concepts

- DXY Index: DXY provides the dollar benchmark behind many gold-dollar discussions.

- Dollar Cycle: The dollar cycle separates temporary dollar moves from broader dollar regime phases.

- Real Assets: Real-asset context helps when gold behavior is shaped by inflation expectations, currency confidence, or commodity-linked regime shifts.

FAQ

Is the gold dollar relationship usually inverse?

Gold and the U.S. dollar often move inversely because gold is priced in dollars and dollar strength changes global purchasing power. The relationship can break when real yields, stress demand, policy expectations, inflation expectations, or reserve behavior dominate.

Can gold and the dollar rise together?

Gold and the dollar can rise together when defensive demand affects both markets or when another gold driver offsets dollar pressure. Parallel strength needs broader cross-asset context before it receives a strong interpretation.

Is DXY enough to explain gold?

DXY is useful for reading dollar pressure, but it is not enough by itself. Gold also reacts to real yields, inflation expectations, defensive demand, policy expectations, and reserve behavior.

Why do real yields matter for gold?

Real yields matter because gold does not pay interest. When real yields rise, the opportunity cost of holding gold can increase. When real yields fall, that pressure can ease even if the dollar backdrop is mixed.