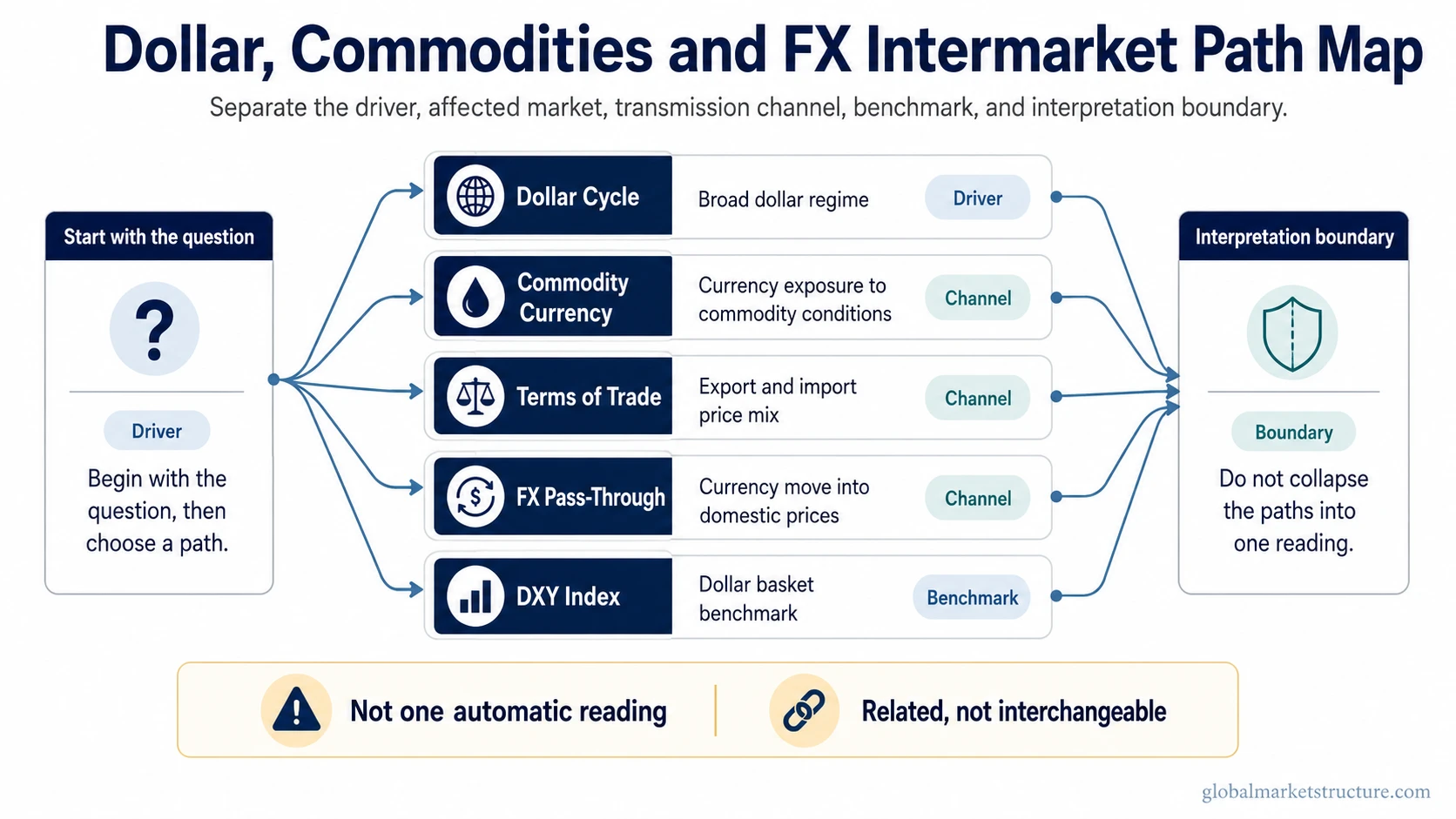

Dollar, commodities, and FX relationships split into different intermarket questions. A broad dollar phase, a commodity-price move, a commodity-linked currency move, a terms-of-trade shift, an FX pass-through channel, and a DXY reading can be connected, but they do not answer the same question. The safest reading starts by separating the driver, the affected market, the transmission channel, and the benchmark before drawing any macro interpretation.

| Question | Best concept path | Why it fits | What not to infer |

|---|---|---|---|

| Is a broad dollar phase affecting several asset classes? | Dollar Cycle | Fits questions about dollar regimes, cross-asset pressure, liquidity conditions, and broader financial conditions. | A dollar phase is not a complete forecast for every commodity, currency, or risk asset. |

| Are commodity-linked currencies reacting to commodity exposure? | Commodity Currency | Fits questions about currencies tied to commodity exposure, export mix, domestic conditions, rates, and risk appetite. | A commodity currency is not a simple one-for-one proxy for a commodity chart. |

| How do export and import prices affect an economy’s external position? | Terms of Trade | Fits questions about the relationship between export prices, import prices, income effects, and external balance pressure. | Terms of trade are broader than one spot commodity price. |

| How can exchange-rate changes affect domestic prices? | FX Pass-Through | Fits questions about currency moves passing into import prices, producer costs, consumer prices, or inflation pressure. | FX pass-through is not immediate, complete, or uniform across economies. |

| Which dollar benchmark is being used as the reference point? | DXY Index | Fits questions about the U.S. Dollar Index as a benchmark for dollar strength against a currency basket. | DXY is not the same as global dollar liquidity or cross-border funding stress. |

How the Five Paths Differ

Dollar Cycle belongs to broad dollar-regime questions. Commodity Currency belongs to currency exposure questions. Terms of Trade belongs to export-versus-import price questions. FX Pass-Through belongs to pricing-transmission questions. DXY Index belongs to benchmark questions.

The concepts can overlap during the same macro episode, but the interpretation changes when the driver changes. A stronger dollar benchmark, a weaker commodity-linked currency, a shift in trade prices, and a change in import-price pressure may point to related stress, but each one describes a different part of the intermarket chain.

False-Reading Boundaries

- A stronger dollar does not automatically mean every commodity must fall.

- A commodity rally does not automatically mean commodity-linked currencies must strengthen.

- DXY is a currency-basket benchmark, not a complete measure of global dollar liquidity.

- Terms of trade are broader than a single commodity price.

- FX pass-through can vary by economy, sector, policy setting, and time horizon.

- Commodity-linked currencies also depend on rates, domestic policy, capital flows, growth expectations, and risk appetite.

Simple Intermarket Scenario

A commodity exporter can face several signals at once: its main export commodity rises, its currency weakens, DXY strengthens, and import costs move higher. That combination should not be compressed into one conclusion. The commodity move belongs to the commodity-price relationship, the currency move belongs to the commodity-currency path, the export/import price mix belongs to terms of trade, and any domestic price effect belongs to FX pass-through.

Related Secondary Paths

Gold-dollar questions belong closer to the gold-dollar relationship and real-yields-and-gold paths. Dollar-and-commodity-price questions belong closer to the dollar-and-commodity-prices path. Broad benchmark questions belong closer to DXY Index, while broader dollar-regime questions belong closer to Dollar Cycle.