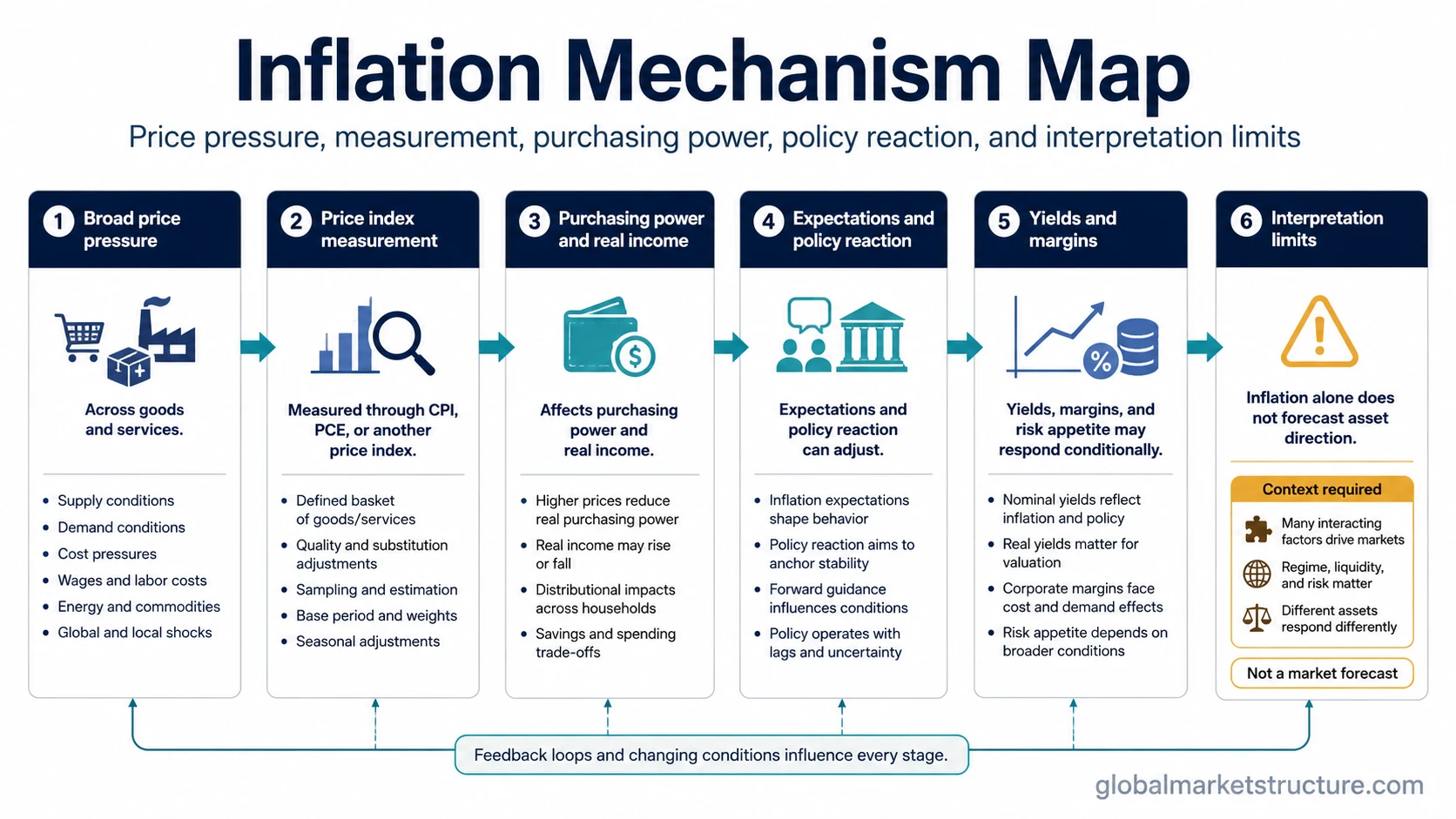

Inflation means a broad rise in the overall price level of goods and services over time, usually measured as the percentage change in a price index such as CPI. It is not the same as one item becoming more expensive. For market interpretation, inflation is a macro driver that can affect purchasing power, real income, policy reaction, yields, margins, and expectations, but the inflation label alone does not predict asset direction.

Short definition: Inflation is a sustained increase in the general price level, measured over time through a price index.

Measurement idea: The inflation rate is usually expressed as a percentage change from one period to another.

Market boundary: Inflation can change the macro backdrop, but it is not a standalone forecast for equities, bonds, earnings, recession risk, or central-bank policy.

What Inflation Is and Is Not

Inflation describes a broad price-level process, not every isolated price change. A single rent increase, fuel spike, or product shortage can affect households, but it becomes part of inflation only when it contributes to a wider and measurable rise in the overall price level.

| Concept | Correct interpretation | Common mistake |

|---|---|---|

| Inflation | Broad increase in the overall price level over time. | Treating one expensive item as proof of economy-wide inflation. |

| Inflation rate | Percentage change in a price index over a defined period. | Reading the index level and the inflation rate as the same thing. |

| Single price increase | A relative price change that may or may not affect broad inflation. | Assuming every price increase reflects general inflation pressure. |

| Falling inflation | A slower rate of price increase when inflation remains positive. | Confusing slower inflation with falling prices. |

| Market signal | A macro input that requires context from growth, policy, yields, margins, and expectations. | Using inflation alone as a market forecast. |

How Inflation Is Measured

Inflation is usually measured with a price index that tracks how the cost of a basket of goods and services changes over time. CPI is one of the most common inflation measures because it focuses on prices paid by consumers, but CPI is not the entire concept of inflation.

Measurement boundary: Inflation is the broad price-level change. CPI is one major way to measure it. Other inflation measures can answer different questions depending on the price universe, weighting method, and economic activity being measured.

Headline inflation usually includes the full basket used by the measure. Core inflation typically removes selected volatile categories, often food and energy, to make underlying price pressure easier to interpret. Core inflation can be useful for analysis, but it is not automatically the “true” inflation rate. Headline inflation still matters because households experience the full cost of living.

| Measure or label | Main use | Interpretation limit |

|---|---|---|

| CPI inflation | Tracks consumer-price changes across a defined basket. | Does not capture every possible price experience for every household. |

| PCE inflation | Tracks price changes tied to personal consumption expenditures. | May behave differently from CPI because of different weighting and methodology. |

| GDP deflator | Tracks broad price changes across domestically produced output. | Not the same as a household consumer-price measure. |

| Headline inflation | Captures the full measured basket. | Can be moved by volatile categories. |

| Core inflation | Filters selected volatile categories to study underlying pressure. | Should not be treated as the only inflation reality. |

Current inflation readings should be checked through dated official statistical releases or official data tools because live values, calculator outputs, and nowcasts change over time.

What Causes Inflation

Inflation can come from several mechanisms. Demand pressure can rise when spending grows faster than available supply. Cost pressure can rise when inputs, wages, energy, shipping, or production constraints increase the cost of supplying goods and services. Expectations can also matter because firms, workers, and consumers may adjust prices, wages, and contracts based on what they believe future inflation will look like.

The distinction between cost pressure and demand pressure is important because the same inflation rate can come from different economic conditions. A demand-led inflation environment can imply a different macro backdrop from one driven mainly by supply constraints, which is why cost-push vs demand-pull inflation separates input-cost pressure from spending-led pressure.

| Inflation mechanism | How it can appear | Why context matters |

|---|---|---|

| Demand-pull pressure | Spending demand rises faster than supply capacity. | May reflect strong demand, constrained supply, or both. |

| Cost-push pressure | Production or input costs rise and pass through into prices. | Can pressure margins if firms cannot pass costs through fully. |

| Expectations | Price and wage decisions adjust to expected future inflation. | Can make inflation harder to cool if expectations become embedded. |

| Policy and monetary conditions | Credit conditions, liquidity, and policy settings can affect demand and pricing behavior. | Policy reaction is not automatic; central banks respond to the full macro picture. |

Why Inflation Matters for Market Structure

Inflation matters because it changes the real value of money, income, cash flows, and expected returns. When prices rise faster than wages or income, purchasing power can weaken. When inflation changes the expected path of policy rates, bond yields and discount rates can move. When input costs rise faster than selling prices, margins can come under pressure.

For market-structure analysis, inflation is best treated as one input inside a wider regime. Its meaning can change depending on growth, labor markets, credit conditions, liquidity, real yields, earnings quality, fiscal conditions, and expectations. The same inflation reading can be interpreted differently in a strong-growth environment, a supply-shock environment, or a weakening-demand environment.

Market interpretation limit: Inflation alone does not prove recession risk, guarantee rate hikes, predict equity direction, predict bond direction, or define earnings outcomes. It becomes more useful when paired with the reason inflation is moving, whether it is broad or narrow, whether it is persistent, and how policy and markets are already priced.

Practical Scenario: Same Inflation Rate, Different Meaning

A practical scenario is that two economies report the same inflation rate. In one case, wage growth, demand, and credit conditions remain firm, while margins are stable. In another case, inflation is driven mainly by supply costs while demand weakens and margins compress.

The number can look similar, but the market interpretation may differ. The first setting may point toward demand strength and policy sensitivity. The second may point toward cost pressure, weaker real income, and margin risk. The inflation rate is the starting point, not the full conclusion.

Common False Readings

Inflation becomes misleading when the label replaces the analysis. A high inflation rate, a falling inflation rate, or a sticky inflation reading can each mean different things depending on cause, breadth, persistence, and market pricing.

| False reading | Safer interpretation |

|---|---|

| Inflation means recession is coming. | Inflation can raise recession risk under some conditions, but growth, credit, labor markets, and policy response must also be assessed. |

| Inflation guarantees rate hikes. | Policy reaction depends on inflation, employment, financial conditions, expectations, and the policy framework. |

| Inflation means stocks must fall. | Equity response can depend on margins, nominal growth, real yields, sector mix, valuation, and policy expectations. |

| Inflation means bonds must fall. | Bond response can depend on expected policy, real yields, growth risk, term premium, and whether inflation is already priced. |

| Falling inflation is always bullish. | Falling inflation can be constructive in some settings, but it can also reflect weakening demand or tighter financial conditions. |

| Lower inflation equals deflation. | Lower positive inflation is not deflation. Deflation means broad falling prices. |

Inflation vs Related Labels

Several inflation labels describe nearby but different ideas. Keeping the labels separate helps prevent one measure from absorbing the meaning of the entire inflation cycle.

| Label | Meaning | Boundary |

|---|---|---|

| Inflation | Broad rise in the overall price level over time. | A broad price-level concept, not a current-rate reading or market forecast. |

| Disinflation | Inflation is slowing while the inflation rate remains positive. | Prices may still be rising, just more slowly. |

| Deflation | Broad decline in the overall price level. | Not the same as lower positive inflation. |

| Sticky inflation | Inflation remains slow to decline. | Useful for persistence risk, not a standalone policy forecast. |

| Inflation persistence | Durability of inflation pressure over time. | Focuses on how long pressure lasts, not only the current rate. |

| Breakeven inflation | Market-implied inflation compensation derived from nominal and inflation-linked bonds. | Not the same as realized CPI inflation. |

| Stagflation | Inflation paired with weak growth or stagnation. | Not every inflation episode is stagflation. |

FAQ

Is inflation just prices going up?

Inflation is broader than one price going up. It refers to a general rise in the overall price level across goods and services over time.

Is lower inflation the same as deflation?

No. Lower positive inflation means prices are still rising, but at a slower rate. Deflation means the overall price level is falling.

Is CPI the same as inflation?

CPI is one major way to measure inflation, especially consumer-price inflation. Inflation is the broader concept of price-level change over time.

Does inflation predict market direction?

No. Inflation can affect policy expectations, yields, margins, purchasing power, and risk appetite, but it does not predict asset direction by itself.