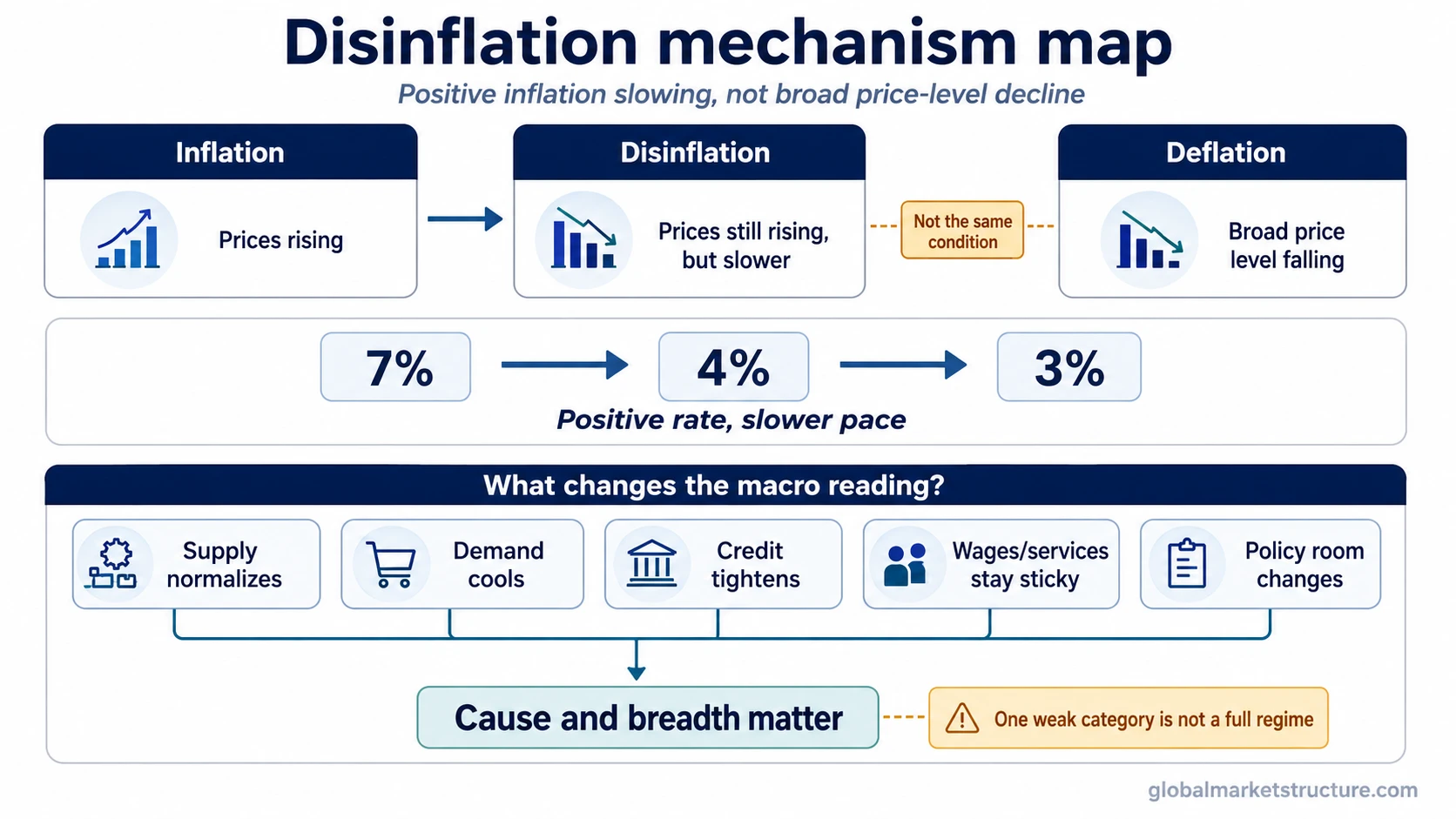

Disinflation is a slowdown in the rate of inflation, not a fall in the overall price level. Prices can still be rising, but rising more slowly than before. That makes disinflation different from deflation, where the broad price level is declining.

The macro meaning changes with the source of the slowdown. Supply normalization can reduce price pressure without signaling broad weakness. Demand cooling, tighter credit, or falling nominal-income growth can point to a weaker growth backdrop even when the inflation rate is improving.

Disinflation definition

Disinflation means inflation is still positive but slowing. If inflation falls from 6% to 4%, prices are still rising, but the pace of increase has slowed. The inflation rate has declined, while the price level has not necessarily fallen.

This distinction matters because inflation describes the rate at which prices rise, while disinflation describes a decline in that rate. Deflation describes broad price-level decline. Those are different macro conditions, even though they are often confused in market commentary.

Disinflation vs inflation vs deflation

| Concept | What is happening | Simple reading | Main confusion to avoid |

|---|---|---|---|

| Inflation | The general price level is rising. | Prices are increasing over time. | Inflation can be high, low, rising, or falling. |

| Disinflation | The inflation rate is slowing. | Prices may still be rising, but more slowly. | Disinflation is not the same as falling prices. |

| Deflation | The broad price level is declining. | Prices are falling across the economy or a broad price basket. | A lower inflation rate is not automatically deflation. |

The closest boundary is between slower inflation and falling prices, which is why disinflation vs deflation is the most important comparison in this cluster.

A simple positive-inflation example

Suppose a broad inflation measure rises 7% one year and 3% the next year. The second year still has inflation because prices are rising. It is also disinflation because the rate of increase has slowed from 7% to 3%.

The same logic applies when price pressure eases but does not turn negative. Consumers may still face higher prices than before, firms may still have rising input costs, and policy authorities may still view inflation as too persistent. Disinflation only says the pace is cooling.

How disinflation is usually observed

Disinflation is usually identified through inflation measures and the components behind them. The useful question is not only whether one monthly or category-level number declined, but whether price pressure is cooling broadly enough and persistently enough to change the inflation trend.

| Observable channel | What it can suggest | Limit to keep in view |

|---|---|---|

| Headline inflation | Broad price growth may be slowing. | Energy, food, or other volatile components can move the headline rate sharply. |

| Core inflation | Underlying price pressure may be cooling. | Core measures still need context from services, wages, rents, and demand. |

| Goods prices | Supply chains, inventories, or input costs may be normalizing. | Goods disinflation alone does not prove broad economy-wide disinflation. |

| Services inflation | Domestic cost pressure may be easing or staying sticky. | Services can remain firm even when goods prices cool. |

| Wage growth | Labor-cost pressure may be changing. | Wages can support demand and margins differently across sectors. |

| Credit conditions | Demand may be weakening as financing becomes harder or more expensive. | Tighter credit can reduce inflation pressure while also raising growth risk. |

No single indicator proves a complete disinflation regime. Breadth, persistence, and the cause of the slowdown matter more than one isolated print or one weak category.

Why disinflation happens

Disinflation can come from several channels. The same inflation slowdown can therefore carry different macro meanings when the pressure is easing because supply is improving, demand is weakening, policy is restrictive, or credit is tightening.

Demand cooling: Slower household spending, weaker business activity, or less pricing power can reduce the pace of price increases. This form of disinflation can be helpful if inflation pressure falls without major growth damage, but it becomes more concerning when it reflects falling demand, rising unemployment risk, or weaker nominal income.

Supply normalization: Better supply chains, lower input costs, more available inventory, or easing commodity pressure can slow inflation without necessarily pointing to weak demand. This version can feel more benign because it reduces cost pressure while leaving activity more intact.

Restrictive policy: Higher rates, tighter liquidity, and slower credit creation can reduce inflation pressure by cooling demand and financial conditions. The key question is whether policy is slowing inflation in a controlled way or pushing growth and credit conditions toward stress.

Wage and services dynamics: Inflation can slow in goods while wage-sensitive services remain sticky. In that case, headline disinflation may look cleaner than the underlying inflation problem.

Why the growth-inflation mix matters

Disinflation is not automatically good or bad for markets. A slower inflation rate can reduce pressure on consumers, margins, yields, and monetary policy. It can also signal weaker demand if firms are losing pricing power because activity is slowing.

The key distinction is whether inflation is slowing faster than growth is deteriorating. When inflation pressure cools while employment, spending, credit availability, and earnings conditions remain resilient, disinflation can look like relief. When inflation cools because demand is breaking down or credit is tightening, the same headline trend can point to a weaker macro backdrop.

| Disinflation context | Macro interpretation | Why it matters |

|---|---|---|

| Supply improves while demand holds | Inflation pressure cools with less growth damage. | Policy pressure may ease without the same recession signal. |

| Demand weakens sharply | Inflation slows because spending and pricing power are fading. | Growth, earnings, and credit risk can become more important than inflation relief. |

| Goods cool but services stay sticky | Headline improvement may hide persistent domestic pressure. | Policy may remain cautious even if the headline rate improves. |

| Credit tightens while inflation slows | Disinflation may reflect financial restraint and weaker demand. | Lower inflation can arrive with tighter lending and higher refinancing stress. |

Disinflation does not automatically mean a policy pivot

A slowing inflation rate can reduce pressure on policy authorities, but it does not automatically force easier policy. Policy may still respond to the level of inflation, inflation expectations, wage pressure, services inflation, labor-market strength, financial conditions, and the risk that inflation re-accelerates.

The policy reading also changes with the reason for disinflation. Supply-driven disinflation can create more room for patience. Demand-driven disinflation can arrive with growth stress. Sticky services or wage pressure can keep policy restrictive even while headline inflation improves.

Market interpretation depends on cause, not the label

Markets can react differently to the same inflation slowdown because the surrounding conditions change the signal. Disinflation with resilient growth can support the view that inflation pressure is easing without a sharp activity break. Disinflation with deteriorating credit, weak breadth, falling margins, or weakening labor demand can carry a more defensive message.

The label matters less than the mix behind it: growth, inflation, liquidity, wages, margins, credit, and policy reaction. Lower inflation can reduce one pressure point while exposing another. That is why disinflation should be read as part of the broader macro regime, not as a standalone market direction signal.

Practical scenario: goods cool, services stay sticky

A common disinflation setup is that goods inflation cools as supply chains improve, inventories normalize, or commodity pressure eases. At the same time, services prices and wage-sensitive categories may remain firmer because domestic demand and labor costs have not cooled as much.

In that scenario, the headline inflation rate can slow, but the underlying policy question remains unresolved. The economy may be experiencing real disinflation, yet the persistence of services or wage pressure can keep policy interpretation cautious.

Common false readings of disinflation

Disinflation is not deflation. Prices can still rise during disinflation if the inflation rate remains positive.

Disinflation is not one-sector discounting. A price cut in one category, one industry, or one product group does not automatically mean broad inflation pressure is cooling.

Disinflation is not a confirmed recession signal. It can come from weaker demand, but it can also come from supply normalization or easing input costs.

Disinflation is not a guaranteed policy-pivot signal. Policy can remain restrictive if inflation is still persistent, services pressure is sticky, labor conditions remain firm, or financial conditions do not justify easier settings.

Disinflation is not a buy or sell signal. It is an inflation-dynamics condition that needs growth, credit, liquidity, wage, margin, and policy context before any market interpretation is defensible.

Related inflation-dynamics concepts

Inflation is the broader concept for rising price levels over time. Disinflation is the slowing of that inflation rate. Deflation is the separate condition where the broad price level falls.

The most important comparison is the boundary between disinflation and deflation, because confusing the two can lead to a wrong reading of prices, policy, and macro risk.