Deflation is a sustained fall in the general price level across the economy, usually shown as negative inflation. It is different from disinflation, where prices are still rising but the inflation rate is slowing.

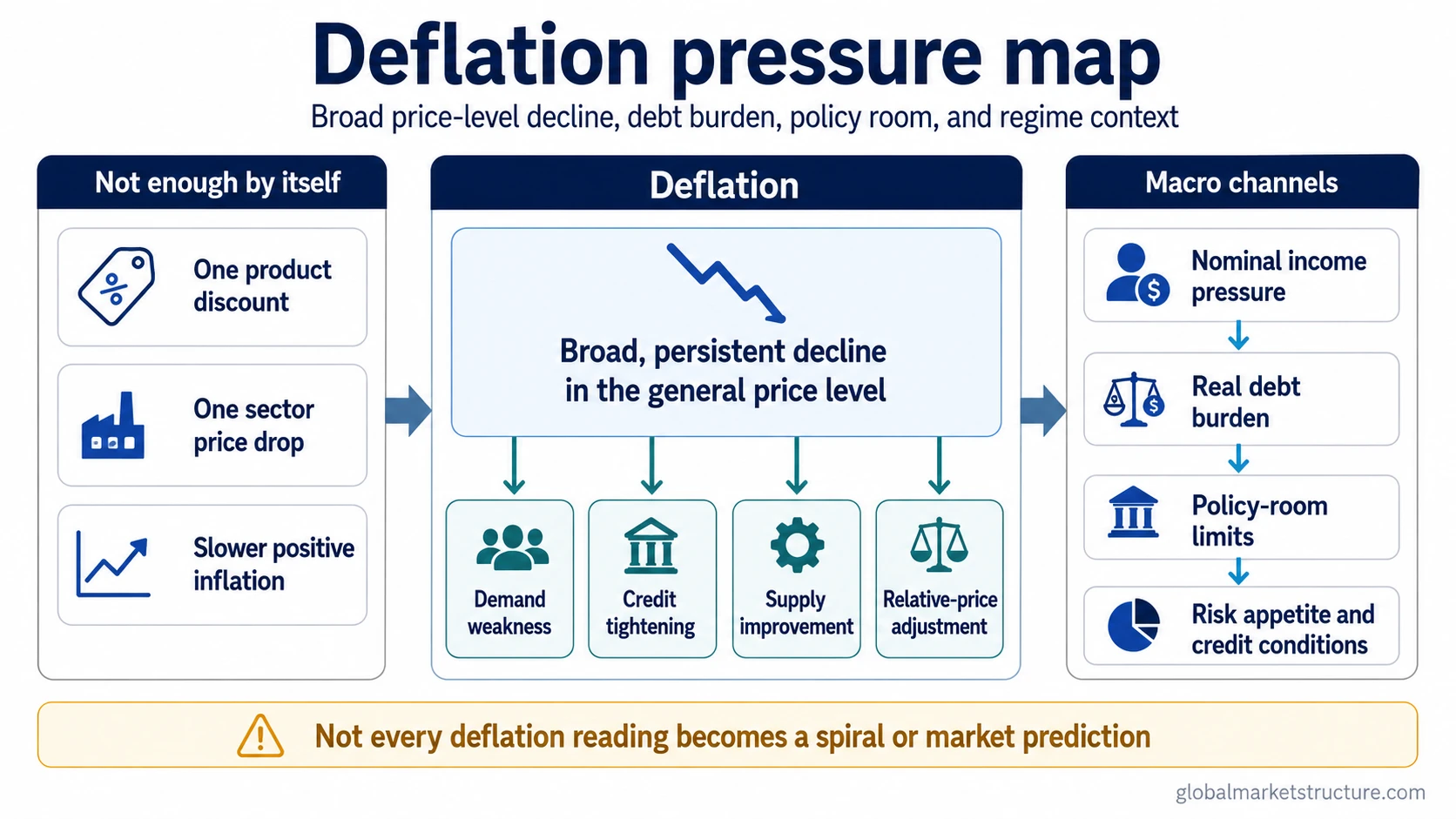

Lower prices in one product, one sector, or one short discount period do not automatically mean deflation. The macro signal becomes more important when price declines are broad, persistent, and connected to demand weakness, credit tightening, debt stress, or policy constraints.

What deflation means

Deflation describes a decline in the overall price level, not simply a cheaper item on a shelf. In inflation dynamics, it sits on the opposite side of positive inflation: instead of prices rising more slowly, the measured price level is falling.

The distinction matters because a broad price-level decline can change how debt, income, spending, and policy interact. If wages, revenues, and asset values weaken while debt payments remain fixed in nominal terms, the real burden of debt can rise even though the headline price level is falling.

Deflation vs disinflation

Deflation and disinflation are often confused because both involve weaker inflation pressure. The difference is whether prices are still rising.

Disinflation means inflation is positive but slowing. Deflation means the general price level is falling. A move from 6% inflation to 3% inflation is disinflation. A move below zero inflation is deflation.

| Concept | Price-level behavior | Simple reading | Macro interpretation |

|---|---|---|---|

| Inflation | Prices rise | The price level is increasing | Nominal growth, policy response, wages, margins, and expectations may all matter |

| Disinflation | Prices still rise, but more slowly | The inflation rate is falling | Inflation pressure is cooling without a broad fall in the price level |

| Deflation | Prices fall | The general price level is declining | Debt burden, nominal income, credit stress, policy room, and risk appetite may become more important |

What deflation is and what it is not

A clean deflation reading requires more than a visible price decline. The key test is whether the decline is broad enough and persistent enough to affect the wider inflation environment.

| Deflation is | Deflation is not |

|---|---|

| A sustained decline in the general price level | A temporary sale or seasonal discount |

| Usually represented as negative inflation | A slower positive inflation rate |

| A broad inflation-dynamics condition | A price decline in one product or narrow sector |

| A signal that needs context from demand, credit, debt, and policy | An automatic recession signal or asset-market prediction |

| A possible source of real debt-burden pressure | A guaranteed benefit for consumers in every setting |

How deflation can form

Deflation can come from more than one channel. A weak-demand version is different from a productivity-driven version, and a credit-stress version is different from a short-lived relative-price adjustment.

A demand-driven deflation pattern can appear when households and firms reduce spending, businesses lose pricing power, inventories build, and nominal revenue pressure spreads. A credit-driven version can appear when borrowing conditions tighten, debt repayment becomes harder, and forced deleveraging reduces spending or investment.

Supply improvements can also lower prices. That does not always carry the same macro stress as debt-deflation pressure. The interpretation depends on whether falling prices are linked to stronger productive capacity or to weaker income, weaker demand, tighter credit, and rising real debt burdens.

| Possible channel | Deflation reading | Important limitation |

|---|---|---|

| Demand weakness | Firms cut prices because buyers are pulling back | Needs confirmation from spending, labor, credit, and revenue conditions |

| Credit tightening | Debt service pressure and reduced financing weaken demand | The stress depends on leverage, refinancing needs, and policy response |

| Productivity or supply improvement | Output becomes cheaper to produce | Lower prices may not carry the same stress as demand-led deflation |

| Relative-price adjustment | One sector or input falls sharply | Not enough by itself to prove broad economy-wide deflation |

Why falling prices can still create stress

Falling prices can look positive at the consumer level because purchasing power appears to improve. The macro problem begins when falling prices are broad enough to pressure incomes, revenues, wages, collateral values, or debt repayment capacity.

Debt is usually fixed in nominal terms. If the price level, revenues, or wages fall while debt payments do not adjust down in the same way, debt becomes heavier in real terms. That can pressure households, firms, banks, and governments in different ways.

The spending channel is also context-dependent. The risk is not that every consumer always delays every purchase. The risk is that persistent price declines can weaken expected income, reduce pricing power, tighten credit, and make debt repayment more difficult, which can reinforce weaker demand.

Why deflation matters for market structure

For market structure analysis, deflation is not only a definition. It is a regime input that can affect how macro conditions are interpreted across rates, credit, equities, currencies, and risk appetite.

Broad deflation pressure can raise real rates if nominal interest rates do not fall enough to offset falling inflation. Higher real-rate pressure can tighten financial conditions even when headline inflation looks low. That is why the same inflation print can mean different things depending on policy room, credit spreads, labor conditions, and growth momentum.

Market-based inflation measures such as breakeven inflation can help frame how investors price inflation compensation, but they should not be treated as a clean forecast of future CPI. In a deflation-pressure regime, the useful question is how price-level weakness interacts with real rates, credit conditions, and nominal growth.

Deflation can also pressure nominal revenues. If companies sell at lower prices while costs and debt obligations do not adjust smoothly, margins and cash flows can become more vulnerable. In markets, that can make credit conditions, earnings expectations, and liquidity conditions more important than the headline price decline alone.

The cleanest market reading separates the price-level signal from the surrounding regime. Falling inflation pressure with stable growth and healthy credit is not the same as broad deflation with tightening credit, weak labor income, rising real debt burden, and limited policy room.

Deflation and policy room

Persistent deflation can make monetary policy harder because nominal interest rates have practical limits. If inflation is negative and nominal rates cannot move down enough, real rates can remain restrictive even when policymakers are trying to support demand.

Expectations matter as well. If households, firms, and investors begin to expect lower prices and weaker nominal income, policy may need to fight both current weakness and the belief that weakness will persist. That makes inflation expectations an important part of the broader deflation picture.

That does not mean every deflation reading becomes a deflationary spiral. Policy response, credit conditions, labor income, fiscal support, productivity, and external shocks all affect whether deflation remains contained or becomes self-reinforcing.

Common misunderstanding

The most common mistake is treating every price decline as the same signal. A discount on one product, a falling commodity price, and a sustained decline in the broad price level are different things.

Another mistake is treating deflation as automatically good or automatically disastrous. The cause matters. A productivity-led price decline can have a different meaning from a demand-collapse or debt-stress deflation. The persistence matters as well. A temporary price-level dip is not the same as an entrenched deflationary environment.

For the tighter boundary case, disinflation vs deflation separates falling inflation from an outright fall in the general price level.

A practical way to read deflation

A useful deflation check starts with the price data, but it should not end there. The stronger question is whether the decline is broad, persistent, and tied to stress in nominal growth, credit, debt, or policy transmission.

A narrow product-price decline may reflect supply improvement, competition, inventory clearance, or a one-off shock. A broader deflation signal becomes more important when it appears alongside weaker demand, soft labor income, tighter lending standards, widening credit spreads, falling inflation expectations, and rising real debt pressure.

If policy response and demand recovery begin pushing the economy away from deflationary pressure, the regime can shift toward reflation. That is why deflation should be read as part of a changing macro process rather than as a static label.