Sticky inflation means inflation pressure tied to prices, wages, or components that adjust slowly. It does not mean inflation will stay high forever, and it does not forecast markets by itself. It matters because slow-moving services prices, contracts, rents, wage setting, expectations, and policy credibility can make inflation harder to cool and harder to interpret without broader macro context.

It is related to inflation persistence, but it is narrower: sticky inflation describes slow adjustment inside prices or wages, while inflation persistence describes inflation remaining elevated or slow to fade across time.

Common mistake: sticky inflation is often treated as a simple warning that markets must weaken or that central banks must stay hawkish. The better reading is narrower. Sticky inflation describes slow adjustment inside the inflation process. Policy and market conclusions still depend on growth, liquidity, yields, margins, shock source, expectations, and risk appetite.

Sticky inflation belongs inside the broader study of inflation, but it does not replace the broader inflation concept. It focuses on the parts of price pressure that are harder to reverse quickly after the initial shock has appeared.

Core Points

- Sticky inflation refers to slow-adjusting price or wage pressure, not a promise that inflation stays high forever.

- Sticky-price CPI and flexible-price CPI are measurement lenses. They do not create a market forecast by themselves.

- Sticky inflation becomes more important when services, wages, rents, contracts, expectations, and policy credibility reinforce each other.

- The same sticky inflation reading can mean different things depending on growth, liquidity, yields, margins, and risk appetite.

What Sticky Inflation Means

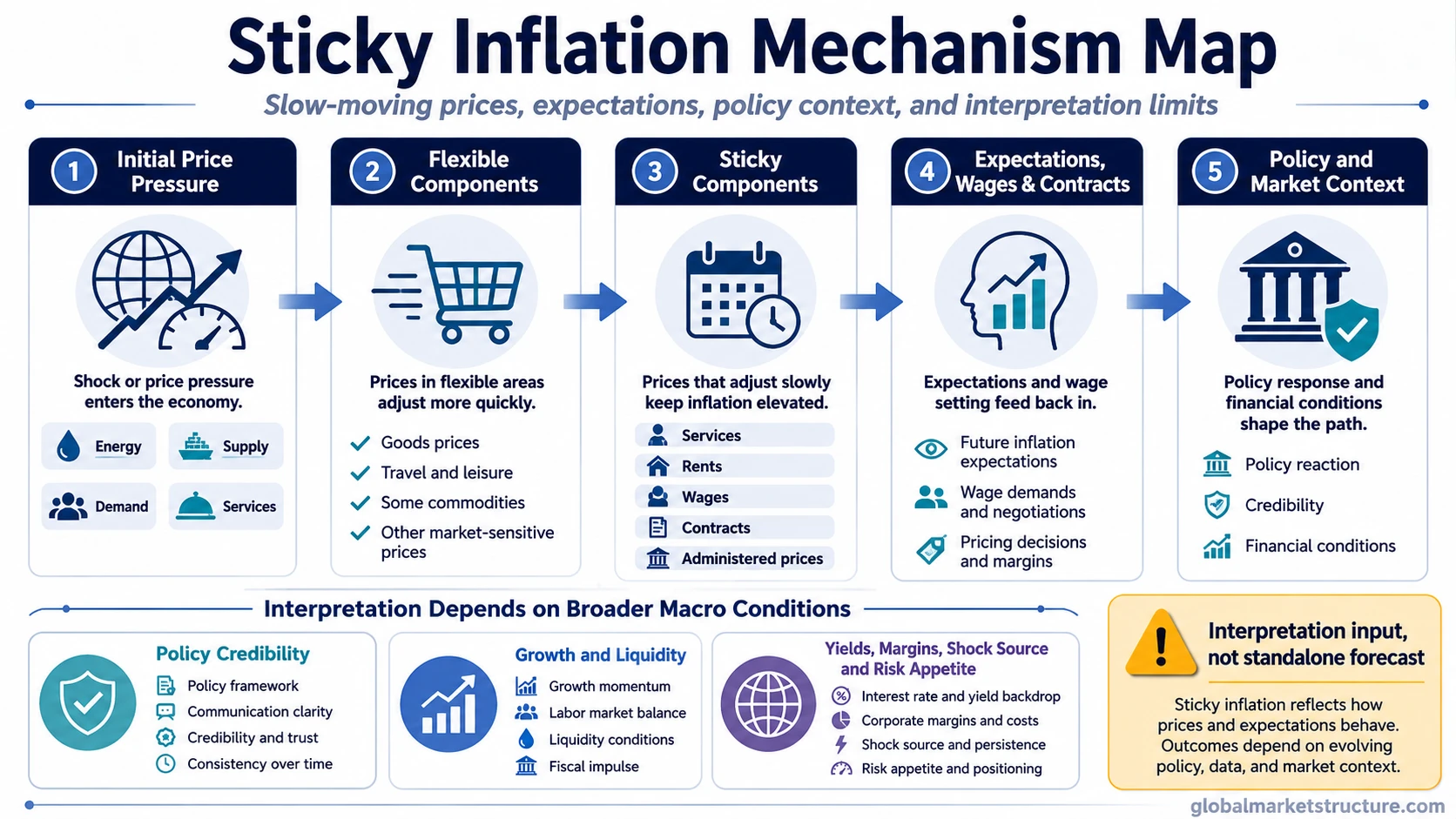

Sticky inflation describes inflation pressure that does not adjust quickly after a shock. The pressure may come from services, wages, rents, contracts, administered prices, or business pricing behavior that changes slowly rather than immediately.

Flexible prices can move quickly when energy, goods, supply chains, or commodity inputs change. Sticky prices tend to move less often. That slower adjustment can make inflation look stubborn even when some headline components are already cooling.

The concept is useful because it separates a temporary price shock from the parts of inflation that can keep pressure alive. It becomes less useful when it is turned into a single-step forecast for central-bank decisions, bond yields, equities, recession risk, or risk assets.

Sticky Inflation vs Inflation Persistence

Sticky inflation and inflation persistence are related, but they are not the same concept. Sticky inflation focuses on why some prices or wage-setting processes adjust slowly. Inflation persistence focuses on whether inflation remains elevated or fades slowly across time.

Sticky inflation: the mechanism is slow price or wage adjustment.

Inflation persistence: the outcome is inflation pressure that remains elevated or slow to fade.

This distinction matters because a persistent inflation episode may include both sticky and flexible components. A sticky inflation reading may also appear without proving that the entire inflation process will keep accelerating.

Sticky-Price CPI and Flexible CPI

The Atlanta Fed describes Sticky-Price CPI as a monthly index that sorts CPI components into either flexible or sticky categories based on the frequency of price adjustment. In that framing, sticky prices are slower to change, while flexible prices adjust more frequently.

FRED’s series notes describe Sticky Price CPI as a subset of CPI goods and services whose prices change relatively infrequently. Because those prices change less often, they are thought to incorporate expectations about future inflation to a greater degree than prices that change more frequently.

Measurement limit: sticky-price CPI can help identify slower-moving inflation pressure, but it is not a complete policy model, recession model, equity model, bond model, or trading signal. It measures a price behavior category. It does not decide the market conclusion.

Data-source note: current Sticky-Price CPI readings belong at the Atlanta Fed or FRED source. Evergreen interpretation works better when it focuses on what the sticky/flexible split means, not on a stale data point.

Why Inflation Can Become Sticky

Inflation can become sticky when prices are slow to reset, when wage agreements adjust gradually, or when businesses avoid changing prices too often. Services are often watched closely because labor, contracts, rent, insurance, medical costs, and recurring expenses can adjust more slowly than tradable goods.

Expectations can also matter. If households, workers, or businesses begin to expect future price increases, wage demands and pricing decisions can carry past inflation into later periods. That is why inflation expectations are part of the sticky inflation mechanism, but not the whole explanation.

Policy credibility affects the same process. If a central bank is seen as credible, sticky pressure may still cool over time. If credibility weakens, the same inflation data can become harder to interpret because price and wage setters may build in more future inflation.

Conditions That Change the Interpretation

A sticky inflation reading becomes more useful when it is placed inside a broader macro context. The same measurement can carry different implications depending on whether growth is firm or weakening, whether liquidity is improving or tightening, and whether yields are rising because of real growth, inflation risk, or policy repricing.

| Condition | Possible interpretation | Limitation |

|---|---|---|

| Sticky services prices remain firm while goods prices cool | Inflation pressure may be shifting from flexible goods into slower-moving services | It does not prove broad inflation will accelerate again |

| Sticky inflation appears with anchored expectations | The inflation process may still cool if credibility and demand conditions hold | Anchored expectations do not remove the need to watch wages, rents, and policy reaction |

| Sticky inflation appears while growth weakens | Policy tradeoffs may become more difficult because inflation and activity send mixed signals | Weak growth can change the policy path and market reaction |

| Sticky inflation appears with strong growth and loose financial conditions | Markets may price a higher policy hurdle or slower disinflation path | The outcome still depends on yields, earnings margins, liquidity, and risk appetite |

| Yields rise during a sticky inflation reading | The market may be repricing inflation risk, policy risk, or real growth strength | The cause of the yield move matters more than the sticky inflation label alone |

| Liquidity improves while sticky inflation remains visible | Risk assets may not respond the same way they would under tightening liquidity | Liquidity support does not cancel inflation risk, but it can change the transmission path |

Why Sticky Inflation Can Be Misread

The main failure mode is treating sticky inflation as a shortcut. A sticky inflation measure remains firm, and the conclusion is treated as already known: the central bank must stay restrictive, yields must rise, equities must weaken, or recession risk must increase immediately.

That logic skips the transmission layer. Sticky inflation can raise policy difficulty, but markets react to a wider mix of variables. Growth resilience, liquidity conditions, margin pressure, the source of the inflation shock, real yields, credit conditions, and risk appetite can all change the outcome.

Failure-mode scenario: sticky inflation remains elevated after flexible goods inflation cools. A simple reading says the result must be negative for equities because the policy backdrop is harder. A better reading checks whether earnings margins are compressing, whether liquidity is tightening, whether yields are rising from inflation risk or growth strength, and whether expectations are becoming unanchored. Without those checks, the sticky inflation label is being used as a forecast rather than an input.

What Sticky Inflation Can and Cannot Tell Markets

Sticky inflation can tell markets that the inflation process may be harder to cool than a headline number suggests. It can also show why central banks may hesitate to declare victory too early when slower-moving components remain firm.

A sticky reading can support different market interpretations under different regimes. The safer reading starts with the surrounding conditions: growth, liquidity, yield drivers, expectations, margins, shock source, and risk appetite. Without those checks, the sticky inflation label becomes too broad to carry a market conclusion.

Practical limit: sticky inflation is best treated as a macro condition that changes the policy and valuation context under certain conditions. It is not a standalone asset-market forecast and not a signal to act.

FAQ

Is sticky inflation the same as inflation persistence?

No. Sticky inflation focuses on slow-adjusting prices, wages, or price-setting behavior. Inflation persistence focuses on inflation remaining elevated or slow to fade over time. Sticky components can contribute to persistence, but the two terms are not synonyms.

Does sticky inflation mean the Fed must keep rates high?

No. Sticky inflation can make policy interpretation more difficult, but it does not mechanically decide the rate path. Central banks also consider growth, labor conditions, expectations, financial conditions, credibility, and risk to the broader economy.

Is sticky-price CPI a market signal?

No. Sticky-price CPI is a measurement lens for slower-changing CPI components. It can help frame inflation pressure, but market interpretation still depends on growth, liquidity, yields, margins, expectations, shock source, and risk appetite.