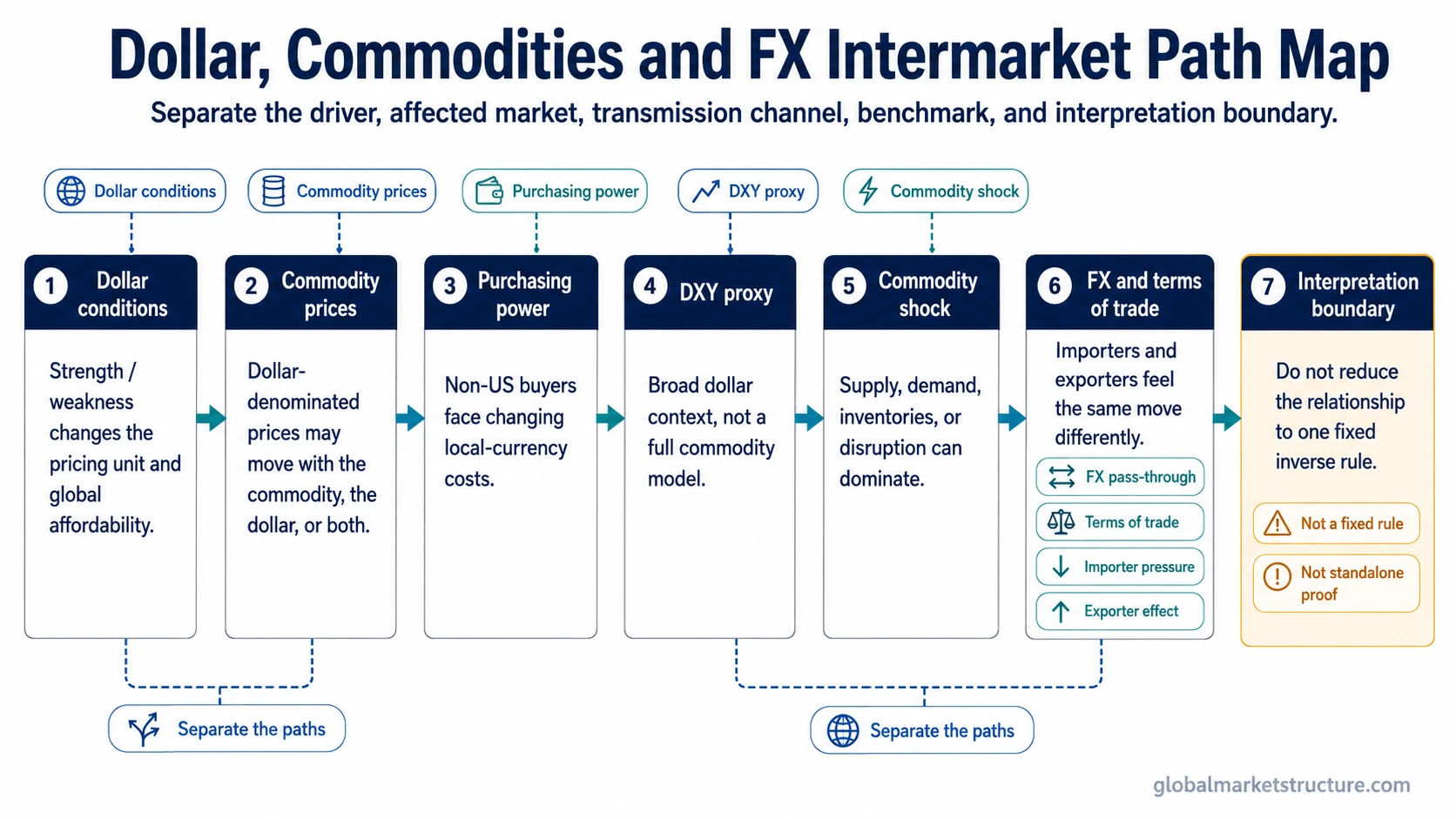

Dollar and commodity prices are linked because many major globally traded commodities are quoted in US dollars, so dollar strength can make them more expensive for non-US buyers and pressure affordability. The link is conditional: supply shocks, inflation pressure, risk conditions, and terms-of-trade shifts can override the simple inverse pattern.

Core relationship: Dollar strength can pressure dollar-denominated commodity prices through purchasing power and affordability, while dollar weakness can support them through easier non-US purchasing power. That connection is a tendency, not a rule.

DXY can help frame broad dollar conditions, but it cannot explain commodity supply, demand, storage, geopolitical disruption, producer behavior, or importer stress by itself. A cleaner interpretation separates the dollar move from the commodity-specific driver before treating the combined move as meaningful.

Key Points

- Dollar strength can pressure commodities when non-US buyers face higher local-currency costs.

- The inverse dollar-commodity pattern is conditional, not automatic.

- DXY is useful for broad dollar context, but it is not a complete commodity-price model.

- Supply shocks, demand shocks, inflation pressure, risk aversion, and terms-of-trade shifts can change the interpretation.

- A commodity price can move because the commodity changed, the dollar changed, or both changed at once.

Why the Dollar Can Pressure Commodity Prices

When commodities are quoted in dollars, a stronger dollar can raise the local-currency cost for buyers outside the United States. That can reduce affordability, slow marginal demand, or force importers to absorb higher costs elsewhere in the economy.

The mechanism is easiest to read when dollar strength is the main new variable and commodity supply conditions are stable. Under those conditions, a stronger dollar can weigh on broad dollar-denominated commodity prices because the same barrel, ton, or ounce becomes more expensive in many other currencies.

The measuring unit can change at the same time as the commodity story. A higher commodity price is not always proof that physical demand improved, and a lower price is not always proof that real supply conditions weakened. Sometimes the dollar side of the quote is doing part of the work.

Why the Relationship Is Not Automatic

The simple inverse pattern weakens when a commodity-specific driver is stronger than the dollar effect. A crop disruption, energy supply shock, mining constraint, shipping bottleneck, or demand surge can lift a commodity even while the dollar is firm.

Limitation: Dollar strength is one force inside a wider intermarket system. Commodity prices also respond to supply, demand, inventories, policy expectations, inflation pressure, risk appetite, and the income effects created by terms-of-trade changes.

Importers and exporters can experience the same market move differently. A commodity-importing country may face higher input costs when the dollar and energy prices rise together. A commodity-exporting country may receive offsetting support through export income, currency effects, or fiscal balances.

Broader regime context also matters. A dollar cycle can change how persistent dollar pressure feels across commodities, FX, liquidity conditions, and risk appetite without turning any single dollar move into a commodity forecast.

DXY as a Proxy, Not a Complete Commodity Model

The DXY Index is useful because it gives a broad proxy for dollar strength or weakness. It can help organize the dollar side of the commodity relationship.

DXY does not measure physical commodity scarcity, refinery demand, crop conditions, inventory pressure, producer discipline, shipping costs, or country-specific import stress. It also does not capture every dollar relationship that matters for commodity buyers and exporters.

A cleaner interpretation starts with one question: is the commodity moving because the dollar changed, because the commodity market changed, or because both are being pushed by a wider macro condition?

Dollar-Commodity Interpretation Boundary Table

The dollar-commodity link becomes clearer when the driver, affected market, transmission path, proxy, and boundary are separated before drawing conclusions.

| Driver | Affected market | Transmission channel | Benchmark / proxy | Interpretation boundary |

|---|---|---|---|---|

| Dollar strength | Broad dollar-denominated commodities | Lower non-US purchasing power and weaker affordability | DXY / broad dollar measure | Can be overridden by commodity-specific supply or demand shocks |

| Dollar weakness | Commodities and real assets | Easier non-US purchasing power and currency repricing | DXY / broad dollar measure | Does not guarantee broad commodity strength if demand is weak |

| Commodity supply shock | Specific commodity or commodity complex | Physical scarcity, input-cost pressure, or inventory stress | Commodity index or spot benchmark | Can dominate the normal dollar-price mechanism |

| Terms-of-trade shift | Commodity importers and exporters | Income, currency, trade-balance, and fiscal pressure | FX basket and commodity terms | Different countries can experience the same commodity move differently |

| Inflation or FX pass-through | Consumer and producer prices | Imported cost pressure and margin pressure | CPI, PPI, FX, and import-price measures | Not the same as a complete inflation-regime reading |

When Dollar and Commodities Can Rise Together

A common failure mode appears when DXY rises while oil, energy, metals, or a broader commodity basket also rises. A simple inverse rule would treat that as contradictory. A cleaner interpretation separates whether a supply shock, inflation shock, or terms-of-trade shift is dominating the normal purchasing-power pressure.

Example scenario: Dollar strength increases pressure on non-US buyers, but an energy supply disruption lifts oil prices at the same time. The dollar effect is still present, yet the commodity-specific shock dominates. The combined move can pressure importers more severely because they face both a stronger dollar and a higher commodity price.

That type of move does not prove a permanent regime shift. It shows why the dollar side and the commodity side need to be separated first. If a long commodity-cycle backdrop is also developing, a commodity supercycle framework can help separate cyclical repricing from a shorter dollar move.

Common Misreads

| Misread | Cleaner interpretation |

|---|---|

| Treating a stronger dollar as automatic commodity weakness | The pattern can fail when supply scarcity, inflation pressure, or risk conditions dominate. |

| Treating DXY as a complete commodity model | DXY helps frame the dollar side, but commodity fundamentals still need separate analysis. |

| Treating a nominal commodity-price move as proof that real commodity conditions changed | The price may reflect the commodity, the dollar, or both. |

| Treating one commodity as the whole commodity complex | An oil shock, metals move, or agricultural disruption may not describe broad commodity behavior. |

FAQ

Does a stronger dollar always lower commodity prices?

No. A stronger dollar can pressure commodity prices through purchasing power and affordability, but supply shocks, demand shocks, inflation pressure, risk aversion, and terms-of-trade shifts can override that effect.

Can DXY explain commodity prices by itself?

No. DXY can frame broad dollar strength or weakness, but it does not measure commodity supply, inventories, physical demand, shipping constraints, or country-specific import stress.

Why can the dollar and commodities rise together?

The dollar and commodities can rise together when a commodity-specific shock, inflation shock, or terms-of-trade shift is stronger than the normal purchasing-power effect of dollar strength.