A commodity supercycle is a long-duration commodity price regime driven by structural demand and supply conditions that take years to rebalance. It is not the same as a normal commodity rally, a short oil shock, a single-metal shortage, an inflation headline, or a trading signal.

The classification depends on duration, breadth, demand durability, supply constraints, and macro relevance. A fast price spike can matter, but it is not enough on its own. The key question is whether the move reflects a persistent imbalance that cannot be solved quickly by inventories, substitution, policy reaction, or new supply.

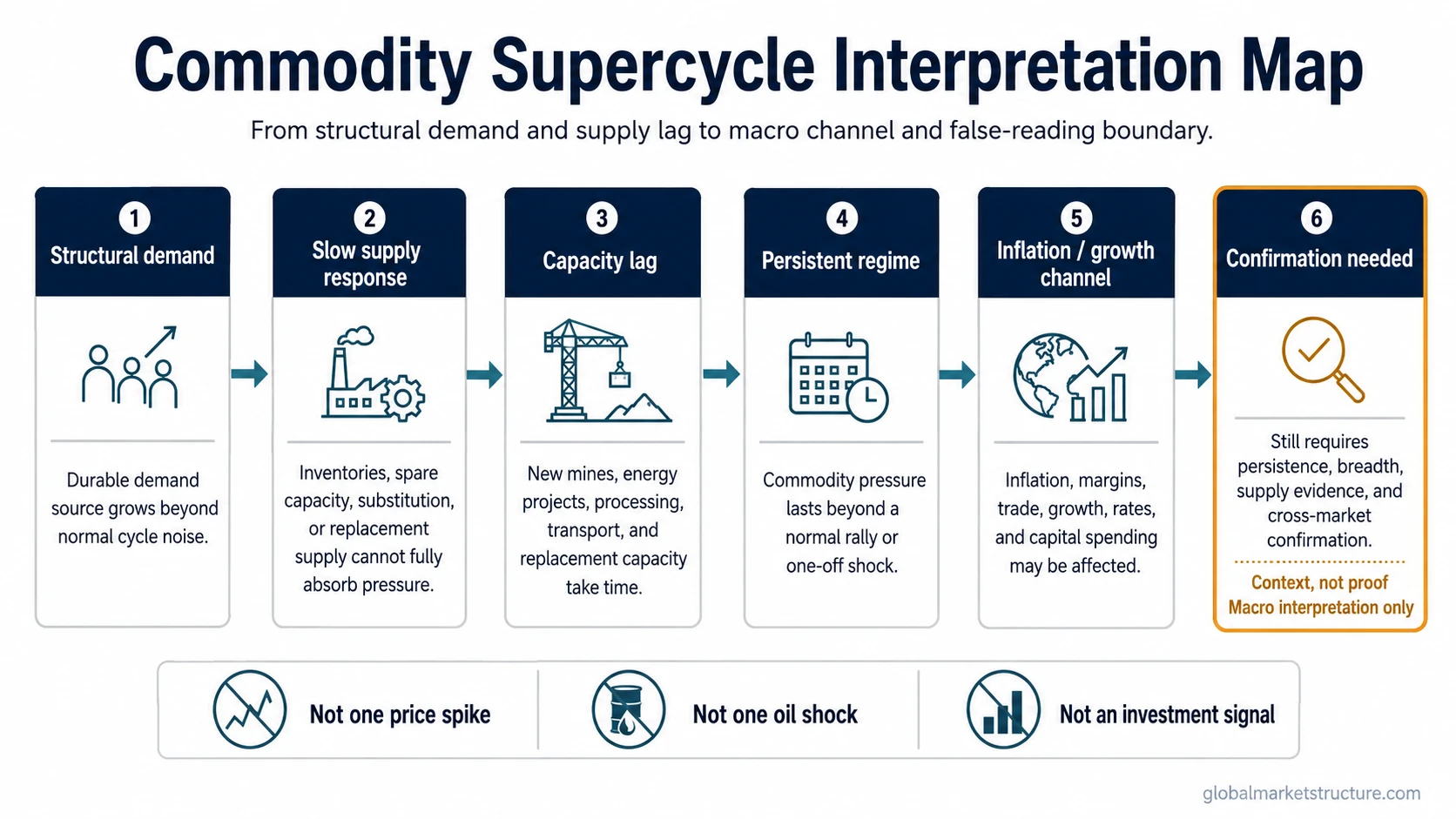

Definition: A commodity supercycle is a multi-year commodity regime in which persistent demand pressure and slow supply adjustment keep commodity prices elevated or structurally supported for longer than a normal cyclical rally.

What drives it: Durable demand growth, underbuilt supply, long investment lead times, delayed capacity response, and macro conditions that keep the imbalance relevant.

What it is not: A short-term price spike, a single supply disruption, a one-commodity shortage, an automatic inflation forecast, or a recommendation to own commodities or commodity producers.

Key Points

- A commodity supercycle is defined by structural imbalance and duration, not by one strong commodity move.

- Supply lag matters because new production capacity can take years to appear.

- Commodity strength can affect inflation and growth interpretation, but it does not predict inflation, recession, growth, or asset returns by itself.

- Producer equities add company, margin, leverage, and execution risk beyond the commodity regime itself.

- A supercycle thesis remains conditional until the move shows persistence, macro relevance, and resistance to normal rebalancing.

Commodity Supercycle vs Commodity Rally vs Commodity Shock

A normal commodity rally can happen inside a business cycle. A commodity shock can come from a sudden supply interruption. A commodity supercycle is different because it points to a longer regime problem where demand and supply cannot quickly return to balance.

| Move type | Usual driver | Time profile | What it may show | What it does not prove |

|---|---|---|---|---|

| Ordinary commodity rally | Cyclical demand, inventory restocking, weaker currency, or temporary risk appetite | Short to medium term | Commodities are being repriced within a normal cycle | A structural supercycle has started |

| Commodity shock | Supply disruption, geopolitical stress, weather, transport issue, or policy restriction | Often sudden | A specific market is stressed | Broad commodity conditions are structurally imbalanced |

| Single-metal shortage | Narrow demand surge or supply bottleneck in one market | Can be persistent but concentrated | One commodity complex has a constraint | All commodities are in a supercycle |

| Commodity supercycle | Durable demand plus slow supply adjustment | Multi-year | A broader or structurally important commodity regime is forming | An automatic investment signal or macro forecast |

An oil shock can overlap with commodity inflation, but it is usually narrower and more event-driven. A commodity supercycle requires a broader or more persistent imbalance.

What Can Cause a Commodity Supercycle?

A commodity supercycle usually begins with a demand shift that is too large or too persistent for existing supply to absorb. The demand side may come from industrial expansion, infrastructure buildout, energy systems, defense demand, electrification, urbanization, or other durable forces. The specific driver matters less than whether it lasts long enough to strain capacity.

The supply side is just as important. Commodity supply often cannot respond instantly. New mines, energy projects, processing capacity, transport infrastructure, and replacement supply can require large capital commitments and long development timelines. If producers underinvest during the previous downcycle, the next demand wave can meet a thinner supply base.

Commodity Supercycle Mechanism

- Durable demand rises faster than available supply.

- Inventories, spare capacity, or substitution absorb the first pressure.

- New capacity is slow because it needs capital, permits, labor, infrastructure, and time.

- Prices stay firm enough to affect inflation, margins, investment, or terms-of-trade interpretation.

- The reading becomes more credible only if the imbalance persists beyond a normal cyclical rally.

- The interpretation remains limited unless macro, cross-asset, and supply evidence support the regime.

The concept is therefore not only about price. It is about the interaction between price, demand durability, supply lag, and the broader market environment.

The Inflation and Growth Channel

Commodity supercycles matter for macro interpretation because commodities sit near the input layer of the economy. Energy, metals, food, and industrial materials can affect production costs, transportation costs, capital spending, margins, trade balances, and inflation expectations.

The inflation channel is conditional. Persistent commodity pressure can make inflation harder to dismiss, especially when the affected commodity complex feeds into many parts of the economy. But commodity strength does not by itself create a sustained inflation regime. The effect depends on breadth, pass-through, currency conditions, policy response, wage behavior, and whether demand remains strong enough to absorb higher input costs.

The growth channel is also conditional. Rising commodity prices can reflect stronger real demand when industrial activity is improving. They can also pressure growth if higher input costs squeeze households, firms, or import-dependent economies. A commodity supercycle can therefore be connected to growth optimism, supply stress, inflation pressure, or margin compression depending on the surrounding context.

What Confirms or Weakens the Supercycle Reading?

A commodity move becomes more credible as a supercycle candidate when the explanation survives several checks. The move should be persistent, tied to a durable demand source, and difficult to rebalance through normal supply adjustment. It should not depend only on one headline, one weather event, one inventory draw, or one speculative narrative.

| Check | Stronger reading | Weaker reading |

|---|---|---|

| Duration | Pressure persists beyond a short cyclical move | Move reverses after inventory, policy, or supply normalization |

| Demand driver | Demand is durable and multi-year | Demand is mostly restocking, speculation, or temporary |

| Supply adjustment | New capacity is slow, constrained, or delayed | Supply can respond quickly |

| Breadth | Multiple commodities or a structurally important complex are involved | One isolated commodity dominates the story |

| Macro channel | Inflation, margins, trade, rates, or growth interpretation are affected | Price move remains narrow and market-specific |

| Cross-market context | Related assets, spreads, currencies, or cycles support the interpretation | Other markets reject the supercycle narrative |

The copper-gold ratio can sometimes help frame growth-sensitive commodity behavior against defensive metal demand. It should still be treated as context, not proof.

Common False Readings

One price spike equals a supercycle. A spike can reflect disruption, panic buying, low inventory, or positioning. A supercycle requires persistence and structural imbalance.

One oil shock equals a broad commodity regime. Energy shocks can be macro-relevant, but they do not automatically imply a multi-commodity supercycle.

One critical-mineral shortage proves a broad supercycle. A narrow bottleneck can be important without representing the whole commodity complex.

Commodity strength automatically predicts inflation or recession. Commodity prices can feed inflation and growth interpretation, but the signal depends on pass-through, policy, demand, and cross-asset confirmation.

A supercycle thesis means commodity producers are the cleanest expression. Commodity producer equities add company-level risk, operating leverage, balance-sheet risk, margin sensitivity, and execution risk. The macro concept and the equity expression are separate layers.

Practical Scenario

A common scenario is that a durable demand source begins growing while producers are still cautious after a prior downcycle. Inventories can soften the first phase, but if demand keeps rising and new supply takes years to develop, prices may remain firm even after short pullbacks.

That still does not prove a supercycle. The interpretation becomes stronger only if the pressure persists, capacity remains slow to adjust, and the move starts affecting broader macro channels such as input costs, capital spending, trade balances, or inflation expectations. If supply arrives faster than expected or demand weakens, the same setup can become a normal commodity cycle rather than a supercycle.

Related Market Structure Concepts

A commodity supercycle belongs inside intermarket analysis because commodities connect real-economy demand, inflation pressure, industrial activity, and supply constraints. It is useful as a macro classification tool, not as a stand-alone forecast.

The concept also connects to real assets, because long commodity regimes can change the interpretation of inflation sensitivity and tangible-asset exposure. That connection does not make real assets an automatic hedge or portfolio answer.

The broader business cycle still matters. A commodity move during early expansion can carry a different meaning than a commodity move during late-cycle inflation stress or growth slowdown. The same price direction can reflect different regimes depending on the surrounding cycle evidence.

FAQ

What is a commodity supercycle?

A commodity supercycle is a long-duration commodity price regime caused by structural demand and supply conditions that take years to rebalance. It is broader and more persistent than a normal cyclical rally.

How is a commodity supercycle different from a normal commodity rally?

A normal rally can happen because demand improves, inventories tighten, or risk appetite rises. A commodity supercycle requires a more persistent imbalance where supply cannot quickly respond to durable demand.

Does a commodity price spike mean a supercycle has started?

No. A price spike can come from disruption, positioning, low inventory, or a temporary shock. A supercycle requires duration, structural drivers, supply lag, and macro relevance.

Is a commodity supercycle an investment signal?

No. It is a macro classification concept. It can help interpret inflation, growth, supply constraints, and market regime, but it is not a buy signal, allocation rule, or commodity producer recommendation.